The ECB has used quantitative easing aggressively in recent years to support the euro-area economy, banks and asset prices. It currently has in place two separate programs with quite different purposes:

The Asset Purchase Programme (APP), first introduced in 2014 and restarted in September 2019, aims to reinforce the ECB’s negative interest rates and help counter downside risks to price stability. The APP purchases €20 billion a month and is due to end “shortly before” the ECB starts raising interest rates.

The PEPP, launched in March 2020 to counter downside risks to the inflation path caused by the COVID-19 pandemic, differs from the APP in two important ways. First, the monthly purchase pace is flexible and secondary to the program’s main aim: preserving “favorable financing conditions.” To this end, the ECB raised the pace from €60 billion in the first quarter to €80 billion in the second and third quarters, and aims for a “moderately lower” pace in the fourth quarter. The second difference from the APP: the PEPP is meant to last only so long as the pandemic weighs on the inflation path.

What Will It Take to Wind Down the PEPP?

So, when will the ECB be able to conclude that the crisis phase is over?

Although the coronavirus delta variant has clouded the outlook somewhat, the economy has improved rapidly in recent months, and the ECB should have sufficient information by its December meeting to confirm that the PEPP will expire next March. Indeed, the central bank’s September forecasts suggest a fading need for emergency monetary stimulus:

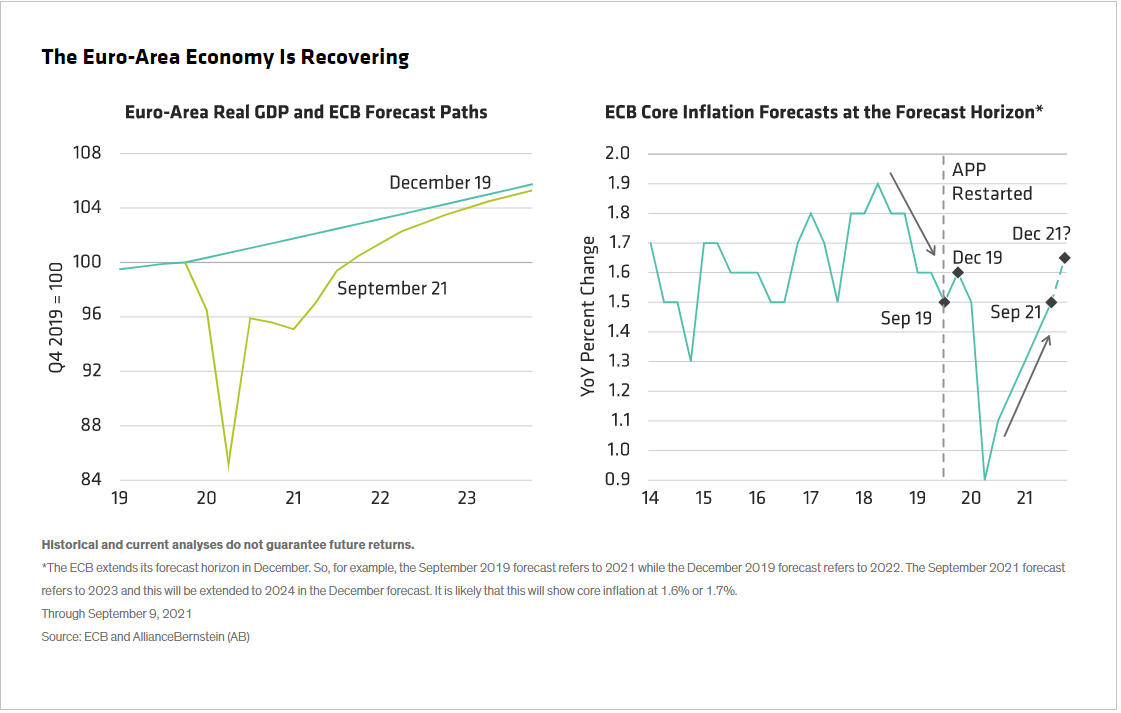

- The ECB expects the level of output to rebound to near its pre-pandemic path in coming quarters (Display below, left) and the output gap to close in 2023.

- Core inflation is expected to reach 1.5% in 2023. That’s the same level as the ECB’s September 2019 forecast for 2021 core inflation, but the trajectory is very different—inflation is now rising instead of falling (Display, right).

But the economic revival doesn’t mean the ECB will cease its asset purchases altogether. With inflation still far from target, a rate hike is still several years away, so the ECB is likely to be buying bonds via the APP for some time to come.

Recalibrating the APP Purchasing Pace

Predicting how the ECB will set the APP purchase volume once the PEPP has expired is more difficult.

