Fed Tapering: Will it Be Different This Time?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs the Federal Reserve transitions from merely talking about tapering its bond holdings to actually tapering, investors may be left wondering what it might mean for the markets and their portfolios. Here’s a quick review of the Fed’s policies, what happened the last time the Fed tapered, and whether it will be different this time.

How we got here

In March 2020, the Federal Reserve was staring down the runway of an unprecedented pandemic with dire economic implications. As a result, the Fed quickly cut the federal funds rate to the range of zero to 0.25% from 1.5% to 1.75% and started purchasing large amounts of Treasuries and agency mortgage-backed securities (MBS) to provide additional stimulus to the economy above and beyond the rate cuts. These large-scale asset purchases are what is commonly referred to as quantitative easing (QE). The goals of quantitative easing are to:

- Support the smooth functioning of the financial markets

- Provide additional stimulus to the economy by lowering borrowing costs

- Put downward pressure on long-term yields to boost investment

- Support the MBS and commercial mortgage-backed securities (CMBS) markets through lowering interest rates for residential and commercial mortgages.

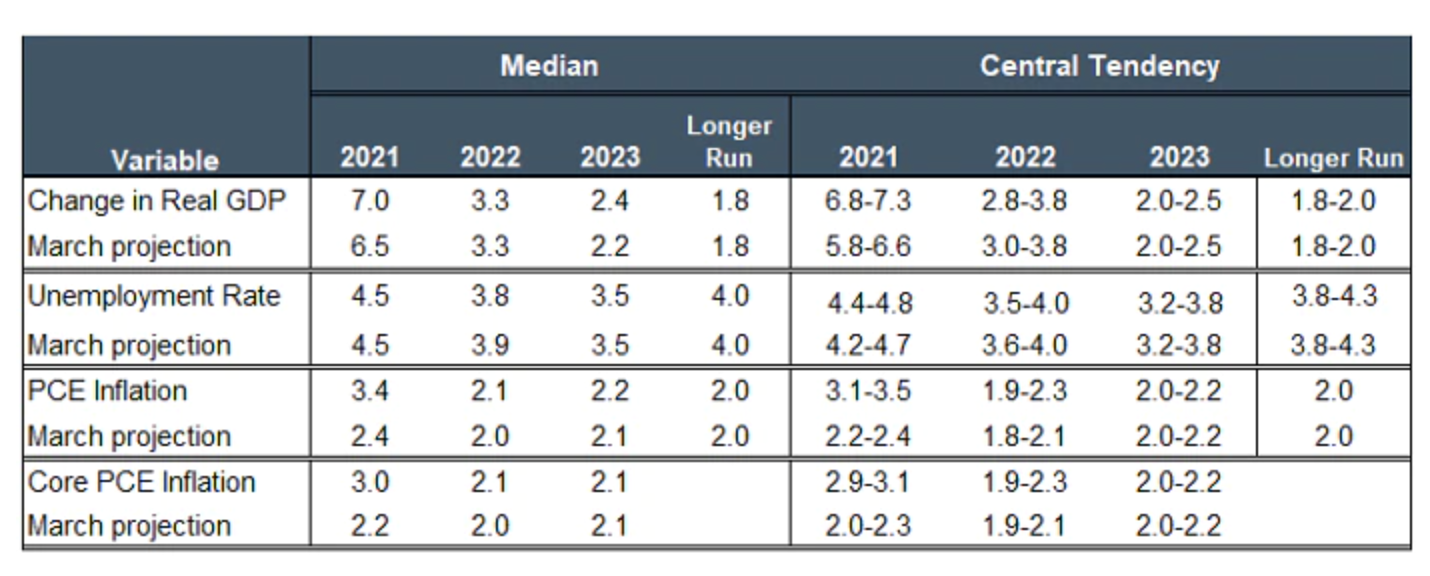

Fast forward through the shortest recession on record and the economy is rebounding strongly. The Fed’s economic forecasts for the end of 2021 show economic growth rising at a 7.0% pace, core inflation at 3.0%, and an unemployment rate of 4.5%.

