Lockdown Leadership Unlikely To Last

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Points

-

In the last few weeks, stock market leadership reversed back to lockdown-era defensives as the stock market made new all-time highs.

-

The defensive turn by investors may be prompted by the rapidly spreading Delta variant of COVID-19.

-

This year’s swings between cyclicals and defensives, value and growth, and international and U.S. stocks exemplify the importance of holding a diversified portfolio to help reduce overall portfolio volatility.

In what seems like a return to the market of a year ago, the last few weeks have seen defensive stocks outperform more economically sensitive stocks, like internet retailing stocks leading airline stocks, growth stocks leading value stocks and U.S. stocks leading international stocks. Surprisingly, this leadership rotation in the stock market back to lockdown-era defensives has coincided with new all-time highs. Let’s examine the potential causes of this rotation and if it will last or if cyclical stocks might make a comeback in the second half of the year.

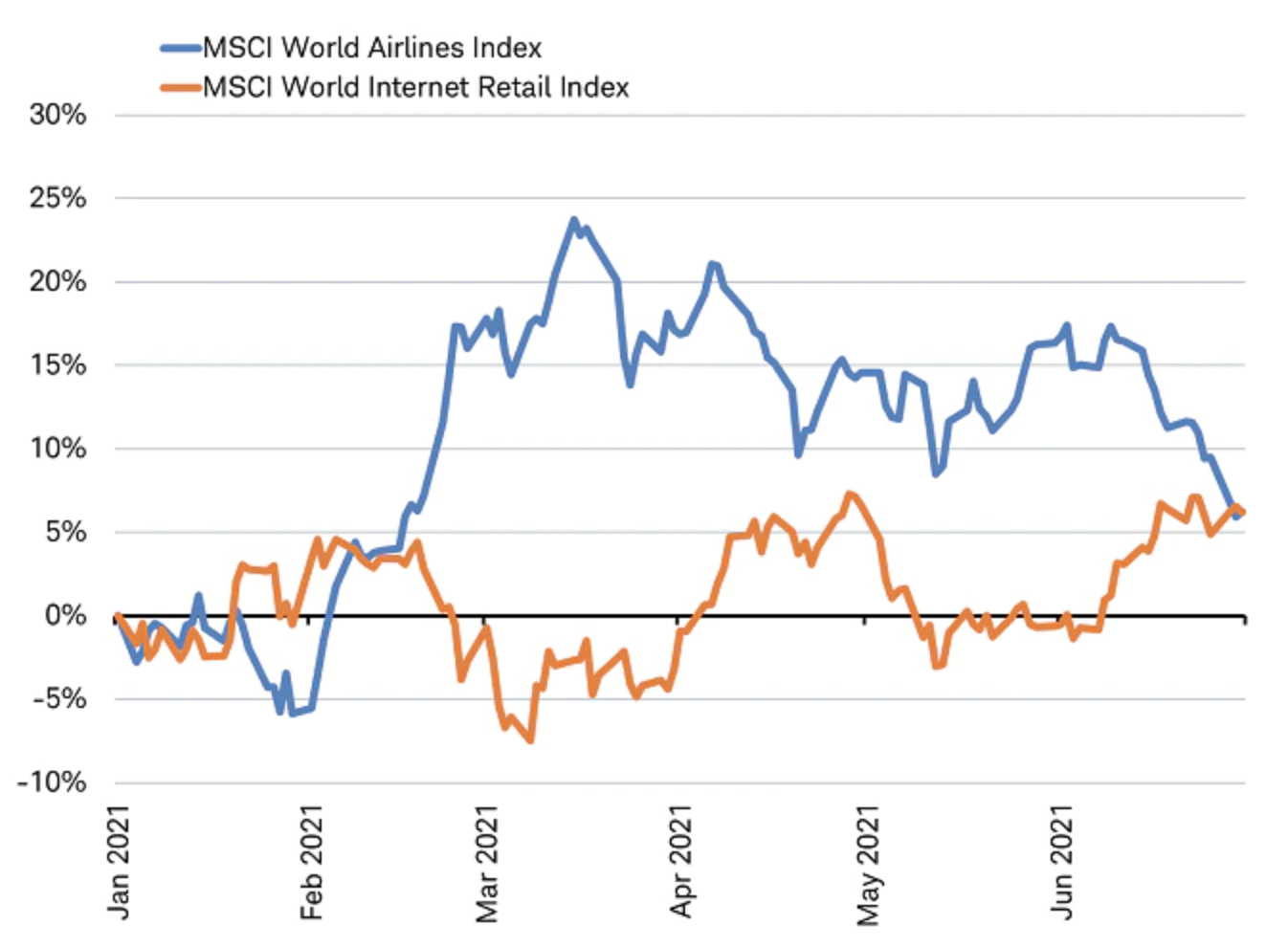

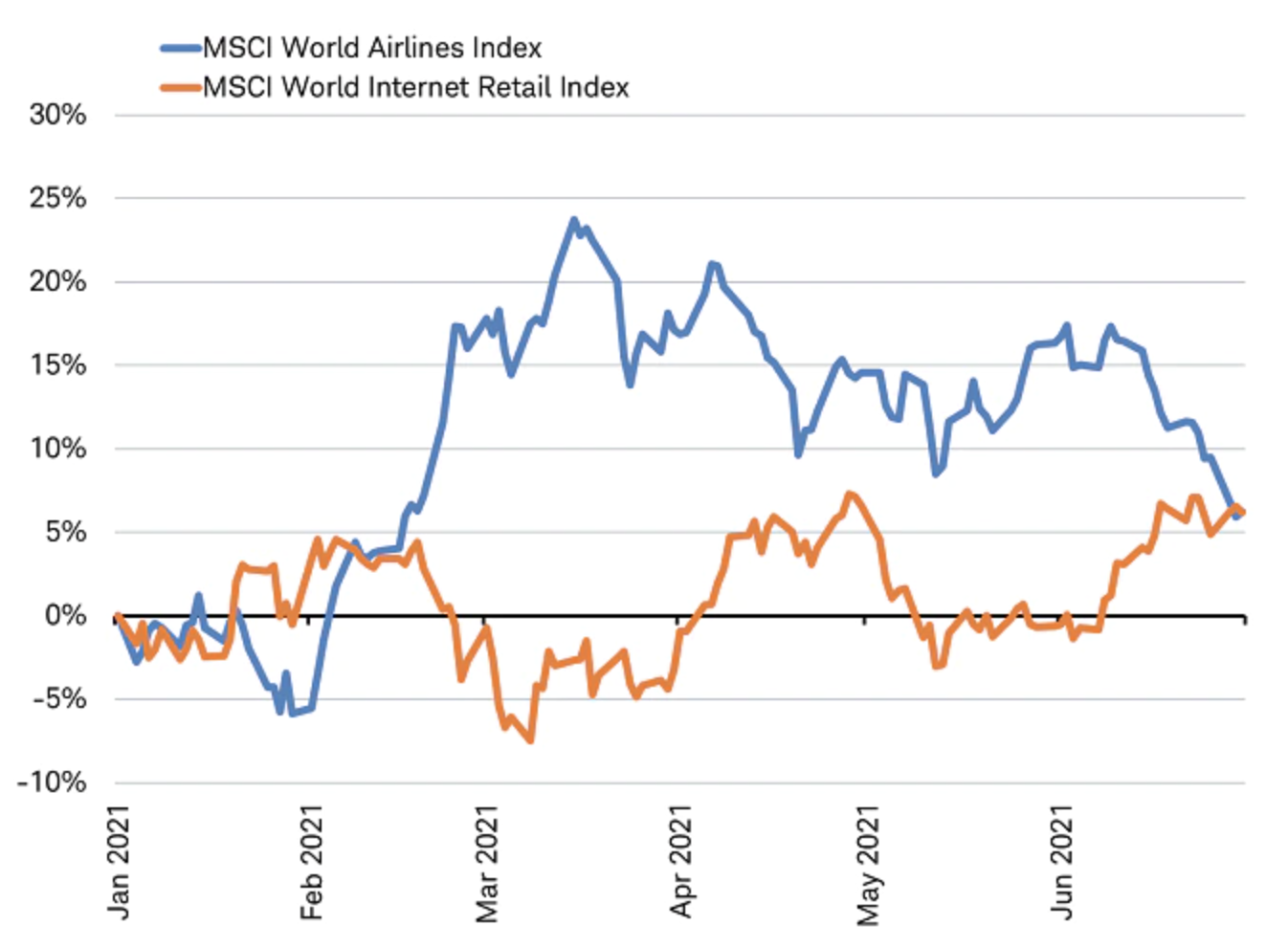

Airlines versus internet retailers year-to-date performance

Source: Charles Schwab. Bloomberg data as of 7/2/2021. Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. Past Performance is no guarantee of future results.

