Defensive stocks are often misunderstood. In recent years, even when they have delivered strong and steady earnings, returns have disappointed. Innovation often goes unappreciated. But we believe the disconnect between resilient businesses and share prices is unsustainable and ripe for reversal.

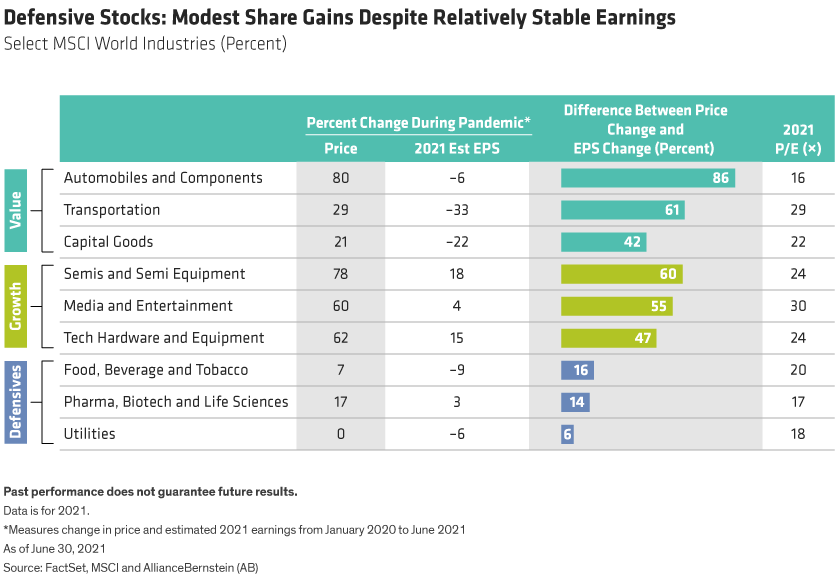

Since the beginning of 2020, the market has paid up for companies with strong sales growth. Share prices of companies in higher-growth industries and in some value industries have dramatically outpaced their earnings growth. Yet despite resilient earnings and attractive valuations, defensive companies have been left in the dust through the uncertainty of the pandemic—a time when their relatively stable businesses should have been prized (Display).

After a period of underperformance for defensives, a broadening market can represent real opportunity. Defensive sectors continued to grow earnings and cash flow during the period when the market chose not to reward them with higher prices. Simply put, there are some high-quality, defensive companies with stable businesses and cash flows that are currently available at very attractive prices.

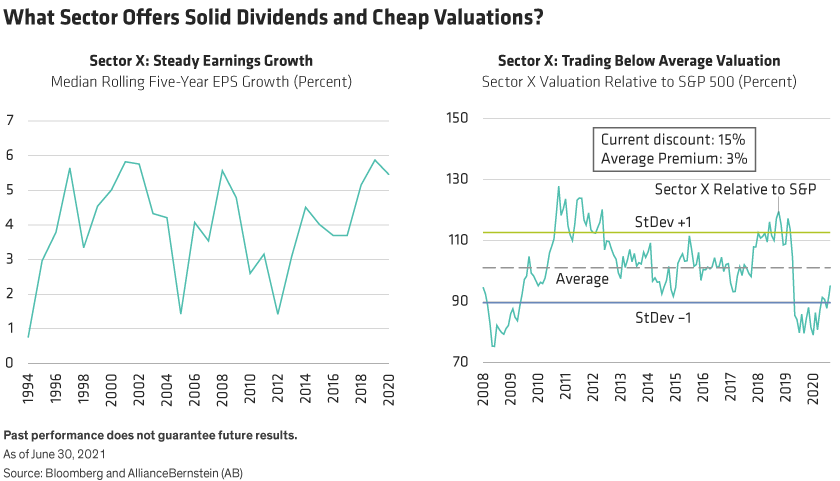

Sector X: Victim of Historical Bias?

Investors may be shunning sectors with attractive fundamentals because of preconceived notions, in our opinion. For example, consider a traditional defensive sector that we will call sector X. In this sector, average earnings and dividend growth are as strong as they have been in over a decade, around 5%. And that’s expected to continue for the foreseeable future. Yet the sector’s shares gained a paltry 0.5% in 2020 compared to a gain of over 18% for the S&P 500.

Earnings and dividend growth expectations for the mystery sector are historically high and expected to remain so for several years (Display, below left). And innovative companies in the group are growing even faster.

Most compelling trait? Its bargain-basement status. Sector X is trading at a 15% discount to the S&P 500 instead of its average 3% premium since 2008 (Display, above right). This sector underperformed the S&P 500 by 53% from March 9, 2020, to August 9, 2021—the worst relative peak-to-trough performance since the 1990s tech bubble. We think it may be time for a comeback.

So why have investors avoided a sector with consistent and improving characteristics like this? We think it’s because investors have focused primarily on hypergrowth companies, recovery plays and inflation beneficiaries, none of which fit this category. But in fact, we believe there are many exciting changes and themes going on under the hood of this underappreciated sector.

Utilities: Not Just a Bond Proxy Anymore

Sector X is, of course, utilities. Historically, our grandparents owned them for their defensive characteristics and dividends. Today’s investors might consider utilities to be boring bond proxies, especially when compared to high-flying media and technology pioneers. But we think the stereotype is overstated and there are several good reasons to take a fresh look at utilities today.

Utilities are the agents of change for the clean energy transition. As power-generating companies build out renewables as well as related transmission and distribution infrastructure, many benefit from tax incentives and continued political support to help states meet carbon goals. Renewables are also getting cheaper and, in wind’s case, more effective as technology improves. We believe the increased focus on climate change and reducing carbon emissions globally will deliver long-term benefits for utilities companies that are proactively positioned for the renewable energy revolution.

Politics aren’t a problem for this group either. The current bipartisan US infrastructure bill could be an upside for investments in transmission and renewables, and could perhaps even expand tax credits. Plus, the US wind corridor runs through mainly Republican states, so the technology build-out is likely to continue under any political constellation. And regulated utilities are protected from higher corporate taxes, too, as they are generally passed through to customers.

To invest in US utilities, however, selectivity is critical. For example, many utilities operating in wildfire-prone areas are a challenging investment at best. They are highly volatile and trade at steep discounts to peers. And even though many areas have laws protecting utilities from liability unless they are found negligent, they still sell off when wildfires occur. Equity investors should look for utilities with high-quality businesses and stable cash flows that trade at attractive prices, in our view. While it’s difficult to time when a change in sentiment toward utilities will develop, we believe the sector’s defensive properties combined with attractive valuation are rather compelling.

Beyond utilities, we believe that focusing on quality, stability and price is a good strategy for finding defensive stocks across sectors. In our view, active defensive portfolios based on these principles should have an advantage versus quantitative or passive approaches, which often include lower-quality businesses or expensive stocks. And by identifying innovators that are changing dynamics in diverse industries, investors can capture resilient return streams that also help reduce downside risk over time.

Kent Hargis is Co-Chief Investment Officer—Strategic Core Equities at AllianceBernstein (AB)

Sammy Suzuki is Co-Chief Investment Officer—Strategic Core Equities at AB

Ian McNaugher is Research Analyst—Strategic Core Equities at AB

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein