In 2010, 68% of the companies in Fortune Magazine’s Global 500 were domiciled in Group of Seven (G7) countries, compared with 17% in the E20* emerging-market (EM) countries. When 2020 ended, the percentage of E20 companies had nearly doubled to 34%. And 124 China-domiciled firms resided in the Global 500, pushing the US into second place.

That’s quite a decade for EM corporations, and an eventful one for emerging markets more broadly. In a period roughly bookended by the recovery from the global financial crisis and the COVID-19 pandemic, there were good years and bad years that required multi-asset investors to manage volatility while tapping into opportunity.

We’ve seen many attention-grabbing headlines in the past decade, but slower-moving trends may have been even more impactful. We’ll focus on two: the relationship between economic growth and valuations and a transformation from commodity-driven to technology-driven. We’ll also highlight two key trends we expect to see in the decade ahead—and a story that we believe remains timeless.

Disconnect Between Economic Growth and Equity Valuations

The years 2011 through 2020 saw a healthy expansion in emerging economies, with real gross domestic product (GDP) growth averaging 4.1% annually, handily outpacing developed markets’ 1.5%, a trend we expect to continue (Display). China led the cohort of larger countries, but many smaller countries—including Vietnam, Turkey, Ivory Coast and the Dominican Republic—posted above-average growth, too.

Surging economies bolstered government revenues, fundamentals and creditworthiness. All of this was reflected in strong credit returns—given superior growth and declining interest rates globally, that’s not surprising. Many countries with the fastest growth, and therefore greatest credit improvement, such as Ivory Coast and Dominican Republic, could only be accessed by debt investors.

What may be surprising is that overall equity returns weren’t stronger. Historically, equity returns generally outpace debt returns, especially when growth is good. So, how do we square the difference? We think it comes down to earnings growth and valuations. Some firms certainly shone, notably innovative global tech leaders: over the past decade, Tencent’s earnings per share (EPS) vaulted from 1.05 to 14.82 and Samsung Electronics’ from 1,660 to 5,778.

But EM equity indices also include a raft of less competitive companies, many heavily influenced by state owners or regulators. These constituents dragged down overall EPS growth to 5% (total, not annualized) versus 104% for the S&P 500. As a result, investors haven’t bid up overall EM valuations as much (10.2x in 2011 to 14.2x today) as they have in the US, where S&P 500 EPS has risen from 13.5x to 22.6x.

So, growth matters, but in different ways for emerging equity and debt. Equity investors need to find companies that will deliver the strongest earnings growth; sovereign debt investors focus on countries undergoing credit-strengthening reforms that support higher and sustainable economic growth. For multi-asset investors, both trajectories matter to capitalizing on opportunities.

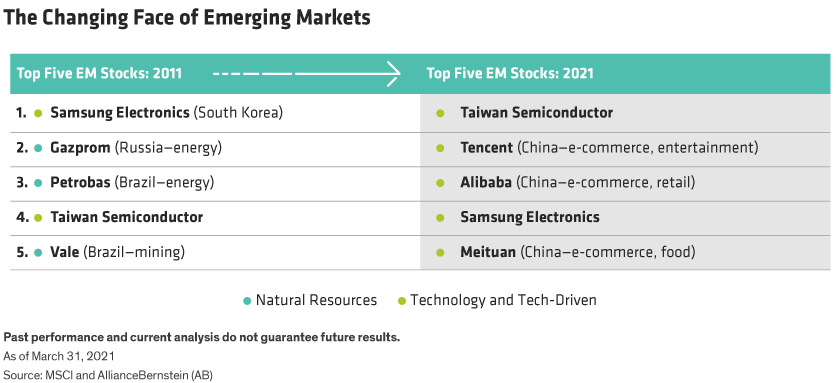

The Great Commodity-to-Technology Transition

A decade ago, emerging equity indices reflected industries typically associated with less developed economies—heavily reliant on natural resources. Index heavyweights were often natural resources issuers needing capital to grow, including energy and mining firms. Banks and telecoms were heavily represented, too.

Fast forward a decade, and technology and innovation dominate emerging equity indices, including many global market leaders (Display). Technology stocks, just 10% of the MSCI EM Index 10 years ago, have doubled their share to 20%. The real proportion is arguably higher, too, because companies such as Tencent and Alibaba aren’t officially classified as technology.

The natural resources to technology evolution has been a sea change for emerging equity indices, and creates an exciting opportunity set that’s very different from the days of dominance by the likes of Gazprom and Petrobras.

Recovery and Emergence From COVID-19

Just as the past 10 years have seen transformation in emerging markets, so will the decade ahead. One notable short-term dynamic will be the road back from the pandemic—a path that will differ for every nation. China, hit first by the pandemic, was also the first to emerge on the other side, leading many Western countries. Taiwan was barely affected, while India and Brazil have been among the hardest hit. As the paths vary, so will the risks and opportunities.

With the world continuing to reopen, we expect business demand for capital and government demand for liquidity to push capital flows beyond the US and early reopeners into other regions, including emerging markets. Strong central bank policy stimulus will likely continue, tempering economic risks. And, as vaccine progress releases pent-up activity, many EM firms will benefit from surging demand in both their domestic and international marketplaces.

A Quest for Supply-Chain Diversification

Another trend that we expect to play out, over the next five years, is accelerating supply-chain diversification, driven in part by concern over geopolitical risk. Today, most products are built with components produced and sourced across the globe, whether it’s a car, computer, coffeemaker or shampoo. Firms will seek to insulate those all-important supply chains from flare-ups and conflicts.

The Suez Canal blockage by a wayward ship highlighted that non-geopolitical risks can crimp stretched supply chains and thin inventories, too. We think companies should—and will—reevaluate existing operations, and emphasize building in greater resilience for the future. In practice, this push will likely translate into building more production facilities and rebuilding inventory in more locations.

Growing scrutiny of environmental, social and governance (ESG) behaviors will also alter supply-chain sourcing. Human rights abuses and climate change, for example, are pressing issues, and the world is increasingly using ESG considerations to steer capital. That will push firms to address ESG concerns in their supply chains, which will require new capital enticed from investors by higher potential returns.

Diversification and Flexibility Still Required

One story that we don’t expect to change over the next decade is the need for investors to integrate exposures thoughtfully when tapping equity, debt and currency opportunities. Getting the formula right can bolster potential returns and diversification, potentially reducing the impact of losses in one company, industry or asset class.

Flexibility will be needed, too, because the full range of emerging opportunities reaches well beyond broad indices. One widely used emerging equity index, for instance, includes issuers domiciled in 26 countries; from our perspective, the emerging universe spans more than 60 countries. A “go anywhere” approach enables multi-asset to cast a much wider net for opportunities.

While much has changed in emerging markets over the past decade, and the next 10 years will likely be just as eventful, we believe firmly that multi-asset strategies that stay diversified, flexible and dynamic stand the best chance of thriving in the decade to come.

*The E20 is a group of top 20 emerging markets selected by Fortune based on their economic and demographic weights. In 2020, the E20 included Argentina, Bangladesh, Brazil, China, Colombia, Egypt, India, Indonesia, Iran, Malaysia, Mexico, Nigeria, Philippines, South Korea, Saudi Arabia, South Africa, Thailand, Turkey, Poland and the Russian Federation.

Morgan Harting is Portfolio Manager—Multi-Asset Solutions at AllianceBernstein (AB)

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

© AllianceBernstein

Read more commentaries by AllianceBernstein