Schwab Sector Views is our three- to six-month outlook for stock sectors, which represent broad sectors of the economy. It is published on a monthly basis and is designed for investors looking for tactical ideas.

Rarely is there any sector that has everything going for or against it—and that is true today of the Information Technology sector. What’s to like? It boasts impressive profitability—the best across all 11 S&P sectors; it’s positioned well if economic growth continues—even at a slower pace; and it has compelling fundamental underpinnings, as inflating input and labor costs are spurring businesses to accelerate investment in productivity-enhancing technologies.

But there also things to dislike about the sector. It is highly concentrated in just a few stocks, valuations are sky-high by almost all measures, and higher interest rates—all things equal—could make them even less attractive. We’re neutral on the sector now.

What’s to like

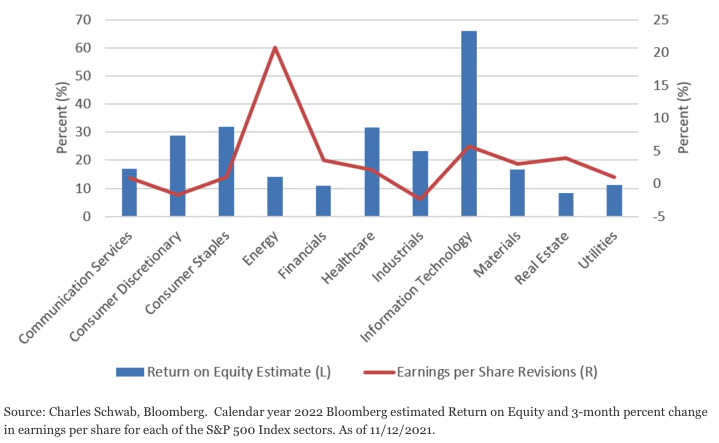

Strong profitability: One of the most important considerations for any sector is its fundamentals—the short- and long-term drivers for revenues and profits. A good yardstick of fundamental strength is return on equity (ROE), which measures how efficiently companies within a sector generate profits relative to shareholders’ equity. The Technology sector has the highest ROE of all sectors, as well as relative to its own historical average; and upward revisions to its expected earnings over the next year have been among the strongest of any sector.

The Technology sector has solid fundamentals

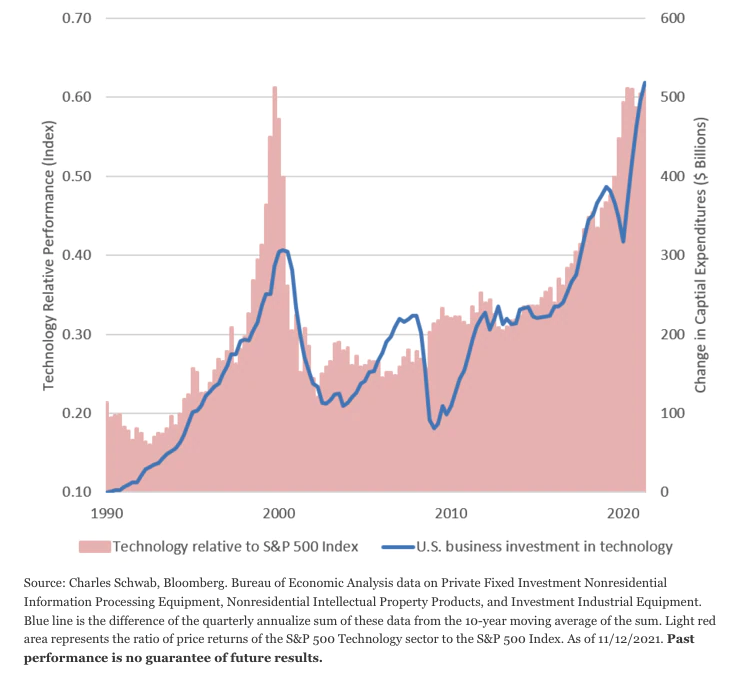

Rising capital expenditures: Even amid the offshoring of much technological innovation and production in the past several decades, business investment in information processing, software, and industrial equipment in the United States has increased significantly. The Technology sector continues to play a pivotal role in advances in robotics and automation; the transformation toward big data and cloud computing; the software and artificial intelligence that make it work; and smartphones, tablets, and network interfaces that enable us to use it. In the wake of the COVID-19 pandemic, higher wages, labor shortages and input inflation has resulted in an acceleration in investment in productivity—and labor-enhancing technologies. While there is some concern that the current surge in semiconductor production could result in oversupply when high demand is satiated, plans for more rapid spending on cost-saving technologies could help sustain demand for chips. We believe that strong trends in capital spending will continue and—if history is a guide—could coincide with outperformance of the Technology sector, as illustrated in the chart below.

