The debate about inflation is a key concern for investors today. Will it be persistent or transitory, with inflationary pressures fading after supply chains normalize?

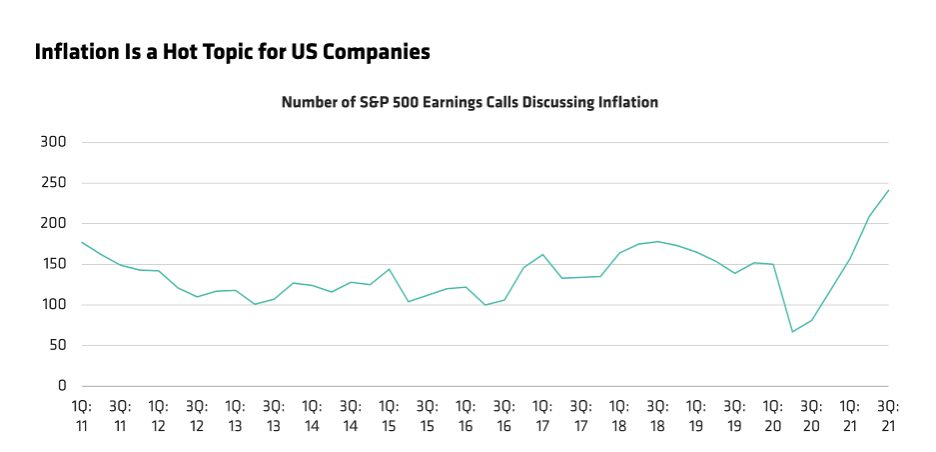

We believe insight offered from recent quarterly earnings calls lends credence to inflation remaining an issue, at least in the coming quarters. Almost half of the management teams of S&P 500 companies mentioned cost pressures during their second-quarter reviews—more than any time in the last 10 years (Display).

Current analysis does not guarantee future results.

As of August 26, 2021

Source: AlphaSense and AllianceBernstein (AB)

Mentions of inflation on US corporate calls have increased almost 200% over last year and 73% versus pre-pandemic levels of 2019. Many companies have managed through these inflationary pressures so far with solid revenue growth and some avoided costs. But, as GDP growth normalizes and some previously avoided corporate expenses return, inflationary pressures could harm earnings.

What’s the solution? In our view, successful companies must have pricing power as an arrow in their business quiver to effectively navigate this inflationary wave. While pricing power has always been important, in today’s environment, it has become critical.

From Technology to Transport

Technology companies with ubiquitous programs or services are among those able to raise prices, in our opinion. Payment processing and software firms that haven’t increased their rates recently, for example, aren’t likely to receive much pushback should they take pricing action. The two most dominant payment processers globally, Visa and Mastercard—both classified as technology companies—are engaged in approximately 75% of all credit and debit card purchases, and the business continues to grow. They’ve both delayed price increases through the pandemic, but have announced intentions to raise prices in 2022.

Microsoft has reinvented itself under CEO Satya Nadella, transforming into a software-as-a-service and cloud company. Over a million companies worldwide use Office 365, accounting for over 200 million individual users. The price of the subscription has remained static since 2014, but Microsoft recently announced it will increase prices in March 2022.

Transportation companies are another cohort willing and able to increase prices. Supply chains disrupted by pandemic lockdowns are now attempting to catch up with surging demand. Not only are ports swamped with containers, but there aren’t enough truck drivers available to meet the need. Some transportation companies can charge 3–4 times what they did a year ago for premium freight. Other shippers are breaking fixed-price contracts to capture higher market rates because they can. In fact, increased costs and supply line delays have caused one large retailer to directly lease ships and containers to bring goods to market without delay, rather than relying on freight companies.

The pandemic also changed consumers’ behaviors, wants and needs. While trapped at home, US consumers accumulated cash from the fiscal stimulus and paid down debt. After more than a year and a half without travel, limited entertainment and shortages of everything from yeast to toilet paper, many consumers are willing to pay for what they want, whether it is a better experience, higher-quality goods or tastier chocolate. So, retailers that can deliver a truly differentiated shopping experience and higher-quality merchandise will be well positioned to raise prices. Nestlé, for example, believes it will succeed at passing higher food commodity prices on to consumers globally over the next two years.

Providing convenience might also allow for pricing power. In the construction business, for example, few contractors want to own and maintain heavy equipment. Equipment rental firms such as UK-based Ashtead can not only handle the burdens of ownership but have found that, as its fleet becomes greener, customers are willing to pay higher rents.

The Other Side of the Inflation Coin

On the other hand, for some firms, higher costs could dent earnings. Being able to avoid investments in companies that may underperform in an inflationary environment could be just as valuable as the knowledge as to which have better prospects.

Multiple firms, for example, have noted increased labor costs when an Amazon distribution center opens nearby—if companies can find workers at all. And, while sign-on bonuses aren’t unusual in professional services firms, surely no one saw them coming for fast-food staff.

Previously discussed higher transportation costs must be absorbed somewhere down the food chain, whether by manufacturers or end consumers. Burlington Stores customers, for instance, are less willing to pay increased prices for goods, so higher transportation costs have been noted by management as impacting margins.

Similarly, construction materials have increased approximately 20% on average in some locales, while contractors have indicated they believe they can only raise prices about a quarter of that. More specifically, the producer price index for milled steel products increased 123 percent over last August—woe unto any company with a need for it in their production or manufacturing process if they don’t have pricing power!

Pricing power is always valuable, but perhaps never more so than during inflationary periods. Companies that can’t pass increased costs on face margin compression or worse. Understanding a firm’s pricing power, whether from competitive advantages, differentiated offerings or experiences, or constrained capacity is imperative to developing high conviction in specific stocks.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

References to specific securities are presented to illustrate the application of our investment philosophy only and are not to be considered recommendations by AB. The specific securities identified and described do not represent all of the securities purchased, sold or recommended for the portfolio, and it should not be assumed that investments in the securities identified were or will be profitable.

© AllianceBernstein

Read more commentaries by AllianceBernstein