Soaring energy prices highlight the challenges of shifting toward renewable power sources. The continuing need for oil and gas during the transitional phase raises complex questions about balancing environmental needs and social concerns on the journey to a net-zero world.

The energy sector generates around three-quarters of greenhouse gas emissions today. It’s clear that renewable energy sources are the world’s only effective long-term solution to global warming. But meanwhile, the energy price spike (Display, below) is pressuring businesses and consumers.

If current trends continue, we believe similar price spikes will recur. And if policymakers and investors fail to plan the journey to a renewable world strategically, it will be hard to reach the ultimate destination of the Paris accords—net-zero carbon emissions by 2050 and limiting the rise in global temperatures to 1.5° C—to thwart a climate catastrophe.

Current and historical analyses do not guarantee future results. Through November 8, 2021 Data has been normalized to 2020. European Gas represented by TTFG1MON OECM Index (USD), Australia Export Coal represented by API31MON Index (USD), Brent Crude represented by CO1 Comdty (USD), US Gas represented by NG1 Comdty. Source: Bloomberg

What’s driving the current energy crunch? In a perfect storm, demand leapt as the world returned to work after COVID-19. But unusual weather patterns meant renewable power sources failed to perform as expected, while hydrocarbon supplies were hit by disruptions globally. Investor aversion to fossil fuels like oil and coal is only a subsidiary factor in today’s price crunch, which we expect will moderate next year as several temporary factors reverse. Still, with shareholders and other stakeholders pressing energy companies to limit oil and gas investment, today’s problems are likely a foretaste of more crunches to come.

Supply/Demand Picture Set to Worsen

To avoid them, the world must ensure a reasonable balance of supply and demand for energy during the transition. On the demand side, energy consumption normally increases in line with global population and GDP growth. By 2050, the world’s population may be two billion higher and the world economy twice as large (according to the United Nations Department of Economic and Social Affairs 2019 estimates). Against that background, achieving net zero carbon consumption by 2050 requires a huge increase in renewable energy generation, enormous advances in fuel economy and major behavioral changes from consumers. But although renewable power generation has increased dramatically from a low base, the absolute levels of new renewables capacity coming onstream are inadequate to cope with current demand growth projections. And consumers may increasingly push back on prices and proposals that will crimp their lifestyles.

Developed countries are leading the way in renewable energy production—but the world is spending only half of what’s needed on clean energy, according to the International Energy Agency (IEA). As for hydrocarbons, the IEA net zero pathway assumes that the world could achieve net zero by 2050 purely on existing reserves—so long as growth rates of clean energy sources are on track. That means, if renewables spending continues to fall short, the world will face a chronic energy gap.

Oil and Gas Exploration Is Fading

In part, that’s because environmental, social and governance (ESG) pressures are stifling investment in oil and gas.

Investment in oil, gas and coal has been subdued for several years (Display, below). Companies are under pressure to return cash to shareholders and invest in energy transition businesses rather than fossil fuels. What’s more, hydrocarbon energy investments have a long lead time and capex has been insufficient to maintain medium-term production, further complicating transition planning efforts.

Current and historical analyses do not guarantee future results. As of November 8, 2021 Source: Company reports and Danske Bank analysis

Effectively the world is living off major investment decisions in oil and gas that were made before the oil price fall in 2015. If nothing changes, hydrocarbons markets could tighten even more, triggering even higher-than-expected price hikes.

Investors have been deterred from the energy sector for two reasons. First, perceived ESG concerns may lead to further derating. In fact, deteriorating support for the sector has pushed oil stocks to extremely low valuations with a price/free cashflow ratio near 25-year lows (Display, below). Second, a collapse in demand for hydrocarbons may leave unused reserves “stranded” and effectively worthless.

In our view, stranded asset fears are misplaced. We think energy stock prices are predominantly valued on a discounted cash flow analysis based on existing projects; that means no value is placed on fields that aren’t yet producing or will produce soon. Most oil and gas companies have about a 10-year reserve life—a period in which fossil fuels will be critical for a smooth energy transition and short enough for investors in select oil and gas stocks to receive satisfactory returns. And if investor aversion continues to act as an additional brake on investment, energy prices will remain high, buoying cash returns to shareholders.

Balancing Environmental and Social Concerns

For ESG-focused investors, the backlash against big energy is understandable given the environmental damage of fossil fuels. However, because of the dynamics of the transition to renewables, we think there is a social dimension to consider as well.

A chronic energy deficit will hit poor countries and poor people hardest. For instance, if lack of power disrupts irrigation in poor countries, water and food will be in short supply. In developed countries, poorer people could be forced to choose between food and heating their homes in winter as prices spike.

Policymakers will find it challenging to maintain the consensus for energy transition if people suffer and businesses shut down because of higher energy costs. How long can they ride out a backlash from voters? As the IEA comments:

“The wholesale transformation of the energy sector cannot be achieved without the active and willing participation of citizens. It is ultimately people who drive demand for energy-related goods and services, and societal norms and personal choices will play a pivotal role in steering the energy system onto a sustainable path”

Wider Perspective Presents Practical Solutions

Faced with this complex picture, governments and investors need to take a more nuanced view of ESG issues to help enable a credible transition journey to net zero. If the journey is fraught with adverse near-term outcomes for society, it will be hard to reach the destination on time.

Currently, some major oil and gas companies are redeploying their hydrocarbon cash flows to invest in and develop renewable businesses, including associated infrastructure such as electric vehicle charging points on fuel station forecourts. And switching from dirtier hydrocarbons such as coal to cleaner ones like natural gas is also an important interim step on the journey.

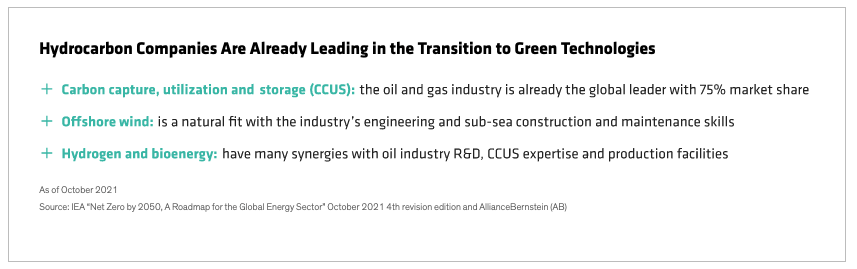

Consequently, we think that oil and gas companies with credible energy transition strategies are actually part of the solution and deserve closer attention from investors. Not only that, as these companies progress their corporate transformation plans, they will unlock value in next generation businesses in renewables and charging stations. The hydrocarbons industry has developed wide-ranging expertise in some of the critical areas for the energy transition. Logically, this makes select oil and gas stocks natural partners for governments and other stakeholders (Display, below).

As of October 2021 Source: IEA “Net Zero by 2050, A Roadmap for the Global Energy Sector” October 2021 4th revision edition and AllianceBernstein (AB)

Engagement Is Key to Successful Transition

The climate crisis inevitably sparks emotional reactions. But it will take cool heads and collaboration to tackle a problem of this magnitude. As President Biden remarked at the COP26 Meeting, “The idea we’re going to be able to move to renewable energy overnight was just not rational.” A complete transition to renewable energy will take decades, and in the meantime, fossil fuels will continue to play a critical and necessary role in, for instance, transportation, electricity and chemicals production.

Investor engagement will be key to expediting the transition. At AB, we routinely engage with our portfolio companies to understand how they are addressing climate change and to ask that they take actions in line with our best practice guidelines that will benefit both society and the sustainability of their cash flows. Such actions include, for example, reducing gas flaring, controlling emissions and strategic planning to secure their long-term future in a decarbonized world.

It’s also important for investors to engage with company management across the renewables sector. Clean energy solutions—including the shift to electric vehicles—may have their own ESG issues through the businesses in their supply chains. We need to ensure these are managed responsibly too.

Refraining from investing in or divesting from oil and gas companies comes at a cost. It removes access to company management and strips investors of the influence necessary to negotiate better outcomes both with the major greenhouse gas emitters and the other companies in the value chain.

Rethinking Oil and Gas Stocks

In the transition to renewable energy, we believe the energy price spike should serve as a wake-up call. ESG issues are rarely monolithic, and in the case of the global energy transition, we believe there are profound environmental and social complexities to be integrated into an investment analysis. Select oil and gas companies should be evaluated based on their role in responsibly supporting the world economy’s journey toward cleaner energy supplies. Their participation is essential for the transition pathway to be robust enough to have a realistic chance of success.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.