Defensive leadership

While cyclical stocks had been outperforming lockdown-era defensives for most of this year, the outperformance gap closed sharply in the last few weeks. This may be best illustrated by the above chart of airline stocks, beneficiaries of post-pandemic reopening and pent up desire to travel, and the stocks of internet-retailers, the winners during quarantine when spending was largely confined to online purchases. Despite outperforming since February as the vaccine rollouts accelerated, airline stocks ended up underperforming internet retailers as the first half of 2021 ended.

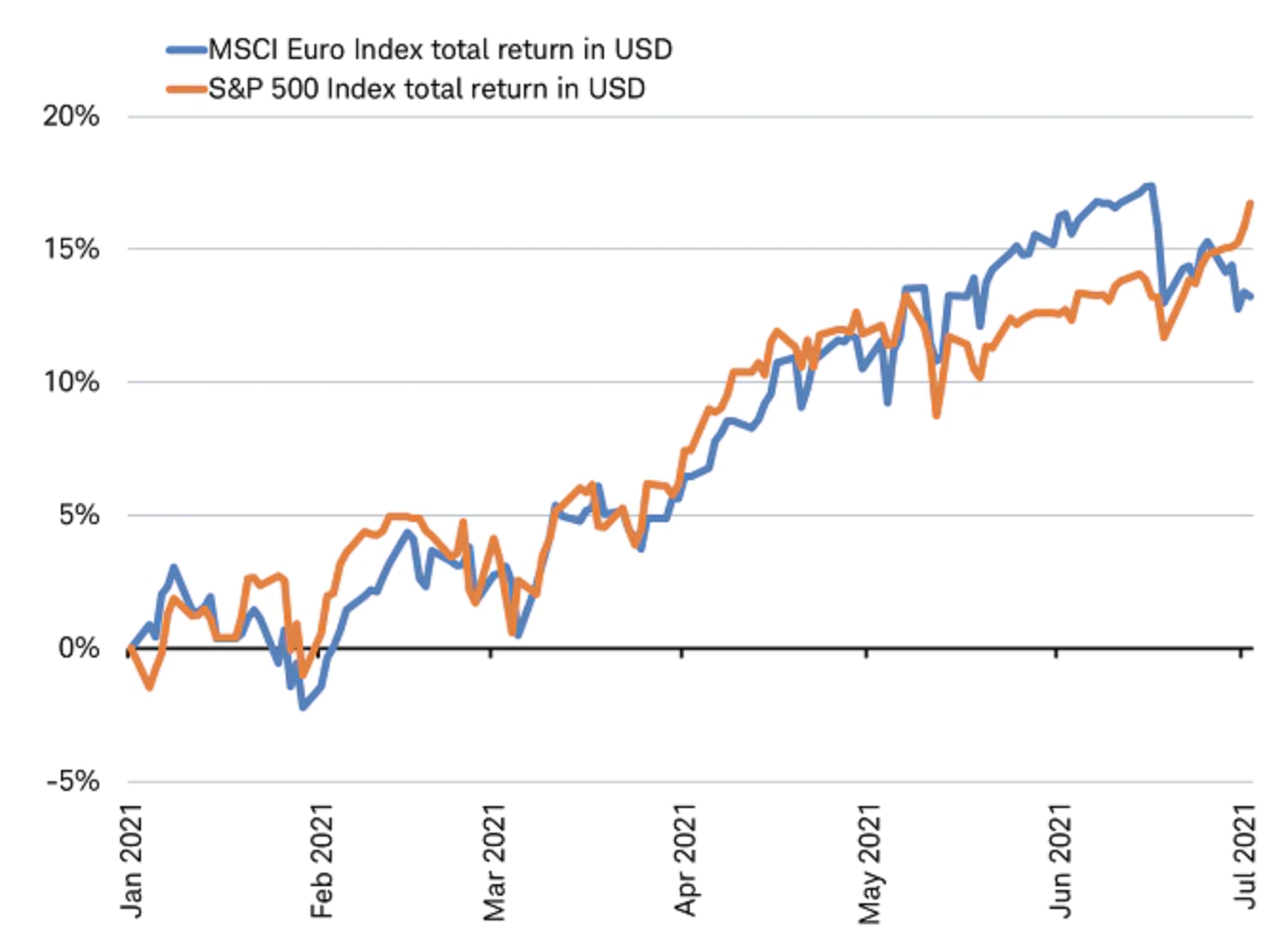

This market rotation is not just across industries but can also be seen across countries. As the U.S. stock market continued to hit new all-time highs in June, the more economically sensitive Eurozone stock market gave back gains starting in mid-June and is now lagging the U.S. on a year-to-date basis.

Eurozone lost its lead in late June

Source: Charles Schwab. Bloomberg data as of 7/2/2021. Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. Past Performance is no guarantee of future results.

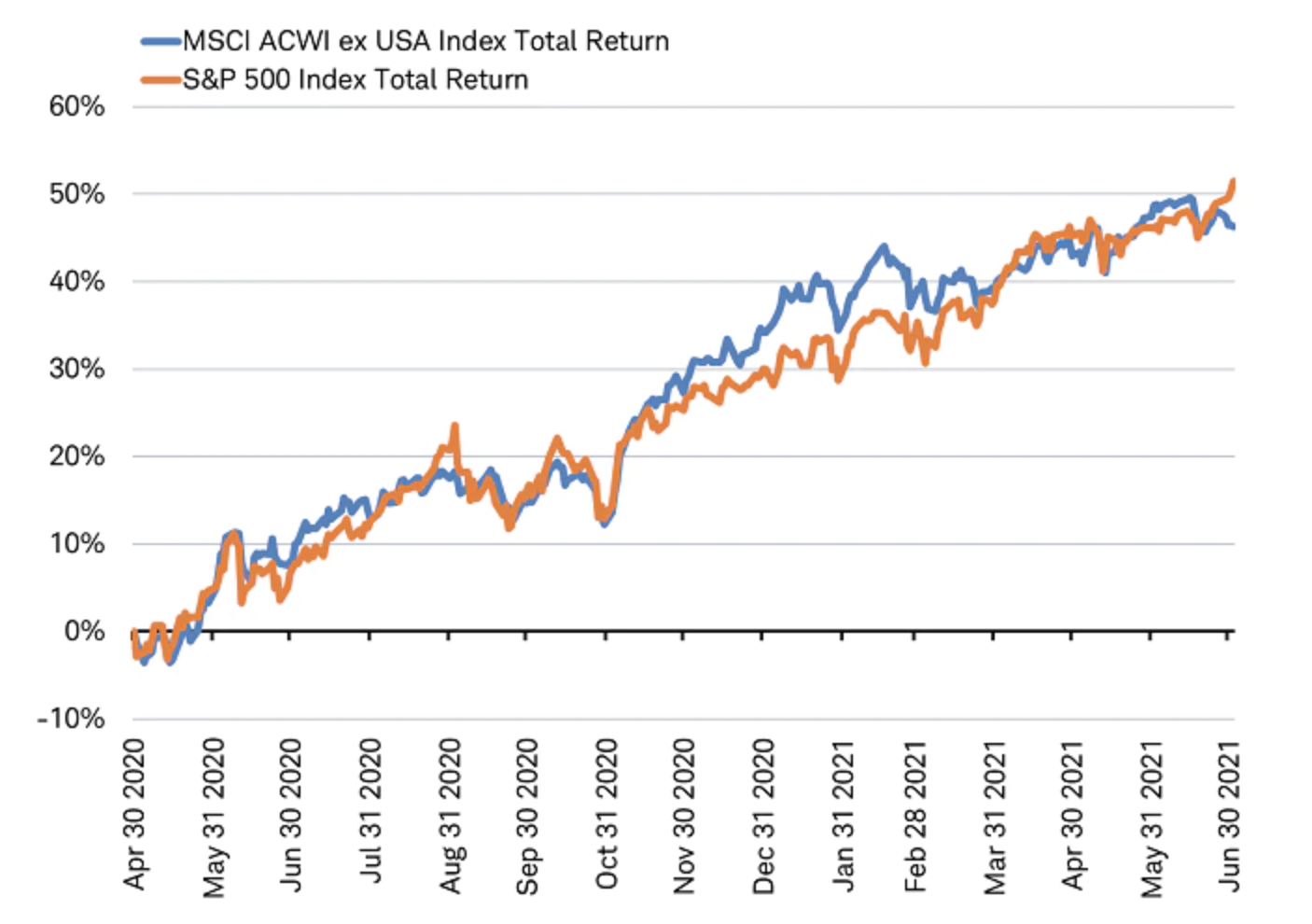

The tech-heavy U.S. stock market benefited from the defensive leadership rotation. As you can see in the chart below, the gap in performance of U.S. and non-U.S. stock returns is now the widest (at 4%) underperformance by non-U.S. stocks since the world’s economic data bottomed in April 2020.