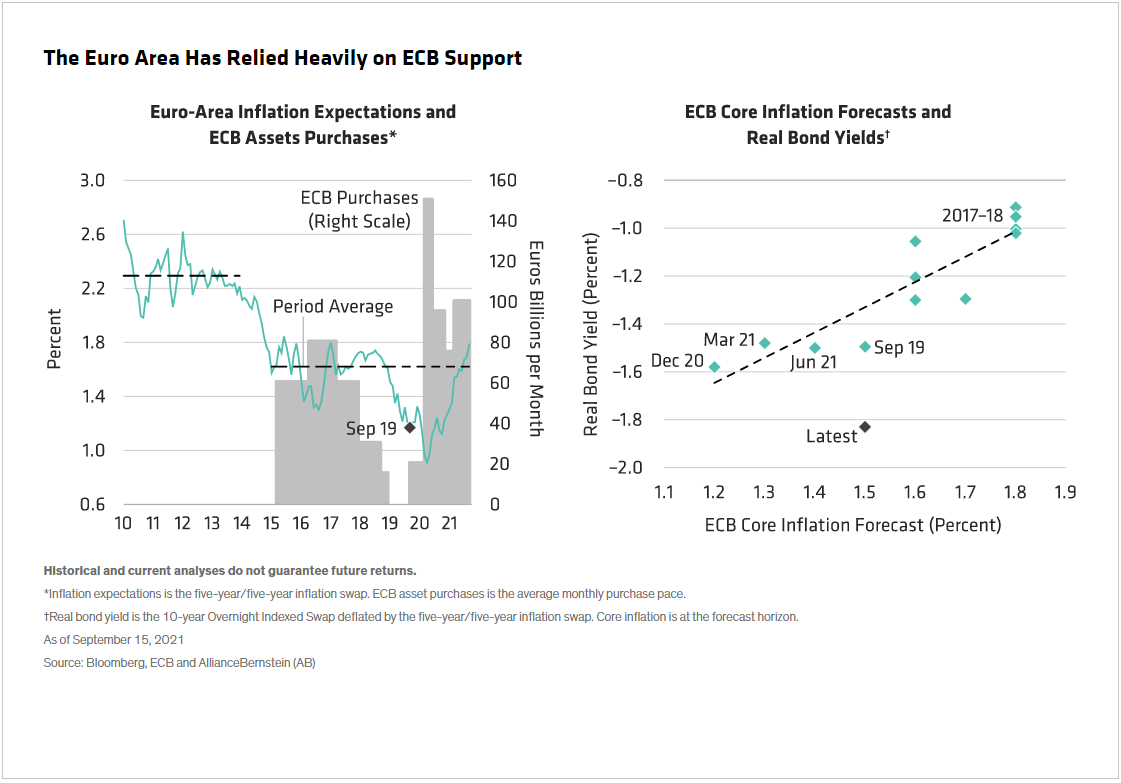

One possibility is to use September 2019 as a benchmark. When the ECB restarted the APP in 2019, the economy was slowing, risks were tilted to the downside and the central bank had lowered its 2021 core inflation forecast to 1.5% from 1.8% at the beginning of the year. Today, the economy is accelerating, risks are seen as broadly balanced and the ECB has raised its 2023 core inflation forecast to 1.5% (from 1.2% at the beginning of the year). Inflation expectations are also well above September 2019 levels: at 1.75%, the five-year/five-year forward inflation swap is roughly 50 b.p. higher.

Based on these numbers, it’s hard to make the case for a higher APP pace than in September 2019. But a lot has changed in two years. Not only has the ECB raised its inflation target to 2.0% and formalized the target’s symmetrical nature, but it has also stressed the need for monetary policy to be more “persistent” when interest rates are near the effective lower bound. The Governing Council has also shifted the PEPP’s focus away from the volume of purchases and toward preserving favorable financing conditions.

The Era of Fiscal Dominance Has Arrived

A final consideration in the policy path is the size of fiscal deficits. In 2019, the euro area was running a budget deficit equal to 0.6% of GDP, and the ECB expected a deficit of 0.8% (just short of €100bn) in 2020; last week, the ECB forecast a 3.0% deficit (about €390bn) for 2023. As ECB Chief Economist Philip Lane recently noted: “you cannot think about the volume of the APP independently of the volume of net bond supply”—a statement that runs perilously close to an admission that fiscal dominance has arrived.

Implications for Financial Markets

So where does this leave us?

Comparing economic conditions today with those in September 2019 would point to a significant reduction in the pace of ECB asset purchases next year (back to €20 billion a month). But the continued inflation shortfall relative to target, the need for persistence and the risk of spooking the bond market all call for a more gradual adjustment (to, say, €40–50 billion a month).

There are other reasons for caution. Not only does the potential for spread widening in noncore euro-area countries put the ECB in a unique position among central banks, but it’s also worth noting that inflation expectations fell away quickly the last time the Governing Council sought to wind down its asset purchases (Display left, below).

We also see strong arguments for making the pace of APP purchases flexible and contingent upon the delivery of appropriate financing conditions (in other words, a form of soft yield-curve control). But whichever path the ECB chooses, the key point is that the economic backdrop is improving. That doesn’t mean the ECB will turn hawkish or abandon its commitment to highly accommodative monetary conditions—after many years of failing to deliver on its price-stability mandate, the inflation outlook is still far too weak for that.

But it does mean the level of bond yields required to deliver appropriate financing conditions is starting to rise (Display above, right chart). And as the Governing Council becomes more confident in the economic outlook, it is likely to become increasingly relaxed about a modest backup in yields. We continue to see 10-year Bunds moving into a –0.25% to 0.00% range over the next few months and into a slightly higher range beyond that (i.e., 0.00% to 0.50%).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein