There is a cost to waiting for interest rates to rise—you may be missing out on higher coupon rates and yields elsewhere. Rather than waiting on the sidelines for yields to rise, investors should consider short-term corporate bonds today—specifically those with fixed coupon rates.

Short-term corporate bonds offer higher yields than many other short-term alternatives

It might be tempting to hold investment funds in cash or cash-like investments, such as money market funds, while you wait for interest rates to rise. While cash always has a place in well-diversified portfolios, we caution against holding cash as a proxy for fixed income, as it is a potential drag on total returns.

To be clear, we are not suggesting investors shift their traditional cash positions, like those needed for daily liquidity or near-term expenses, into short-term, fixed-rate corporate bonds. Rather, we’re targeting funds that would or should be allocated to fixed income, based on an investor’s strategic asset allocation mix, but instead is sitting in cash because bond yields are so low. Short-term investment-grade corporate bonds come with higher risks than cash or money market funds, like more credit risk and interest rate risk, but overall those risks are relatively low.

Short-term investment grade corporate bonds offer a yield advantage over Treasury bills

Source: Bloomberg, as of 10/5/2021. Bloomberg U.S. Corporate 1-5 Year Bond Index (LDC5TRUU Index), Bloomberg U.S. Treasury 1-5 Year Index (LTR1TRUU Index), Bloomberg U.S. Floating-Rate Notes Index (BFRNTRUU Index) and the Bloomberg U.S. Treasury Bills 1-3 Month Index (LD12TRUU Index). Past performance is no guarantee of future results.

For those tactically waiting for rates to rise before investing in bonds, there is a cost to that strategy: the opportunity cost of compounding the higher yields that are available today in other high-quality investments. While the yields shown above are low by historical standards, the nearly 1% yield advantage that investment grade corporate bonds offer over short-term Treasury bills can’t be ignored.