Economic Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents

Source: Federal Reserve Board, as of 06/16/2021.

Notes: For each period, the median is the middle projection when the projections are arranged from lowest to highest. When the number of projections is even, the median is the average of the two middle projections. The central tendency excludes the three highest and three lowest projections for each variable in each year. The range for a variable in a given year includes all participants' projections, from lowest to highest, for that variable in that year. Longer-run projections for core PCE are not collected.

As the economic picture improves, it is not surprising that the Fed would start talking about scaling back its stimulus. Although it’s waiting for “substantial further progress” towards its dual mandate of an average inflation target of 2% and full employment, it looks like those benchmarks may be reached sooner rather than later, given its forecasts for 2021.

What is tapering?

Tapering is a term used to describe the process of gradually stopping asset purchases when there is no predefined end date or amount. Tapering does not involve the outright sale of Treasuries or agency MBS by the Fed—it only means reducing purchases to zero. The Fed likes to signal its intentions around tapering its QE program well in advance to minimize the impact on the markets. Although in the past, the prospect of tapering has unsettled markets, we expect it to be more orderly this time around, as the markets have been through the experience before. Nonetheless, it’s important for investors to understand the process.

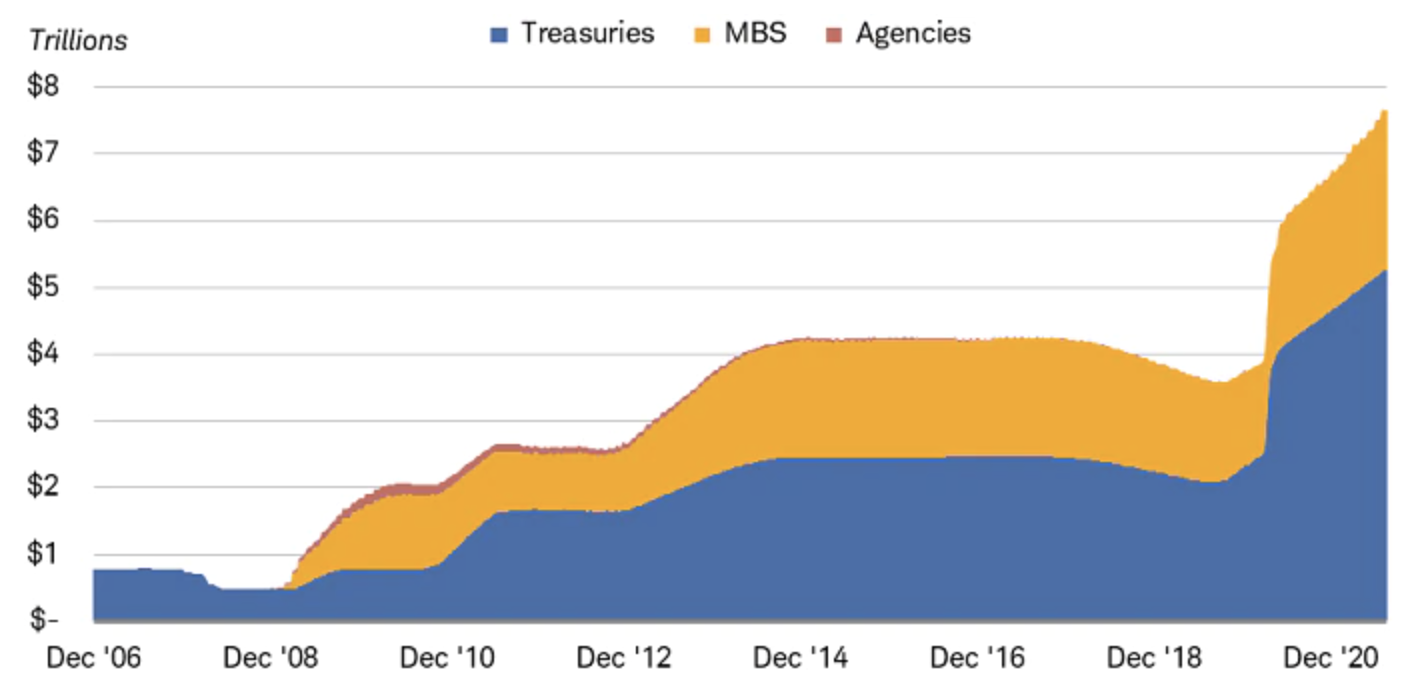

Now and then: The Fed’s balance sheet

The Federal Reserve initially implemented what some coined as “unlimited QE” in March 2020 before subsequently capping its monthly purchases at $80 billion and $40 billion for Treasuries and agency MBS, respectively. Ringing in around $7.7 trillion, the Fed’s current holdings of securities quickly blew past the prior peak seen after the 2007-2009 Great Recession. But that’s not the full story.

The Fed’s balance sheet has grown and changed

Source: Bloomberg. Federal Reserve Balance Sheet Securities Held Outright: Treasuries, Mortgage-Backed Securities, and Federal Agency Debt (FARWUST Index, FARWMBS Index, FARWUSFA Index). Weekly data as of 7/28/2021.

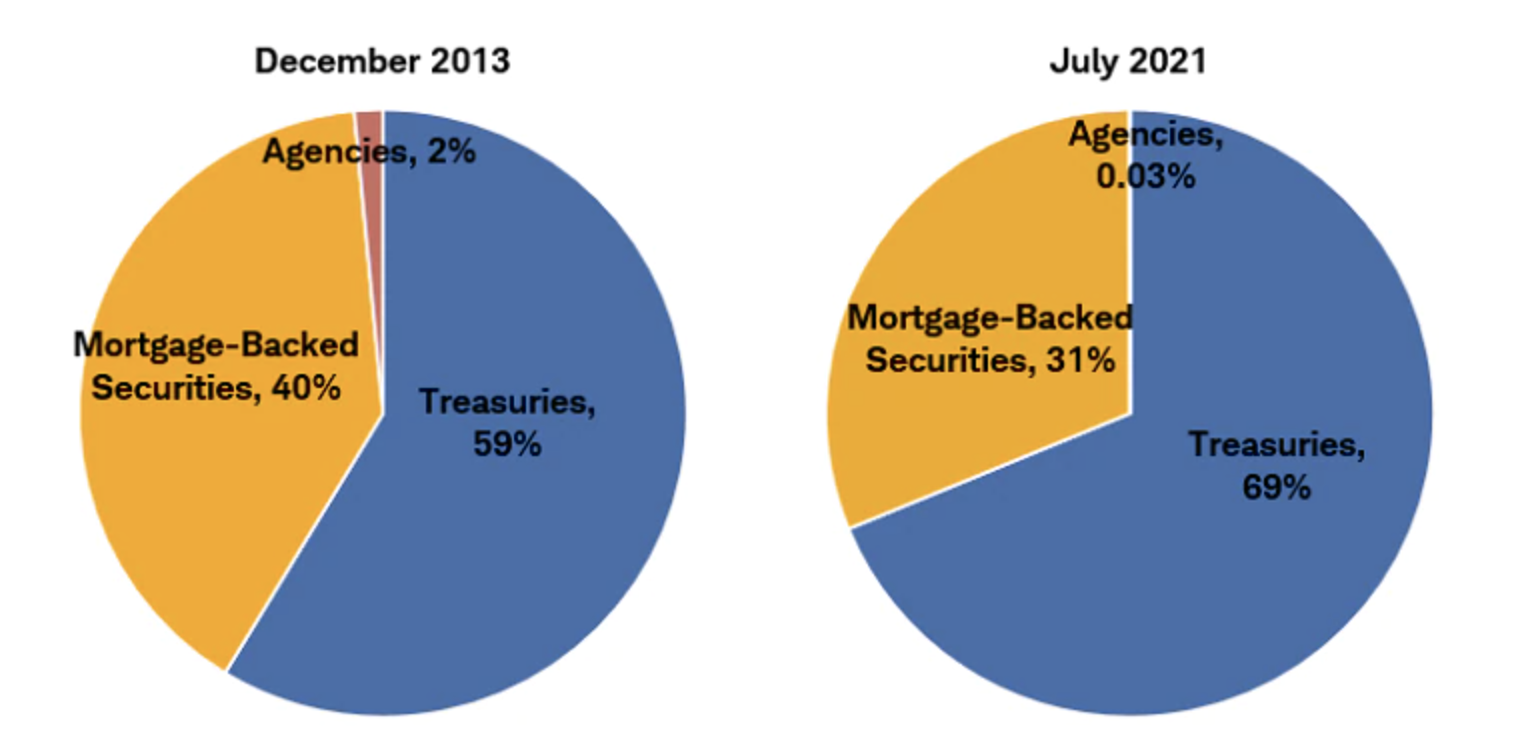

The composition of assets has shifted slightly, with the Fed holding a higher proportion of Treasuries compared to MBS this time around. Treasuries now comprise about 69% of the Fed’s holdings compared to 59% last time, and MBS holdings stand at 31% versus 42%.

The Fed’s balance sheet composition in 2013 vs. 2021

Source: Bloomberg. Federal Reserve Balance Sheet Securities Held Outright: Treasuries, Mortgage-Backed Securities, and Federal Agency Debt (FARWUST Index, FARWMBS Index, and FARWUSFA Index). Data as of 12/18/2013 and 7/28/2021.

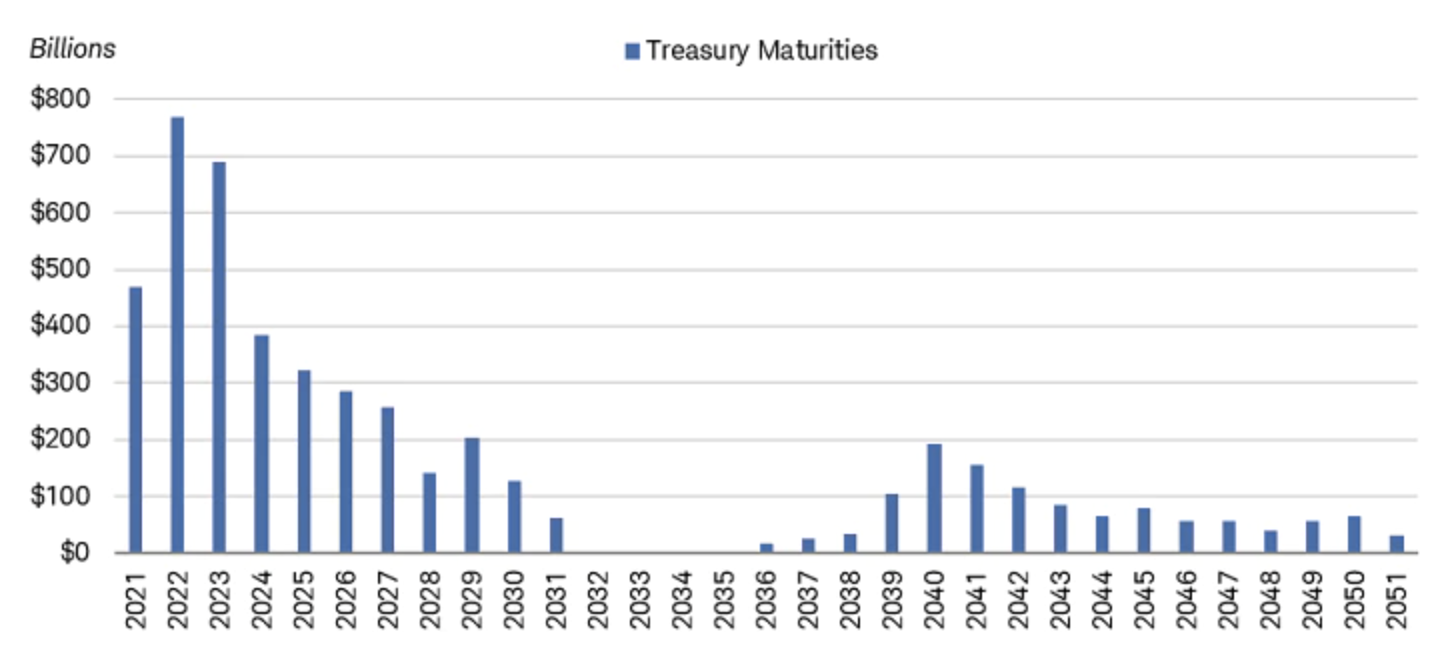

Another difference is that the bulk of the Fed’s holdings of Treasuries have shorter maturities, resulting in a weighted average maturity of 7.5 years versus 10.2 years previously.

The Fed’s balance sheet: Treasury maturity distribution

Source: Bloomberg. Maturity distribution of Federal Reserve SOMA Treasury Holdings. As of 7/28/2021.

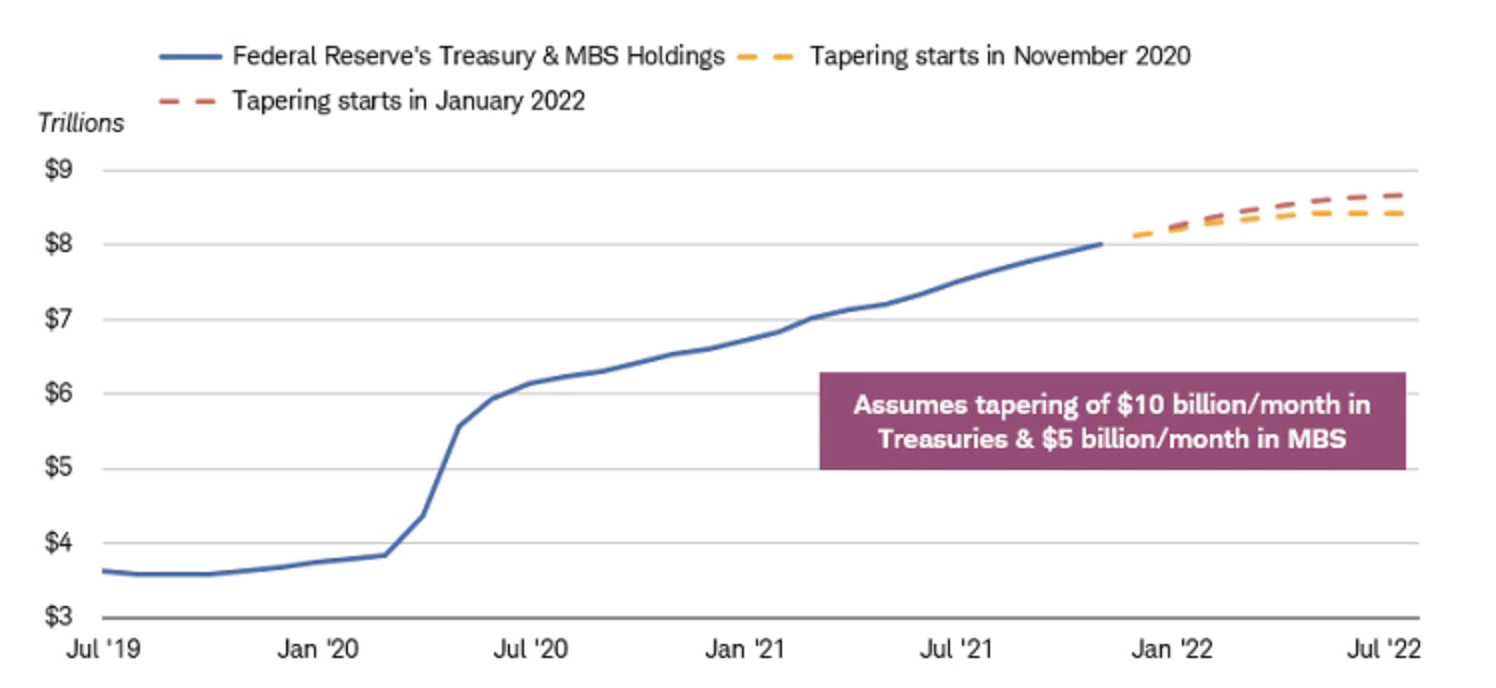

How long will tapering take?

Tapering is likely to be very gradual—in 2014 when the Federal Reserve tapered for the first time, it did so by decreasing monthly purchases by $5 billion per month for Treasuries and MBS each. The full tapering process took 10 months to complete. This time there has been some indication from Federal Open Market Committee (FOMC) members that they would like to move more quickly, as the economy has bounced back so fast. As a result, we forecasted two scenarios—tapering sooner and tapering later.

Tapering earlier vs. later

Source: Bloomberg. Federal Reserve Balance Sheet Securities Held Outright: Treasuries & Mortgage-Backed Securities (FARWUST Index, FARWMBS Index). Monthly data as of 7/30/2021.

In both scenarios, the balance sheet will likely stand around $8.5 trillion once tapering is complete. If the Fed starts tapering in November at $10 billion per month for Treasuries and $5 billion per month for MBS, tapering would be completed in about seven months, or by May 2022. On the other hand, if the Fed holds off until 2022 to start tapering by the same amount, it would be completed by July 2022. Although unlikely, the Fed does have flexibility to speed up or slow down the tapering process. Once completed, income received from the holdings will continue to be reinvested, growing the balance sheet at a much slower rate.

Given the expressed preference by some FOMC members to complete tapering sooner rather than later and the Fed’s forecast for the economy, we expect the Fed to announce it will begin tapering this fall, by slowing the pace of Treasury purchases by $10 billion per month and MBS by $5 billion per month. At that pace, tapering should take roughly seven months.

What does tapering mean for the markets?

In theory, tapering should lead to higher interest rates. By tapering its bond purchases, the Fed is increasing the supply that needs to be absorbed by the market and signaling that policy is becoming less accommodative. In practice, that hasn’t always been the result. We only have one previous example of tapering to look at, but the results were counterintuitive.

1. Treasury yields

Tapering doesn’t necessarily mean yields will spike higher. In the previous period of tapering, yields rose prior to the onset of tapering in 2013 but then fell during the implementation period. The pattern was similar to earlier periods when the Fed started and stopped QE. Yields rose during periods of QE and fell when QE ended.

10-year Treasury yields historically fell after tapering was announced

Source: Bloomberg, using weekly data as of 7/30/2021. US Generic Govt 10 Yr (USGG10YR Index). Shaded areas represent the periods of quantitative easing.

We believe this pattern reflects the power of the Fed’s signaling—it wasn’t necessarily the removal of the Fed as a buyer of Treasuries that caused yields to decline, but the signaling that did. Markets viewed ending QE and/or tapering as the start of tighter policy which would likely result in rate hikes down the road, slower growth, and less inflation. Consequently, yields fell, and the yield curve flattened.

It could always be different this time since yields for intermediate to long-term treasuries are already very low. However, it’s worth noting that the market reaction will depend more on the outlook for economic growth and inflation than on the level of treasury supply.