Non-U.S. stocks slip

Source: Charles Schwab. Bloomberg data as of 7/2/2021. Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. Past Performance is no guarantee of future results.

Uncharacteristically, this return to defensive leadership has come alongside positive economic data, which has been exceeding expectations in every major country and region of the world. Corporate earnings estimates continue to climb. Even the recent news for airlines has been good:

- The International Airline Trade Association (IATA) is reporting summer bookings at 80-90% of 2019 levels, compared with 36% in 2020.

- In the U.S., TSA checkpoint numbers show the number of air travelers rose to 2.20 million on July 2 from 719,000 a year ago, exceeding 2.18 million in 2019.

- Last week, United Airlines placed its largest ever order for new airplanes expecting a continuing rebound in air travel.

The return to defensive leadership, accompanied in the bond market by a modest flattening of the yield curve, doesn’t appear to be driven by any deterioration in the economic or earnings environment.

Not the first time

June wasn’t the first time this year we saw a reversal of cyclical leadership. In April, the stock market rotated back to defensives for several weeks as soaring inflation fears gripped the market. Market participants seemed to worry that faster inflation may force central banks to curb stimulus and tighten monetary conditions earlier than anticipated. Yet, in April, stocks rose to new all-time highs, in contrast with the market’s defensive leadership. As commodity prices eased in May and the Fed reassured markets, cyclicals returned to favor.