Higher capital expenditures have led to better performance of the Technology sector

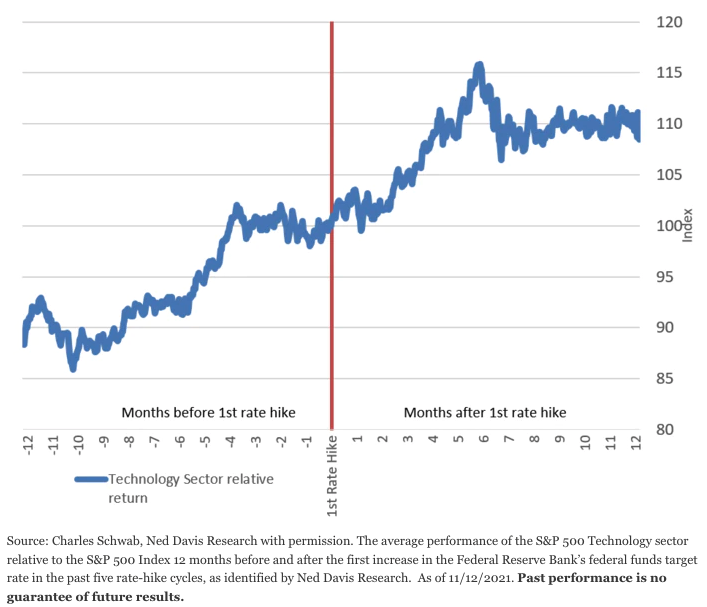

Cyclical growth characteristics: We think we’ve seen a peak in the rate of economic growth, though we expect it to continue at a slower pace—consistent with a maturing expansion phase of the economic cycle. Historically, the Technology sector has had its strongest outperformance on the tail end of recessions and into recoveries—as was the case in 2020 emerging from the COVID-19 recession. Growth stocks—many of which are in the Technology sector—also tend to perform well as economic expansions mature, as investors search for stocks with ongoing profit growth potential amid peaking earnings growth for the market overall. Additionally, the sector has historically outperformed the overall market on average in the 12 months prior to the Federal Reserve’s first hike in the federal funds rate.

The Technology sector has tended to outperform before a first rate hike

What’s to dislike

High valuations: Strong profitability and prospects for continued earnings growth, cyclical tailwinds, and trends in technology capital expenditures have been contributors to the outperformance of the sector in recent years. However, this has driven valuations by most measures well above their historical norms, except when they are considered in the context of the currently very low level of interest rates. A lower interest rate (a.k.a. discount rate) makes the value of future cash flows (i.e. earnings paid as dividends) worth more today. Taking that into account, the Technology sector appears to be fairly valued.

Here’s the rub. With inflation sharply higher and the Federal Reserve having embarked on the unwinding of its monetary stimulus, higher interest rates pose a significant though surmountable risk, in our opinion. We think that the 10-year Treasury yield could rise to 2% or higher in 2022, which may be a short-term headwind to the sector. Sectors with the highest valuation multiples—like Technology—could be the most at risk, particularly if the overall market reacts negatively to higher rates.

The sectors with high valuations are at risk from higher rates

Highly concentrated: While the Technology sector has 75 companies across six industries, just three stocks—Apple, Microsoft, and NVIDIA—account for nearly 50% of the sector’s market cap. As such, if you get the call on those stocks wrong, then you can get the whole sector wrong.

Putting it all together

We think that the fundamental and cyclical underpinnings of the Technology sector will prevail over the intermediate term. In our opinion, the strong trend in capital expenditures on productivity enhancing technologies will continue to support robust profitability, and the maturing phase of the business cyclical is favorable to the growth-oriented sector. Expectations for a rise in interest rates could be a short-term headwind for richly valued technology stocks.

However, if economic growth continues and inflation pressures eventually ease—as we think they will—a further rise in interest rates could reflect investor optimism in the economy, which is typically good for the Technology sector. We’re currently neutral on the sector as we assess the reaction to higher interest rates, but continued relative strength and seasonal tailwinds at the start of the year could tip the scales in favor of the sector.

What do the ratings mean?

The sectors we analyze are from the widely recognized Global Industry Classification Standard (GICS®) groupings. After a review of risks and opportunities, we give each stock sector one of the following ratings:

- Outperform: likely to perform better than the broader stock market*

- Underperform: likely to perform worse than the broader stock market*

- Neutral: no current view on likely relative performance

* As represented by the S&P 500 index

Important Disclosures:

Schwab Sector Views do not represent a personalized recommendation of a particular investment strategy to you. You should not buy or sell an investment without first considering whether it is appropriate for you and your portfolio. Additionally, you should review and consider any recent market news.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Diversification and asset allocation do not ensure a profit and do not protect against losses in declining markets.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

All corporate names are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

The Schwab Center for Financial Research (SCFR) is a division of Charles Schwab & Co., Inc.

(1121-1FH0)

© Charles Schwab

Read more commentaries by Charles Schwab