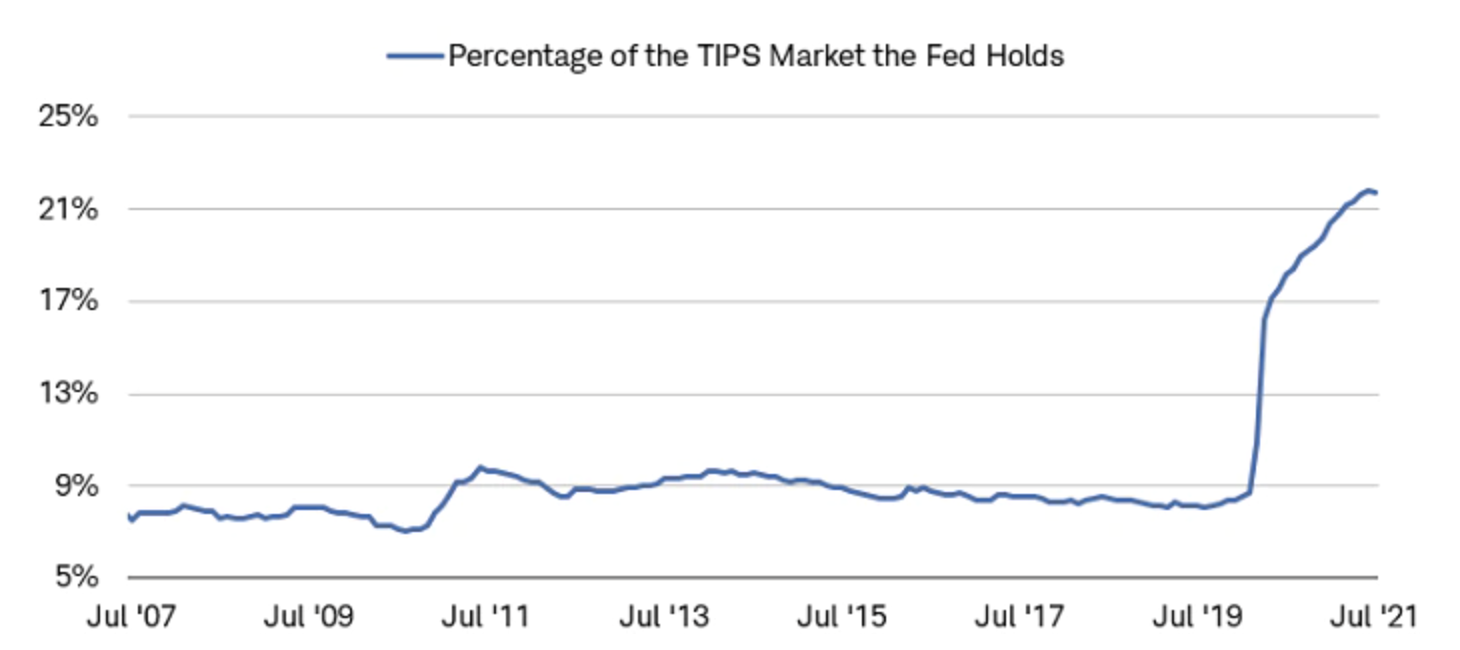

2. The TIPS market

The Fed has arguably had the most outsized impact on the Treasury Inflation Protected Securities (TIPS) market given the characteristically low level of supply in that market. The TIPS market is the only market where the Fed’s purchases decreased the overall supply of securities since initiating QE. Currently, the Fed holds 22% of the TIPS market.

The Federal Reserve holds 22% of the TIPS market

Source: Bloomberg. Federal Reserve's Percent of Ownership of the MBS Market (.FEDMBSIN G Index). Monthly as of 8/2/2021.

In 2014 when the Fed started tapering MBS purchases, MBS spreads narrowed, and yields declined. The decline in yields and narrowing of spreads in the MBS market resulted from the general improving of the housing market more so than the Fed tapering QE. Although MBS spreads could rise slightly this time around, it is likely that the tapering of MBS purchases will have a minor impact on the MBS market.

Is this time different?

Yes and no. If yields remain very low, the start of tapering may send them higher, reversing the pattern of the last round of tapering. It is also worth noting that we expect this round of tapering to be completed faster than the previous round of tapering in 2014.

However, since the markets and the Fed have experience with the process, we don’t necessarily expect a jump in Treasury yields or Treasury volatility. The key to the market’s reaction is based on how strong the economy looks at the time. Tapering is as much about signaling as it is about the implementation, and tapering signals that the Fed will have the flexibility to hike rates sooner rather than later.

What to consider now

If intermediate to long-term yields rise in anticipation of the Fed reducing its asset purchases, we suggest investors use that as an opportunity to increase the average duration in their portfolios. We have been suggesting keeping average duration low over the past year and would use a moderate rise in yields to add some longer maturity bonds to generate more income over time. A bond ladder strategy still makes sense to us in this environment, given the steepness of the yield curve.

Do not be surprised if there is an uptick in volatility for the riskier segments of the bond market. Over the past year, QE has provided an incentive for investors to take on more risk, and as asset purchases come to an end, it could spook the riskier segments of the market.

We always suggest investors check in with their Schwab representatives for a portfolio review to make sure they are prepared for increased market uncertainty.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All