Schwab Sector Views: What if Inflation Persists?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSchwab Sector Views is our three- to six-month outlook for stock sectors, which represent broad sectors of the economy. It is published on a monthly basis and is designed for investors looking for tactical ideas.

Signs are growing that inflation may be more tenacious than originally expected. We don’t believe a return to 1970s-style inflation is likely, but there is a worrisome scenario in which persistently sharp increases in prices could be a factor to reckon with—and if history is any guide, they could have an impact on sector performance.

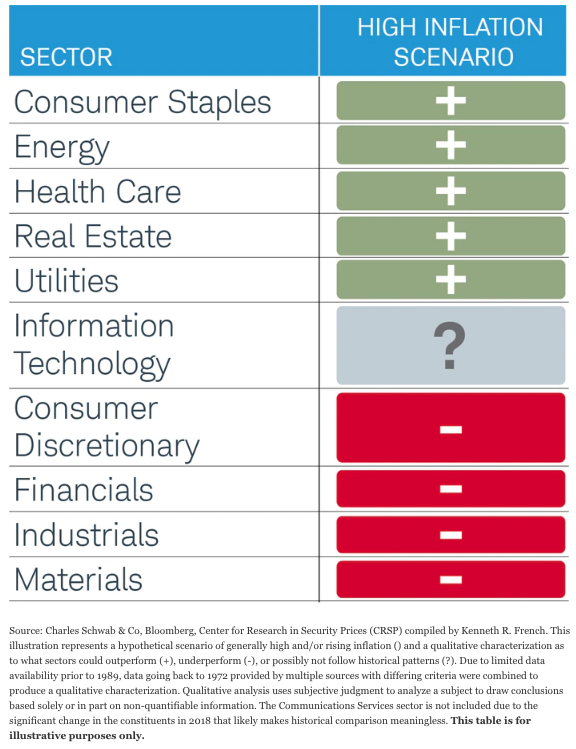

In every market environment there tend to be winners and losers, and inflationary periods are no exception. When inflation is stubbornly high, sectors such as Energy, Real Estate, Health Care, Utilities, and Consumer Staples historically have outperformed on average. Others such as Consumer Discretionary, Industrials, Materials and Financials have struggled in general.

Of course, there are always extenuating circumstances that make every inflationary cycle different. The lopsided impact of the COVID-19 pandemic could alter some historical patterns. For example, Information Technology historically has struggled when inflation was high and rising. However, technology has become so integral to daily life and the overall economy—more so during the pandemic, when working remotely, shopping online, and streaming entertainment became ubiquitous—that the sector may react differently to high inflation going forward.

To be clear, we don’t think that we are currently in the more dire inflationary scenario, but the market might periodically reflect investors’ worries that we are going down that path—so let’s take a look at how various sectors might perform, and why.

Hypothetical sector relative performance during a period of high inflation

Sectors that may benefit from higher inflation

1. Energy: In the early stages of an inflationary cycle, Energy typically benefits from the same factor that drives overall prices higher: demand that outstrips supply. OPEC usually acts to support oil prices, as it’s doing now, only incrementally returning supply to the market after sharp cuts during the COVID-19 crisis and the plunge in oil prices. Although many energy companies are likely to ramp up production quickly now that oil and natural gas prices are at very profitable levels, the International Energy Agency (IEA) estimates that supply will not match demand until sometime next year. Meanwhile, logistical and geopolitical roadblocks to increasing natural gas supplies could take some time to resolve. Historically, the Energy sector has often been one of the top relative performers when inflation in on the rise—at least until the Federal Reserve tightens monetary policy enough to slow economic growth, or excess supply causes prices to drop.

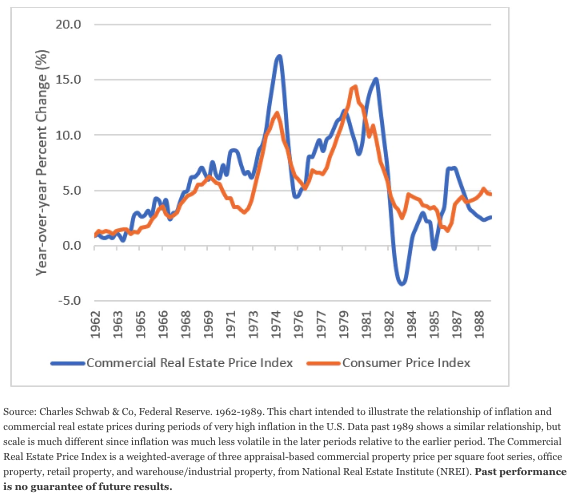

2. Real Estate: Rising inflation usually reflects an improving economy, which tends to be good for the real estate investment trusts (REITs) that make up the bulk of the Real Estate sector. Office buildings and retail shopping centers experience greater demand for space and can charge higher rents when economic growth is strong. It’s true that the rising interest rates that typically occur with inflation can be a headwind for the Real Estate sector, which relies heavily on borrowing. However, commercial real estate prices also tend to rise, providing a positive counterbalance—this is particularly true when the rate of inflation is high relative to interest rates (i.e., when “real,” or inflation-adjusted, interest rates are low) and the economy is growing, as is the case now.

The pandemic has changed the way people work and shop, leading to uncertainty for office and retail REITs, in particular. It’s not clear whether household migration out of major city centers will be sustained, how many workers will continue to telecommute, and how effectively shopping malls—which were already in decline prior to the pandemic—will compete with online retailers going forward.

However, the high demand for e-commerce warehouses, telecommunication infrastructure, and cloud computing data centers may be enough to provide solid underpinnings for the commercial real estate portion of the sector. For residential REITs, the massive fiscal and monetary stimulus efforts combined with extremely low interest rates, materials shortages, and work-from-home dynamics, are resulting in a boom in house prices, which is likely to continue to push single- and multifamily rents higher.

Commercial real estate prices typically rise with inflation

3. Traditionally defensive sectors—Health Care, Utilities and Consumer Staples: These sectors tend to outperform during periods of high inflation. In part, this is due to their relatively steady earnings no matter the economic conditions—people need medicine, heat, and food in any economy—and their ability to pass higher costs on to consumers.

- While Utilities could face short-term headwinds from higher energy prices, regulators typically allow them to pass higher gas and electric costs on to consumers, enabling them to maintain profit margins. However, clean-energy regulations and currently poor valuations could lessen some of the sector’s defensive characteristics, particularly if companies don’t receive substantial federal government subsidies for switching away from fossil fuels.

- The Health Care sector faces risk from potential prescription drug price controls. However, it should benefit from strong longer-term fundamentals, like growing demand in emerging markets and aging populations that typically require more health care services, as well as currently attractive valuations and strong balance sheets.

- In high-inflation environments, industries within the Consumer Staples sector—including makers of household goods and supermarkets—often can raise prices to offset higher input costs. Some of the biggest companies within the sector, particularly big-box discount retailers, can benefit from cost-conscious shoppers shifting their buying habits. Although the current supply-chain constraints are a significant problem for many of these retailers, the largest companies—like Walmart and Costco—have navigated the shipping backlog by chartering ships and moving product with their own trucks and workers, albeit at a high price.

Sectors that may struggle amid higher inflation

1. Consumer Discretionary: This sector, which includes business lines ranging from apparel and automobiles to home improvement and internet retailers, is a favorite punching bag when it comes to inflation—and rightfully so. As the script goes, higher energy costs and reduced purchasing power due to higher prices in general eat away at nonessential consumer spending, especially for lower-income consumers. However, there are currently some mitigating circumstances. Unlike past eras, energy on average accounts for only about 4% of disposable income—half of the level in the early 1980s—so price increases may not have a significant impact. And wages are rising fast—particularly for the lower-paid service workers in the leisure & hospitality and retail industries—taking the sting out of higher overall inflation. Additionally, household finances are relatively healthy, and banks are eager to lend at attractive interest rates.

In terms of fundamentals for businesses in the sector, supply constraints are affecting sales and production, with the auto industry being one of the hardest-hit by the semiconductor shortage. Meanwhile, many companies within the Consumer Discretionary sector are facing higher costs—in large part due to surging shipping costs, wholesale prices, and wages. So far, many are having some success in passing along higher costs to consumers amid strong demand, thereby protecting profit margins. However, if the economy slows, the Fed tightens monetary policy because of mounting inflation concerns, and/or market volatility picks up, this cyclical sector could underperform, as it has historically done during periods of higher inflation.

2. Financials: The sector’s initially positive reaction to higher prices and accompanying rise in interest rates tends to fade when inflation rises sharply. At first, the growing economy behind rising inflation is good for banks and other Financials industries, as it spurs loan demand and lowers credit defaults. This can be true even as the Fed begins to intervene to slow inflation by raising short-term interest rates. However, the picture changes if inflation continues to rise at a fast pace and the Fed’s policy becomes much more restrictive to counteract it. In the simplest terms, banks borrow at short-term rates (the rates they pay depositors) and lend at longer-term rates. When the Fed raises short-term rates aggressively, it typically leads to expectations for slower economic growth that can drive long-term rates lower, resulting in lower net interest margins and potentially weaker relative performance for Financials. Stronger-than-usual balance sheets currently could mitigate the headwinds if a more dire scenario were to play out, but likely not enough to thwart underperformance.

3. Industrials: Relative performance of this sector historically has been weak during periods of high and rising inflation. Companies typically face challenges from higher input costs along with ebbing demand for cyclical products such as construction equipment and industrial machinery. Current supply constraints, high labor costs, and the spike in fuel costs are all headwinds for the sector, particularly for heavy fuel users and labor-intensive industries such as airlines, package delivery, and transport industries. On the plus side, inventory rebuilding and the backlog of product deliveries could benefit the sector once supply bottlenecks have cleared.

4. Materials: Although the Materials sector typically gets support early in an inflationary cycle as global growth and demand remain strong, concerns about slowing economic growth can take a toll. The recent slowdown in Chinese growth could mean that Materials stocks would struggle even earlier and to a greater degree than usual.

One sector may perform differently this time

Information Technology: This sector historically performed poorly when inflation was high, owing to its previous cyclical nature. In the past, consumer and business spending would decline when higher inflation and/or Fed rate hikes slowed economic growth. However, the sector has become less cyclical in recent years, likely due to the evolving nature of demand for Information Technology equipment and devices. As seen during the COVID-19 crisis, demand for technology increased amid the decline in economic growth. While that was a unique event, consumer electronics have become integral to social interaction and entertainment. Meanwhile, businesses must invest in technology to remain competitive, as well as increase productivity to counteract labor shortages and higher wages. While the sector has extremely high valuations, its historical underperformance might not repeat itself if inflation does turn out to be persistent.

Bottom line

Every economic and inflation cycle is different—particularly so now with the unprecedented COVID-19 impact. We don’t think that we’re on the cusp of lasting inflation, but the market may periodically react as if we are. Even if we’re wrong and inflation continues to charge sustainably higher, the same principles apply—keep any tactical sector tilts small and remain diversified within U.S. equities, just as you should across all asset classes.

What do the ratings mean?

The sectors we analyze are from the widely recognized Global Industry Classification Standard (GICS®) groupings. After a review of risks and opportunities, we give each stock sector one of the following ratings:

- Outperform: likely to perform better than the broader stock market*

- Underperform: likely to perform worse than the broader stock market*

- Neutral: no current view on likely relative performance

* As represented by the S&P 500 index

Important Disclosures:

Schwab Sector Views do not represent a personalized recommendation of a particular investment strategy to you. You should not buy or sell an investment without first considering whether it is appropriate for you and your portfolio. Additionally, you should review and consider any recent market news.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Diversification and asset allocation do not ensure a profit and do not protect against losses in declining markets.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

All corporate names are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

The policy analysis provided by the Charles Schwab and Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Real Estate Investment Trusts (REITs)- Risks of REITs are similar to those associated with direct ownership of real estate, such as changes in real estate values and property taxes, interest rates, cash flow of underlying real estate assets, supply and demand, and the management skill and creditworthiness of the issuer. Investing in REITs may pose additional risks such as real estate industry risk, interest rate risk, risks related to the uncertainty of and compliance with certain tax regime rules, and liquidity risk.

The Schwab Center for Financial Research (SCFR) is a division of Charles Schwab & Co., Inc.

(1021-1FCM)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All