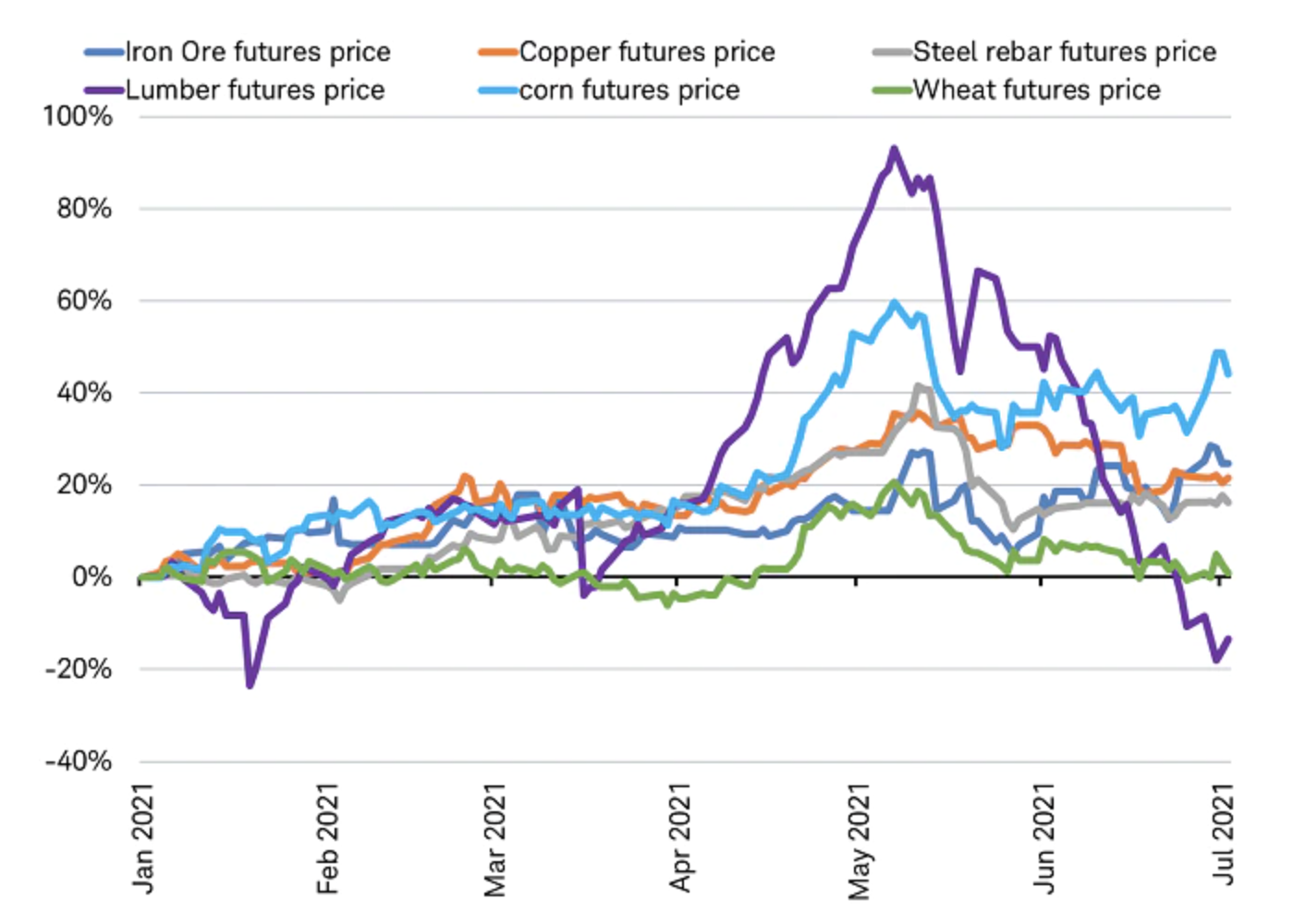

The shift in June back to defensives also came with the MSCI World Index making new all-time highs. Did inflation and Fed concerns prompt the shift again? While the Fed’s mid-June “dot plot” signaled members’ support hiking rates earlier than they did back in March, they still reflect a lift off for rate increases sometime in 2023—two years from now. Unlike in April, most commodity prices are not surging and lifting inflation at a pace that could warrant more aggressive Fed action. In fact, lumber prices have completely reversed their earlier surge in 2021, ending the first half of the year down nearly -20%.

Commodity price surge fades

Source: Charles Schwab. Bloomberg data as of 7/2/2021.

Inflation and central bank actions do not seem to be the primary driver of this latest rotation. Instead, the rapidly spreading Delta variant of COVID-19 may be prompting this defensive turn by investors.

Delta variant

COVID-19 is still the biggest risk to the expansion. Encouragingly, major countries, including China, are on track to have more than 50% of their populations vaccinated this summer.

Rate of vaccination increases in Europe and China as the summer heats up

Source: Charles Schwab, Bloomberg, as of 6/29/2021. *Most vaccines require two doses to be fully vaccinated

On the negative side, the fast spreading Delta variant, potential for new variants and the fact that antibodies wane over time may mean that we could begin see yet another wave of infection. The U.S. could see case counts jump unexpectedly as more than half of states no longer report cases daily. This absence of high frequency data can prevent the early identification of risks that would require immediate response.

Due to propagation of the Delta variant, the World Health Organization is recommending even fully vaccinated people wear masks, socially distance, and avoid crowds to limit ongoing community transmission. Restrictions and lockdowns could come in short-term waves in targeted regions–like those recently reimposed in Sydney and Tokyo. Hospitalizations are on the rise in the U.K. and in some U.S. states. Israel has delayed reopening its borders and Europe has tightened its curbs on U.K. visitors. These responses, should they become more frequent, may affect summer tourism and weigh on the growth outlook. Renewed restrictions would likely be unwelcomed by stocks and could be one reason cyclicals—especially those tied to travel and entertainment—are suffering the most in the recent rotation.

Takeaways

Examining the recent rotation, the biggest short-term investor concern appears to be rising risks from the more contagious Delta variant, with travel & leisure stocks among the worst decliners in June. While very hard to predict, we are hopeful that the vaccines effectiveness against the Delta variant combined with the surge in vaccinations in Europe and Asia may avoid a return to broad-based lockdowns that have a measurable economic impact.

The economic and earnings backdrop remains strong and is supported by unprecedented fiscal stimulus and cautious central banks. It’s possible that the underperformance of cyclicals may be more tied to selling off winners, and not the start of a deeper downturn. When yields begin to rise again the rotation may reverse back to favoring cyclicals.

This year’s swings between cyclicals and defensives, value and growth, and international and U.S. stocks exemplify the importance of holding a diversified portfolio to help reduce overall portfolio volatility.

Michelle Gibley, CFA®, Director of International Research, and Heather O’Leary, Senior Global Investment Research Analyst, contributed to this report.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All