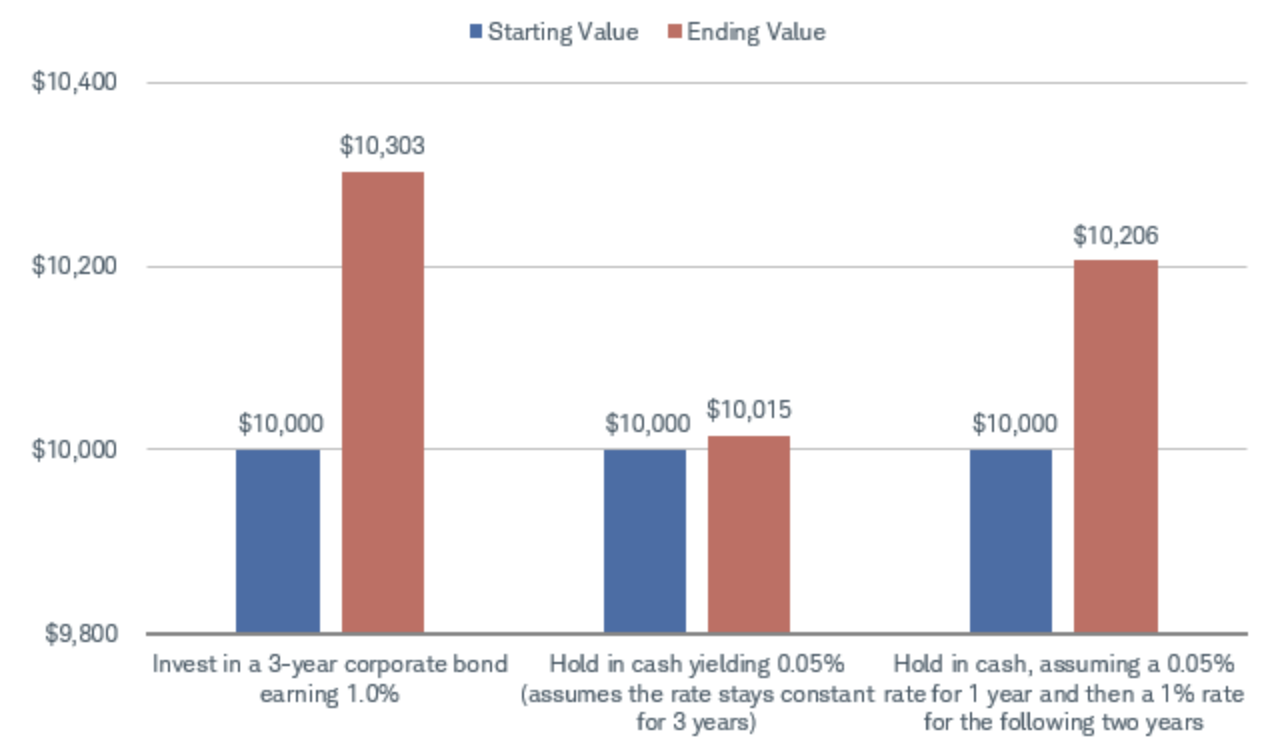

In this example below, note that the column on the right assumes a 1% interest rate in just one year, which is still well below market expectations of where the federal funds rate likely will be at that time.

There is a cost to waiting for rates to rise

Source: Bloomberg. Hypothetical scenarios using the yield on a 3-month Treasury bill of 0.05% and the yield-to-worst of an average 3-year corporate bond of 1.0%. The third scenario assumes the Fed funds rate is increased to 1% in year two, resulting in 3-month Treasury bill yield of 1.0%. For illustrative purposes only.

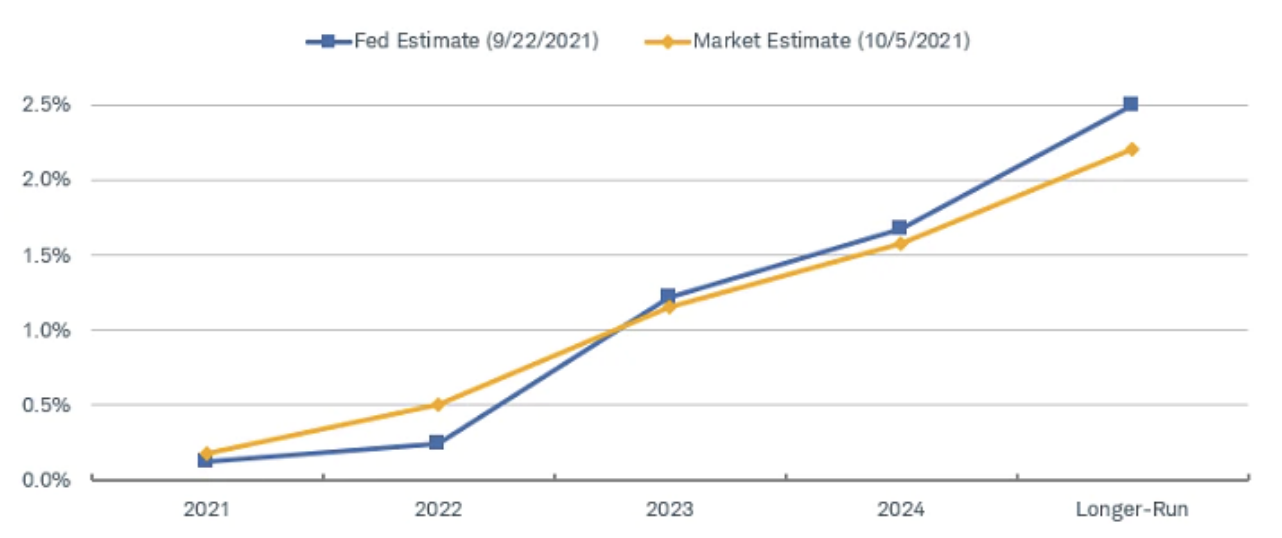

The Federal Reserve is likely to keep rates near zero for at least another year. The federal funds rate remains in its zero to 0.25% range, and it’s expected to stay there until the end of 2022, if not later. Based on projections from the Federal Open Market Committee, participants are split on whether the first rate hike likely will come in 2022 or 2023, while markets are pricing in a 25-basis-point rate hike by the end of 2022.1

It’s not just the first rate hike that matters, but the pace. The federal funds rate isn’t expected to get to 1% or higher until late 2023. The longer the Fed remains on hold, the longer investors sitting in cash may miss out on the higher yields that other investments offer.

The federal funds rate isn’t expected to hit 1% until late 2023

Note: The “forward curve” represents future interest rates implied by the market for interest rate swaps. Market estimate for "Longer Run" represents the Euro Dollar Synthetic Rate for December 2027.

Source: Bloomberg. Fed estimate as of 9/22/2021. The market estimate of the federal funds using Eurodollar futures (EDSF). As of 10/5/2021.

Consider fixed-rate over floating-rate corporate bonds

Now that you’re considering short-term corporate bonds—after all, you’re still reading this article—we prefer fixed coupon rates over floating coupon rates.

First, short-term, fixed-rate corporate bonds offer yields that are currently three times as high as floaters on average. The average yield-to-worst of the Bloomberg U.S. Corporate 1-5 Year Bond Index is roughly 1%, compared with just 0.3% for the Bloomberg U.S. Floating Rate Notes Index.2 We compared these indexes since they both have similar average maturities of between 2 and three years.

The yield on the one-to-five-year index has risen modestly lately as the market has begun to price in sooner-than-expected rate hikes. The three-year Treasury yield, for example, is over 0.5% today, compared with 0.3% or so just a few months ago. The three-year Treasury yield tends to fluctuate based on expectations of when, and how quickly, the Federal Open Market Committee will raise rates.

Floater coupon rates are indexed to short-term reference rates that are tied much more closely to the federal funds rate and are unlikely to rise until the Fed begins to hike rates, which is likely a year or more away.

Short-term corporate bonds offer higher yields than floaters

In the meantime, floater investors are earning less income until the Fed starts to hike rates, which can weigh on total returns. We believe the Fed could begin hiking rates as early as late 2022, but we don’t know for sure. The longer the Fed remains on hold, the longer floater investors are missing out on higher yields available elsewhere.

Leading up to—and even during—the Fed rate hike cycle that began in 2015, short-term fixed-rate corporate bonds outperformed the floating-rate notes index.

Short-term fixed-rate corporate bonds outperformed floaters leading up to, and during, the last Fed rate hike cycle

There are benefits to owning floaters, like their relatively stable prices compared to fixed rate corporates. But those stable prices come at a cost of lower yields and likely lower total returns.

Finally, keep in mind that any type of corporate bond—either fixed or floating—comes with risks, like the risk that a deteriorating economic outlook can weigh on their values. Overall, we believe that these risks are relatively low today, as corporate profits are rising and balance sheets are generally healthy.

What to do now

Don’t just wait for yields to rise by holding investments that yield nearly nothing. Short-term investment-grade corporate bonds offer higher yields than many other ultrashort-term alternatives, but also have relatively low interest rate risk.

Short-term corporate bonds with fixed coupon rates appear more attractive than floaters today. Schwab clients considering short-term investment grade corporate bonds that prefer to use mutual funds or exchange-traded funds (ETFs) can use the ETF screener or mutual fund screener. When using both screeners:

- Search for bond funds under the “Short-Term Bond” category, as the more traditional “Corporate Bond” fund category likely won’t capture funds with short-term average durations.

- Use the left-hand side of the page to select “Average Effective Duration” as a screen criteria, which will allow the fund’s average duration to be showcased in the screen results.

- Once the results are listed, look for mutual funds or ETFs that focus on corporate bonds.

If you’ve been waiting on the sidelines to invest in higher yields, we’d ask “what are you waiting for?” and “if you are waiting, what are you earning while waiting?”

1 One basis point is equivalent to 0.01% (1/100th of a percent). A 25-basis-point change is equivalent to 0.25%.

2 As of 10/4/2021

Important Disclosures:

Investors should consider carefully information contained in the prospectus or, if available, the summary prospectus, including investment objectives, risks, charges, and expenses. Please read it carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Money market funds: An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the fund.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(1021-1R0J)

© Charles Schwab

Read more commentaries by Charles Schwab