Equity investors focused on a low-carbon strategy needn’t compromise on company fundamentals. When quality and compelling valuations are equally considered, joining the global fight against climate change and generating strong return potential can work hand in glove.

At the UN’s recent COP26 climate summit, world leaders made ambitious pledges to combat global warming, but also appeared more concerned than ever of the hard work ahead. Delivering on their promises will be challenging, so it will take a collective effort to reach their goals. And equity investors can play a big role—lowering carbon emissions while meeting returns goals—with the right approach.

The Climate Task Is Monumental and the Stakes Are High

The COP26 gathering proved even more groundbreaking than the landmark 2015 summit, which spawned the watershed Paris Agreement. Among many resolute goals codified this year, the US outlined a record $555 billion in funding for clean energy projects as part of its Build Back Better infrastructure package. Additionally:

- G20 leaders agreed to halt funding of overseas coal power plants

- China and India, top greenhouse gas emitters, committed to net-zero emissions by 2060 and 2070, respectively

- South Korea will reduce greenhouse gas levels by 40% by 2030 and—with other countries—cut methane by 30%

- Canada will phase out coal-fired electricity by 2030

- Denmark will reduce emissions by 70% by 2030

- Italy has pledged to triple its climate protection budget commitment to $1.4 billion

While the shared goals were inspiring, the general mood was sober. The new and long-known science still points to the need to do more. And the next decade will be make or break. With little time to spare, countries, businesses and investors alike are being asked to do their part to directly or indirectly help lower emissions as 2030 approaches.

Nations and Governments Set the Tone, Companies Step Up

For equity investors, this means they don’t have to choose between a better environment or competitive returns, because it’s increasingly possible to have both.

While countries commit to goals, many quality companies are already reducing carbon-emissions. Forward-looking businesses have long seen higher value in a lower carbon footprint. And it’s starting to make a difference. For example, while global emissions rose 3.4% between 2015 and 2019, companies that applied science-based reduction targets cut their greenhouse gas emissions by 25%, according to CDP Worldwide, which helps businesses track their environmental impact. Actively engaging with companies on such measurable targets is a large step toward environmental improvement and a key consideration in the stock-selection process for an active low-carbon strategy.

Low-carbon investing covers a lot of ground and industries. Companies’ climate-resilience strategies, for instance, can shift strains and ensure continuity amid climate events. For example, Nestlé is putting resources and scale to work and tackling issues of climate change and biodiversity through their focus on regenerative agriculture. Many companies now reach out to help others lower their carbon emissions. Schneider Electric, a leading energy management firm, promotes and connects renewable energy sources among Walmart’s US-based suppliers.

Even companies with less obvious environmental credentials in the past have been taking low-carbon initiatives. Whether among the highest emitters, like Royal Dutch Shell, or lower-emitting businesses such as Microsoft, low-carbon strategies are improving bottom lines and fundamentally changing how companies do business up and down their supply chains.

Multiple Angles to Gauge Climate-Change Risk

There’s more to a climate strategy than owning low-emitting companies. Our research enables us to actively “decarbonize” a portfolio from the core out, starting with quality companies committed to long-term decarbonization goals. Companies without such plans may still seem to have high-quality businesses today, but eventually they’ll incur greater risks to their balance sheets and cash flows from the potentially burdensome cost of their carbon emissions down the road.

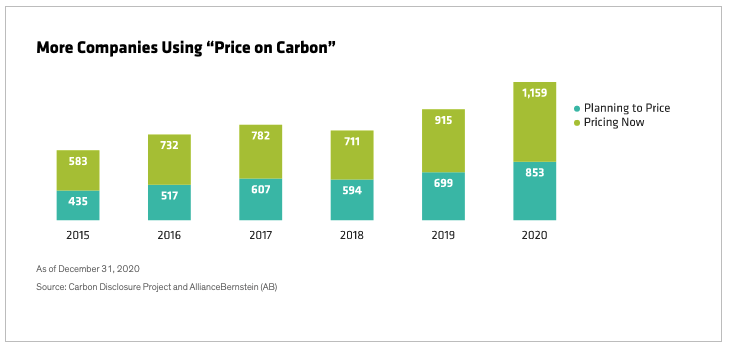

“Price on Carbon” Is a Game Changer

Practically every business model is linked to carbon emissions, whether as a producer or consumer of energy, or even indirectly via their supply chain.

With carbon emission levels widely varied across companies, factoring their cost implications up front offers an insightful apples-to-apples comparison across the investment universe. This “price on carbon” priority is a dynamic factor that can dramatically change a company’s forecast in an instant. The World Bank calls it one of the “strongest levers we have to shift financing toward climate action.” Price on carbon is a rapidly growing internal gauge as companies form strategies and a powerful tool for low-carbon investors to assess them more accurately (Display). As more companies incorporate a price on carbon when making decisions, investment analysts do too, so they can build more accurate forecasts to identify attractive opportunities.

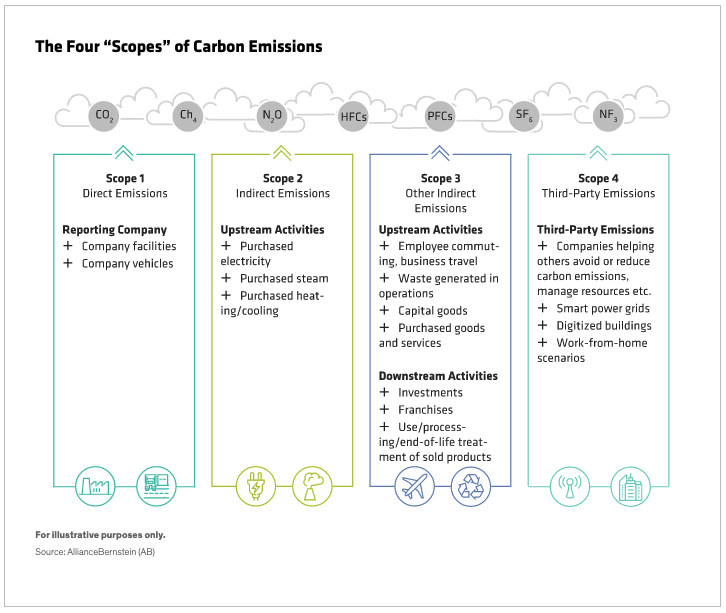

A price on carbon can also help catch tangential but related fundamentals that impact a company’s bottom line, like potential regulation (carbon taxes) and complying with standards (costly upgrades). These are typically found across four types of CO2 emission “scopes” that should all get equal scrutiny (Display).

Some are from current fossil fuel combustion and consumption or potential future releases from fuels not yet consumed; others are produced by third parties. But we believe investors should weigh them all to fully grasp their impact on a company’s value. From there, further research would drill down to other telling characteristics of quality and price.

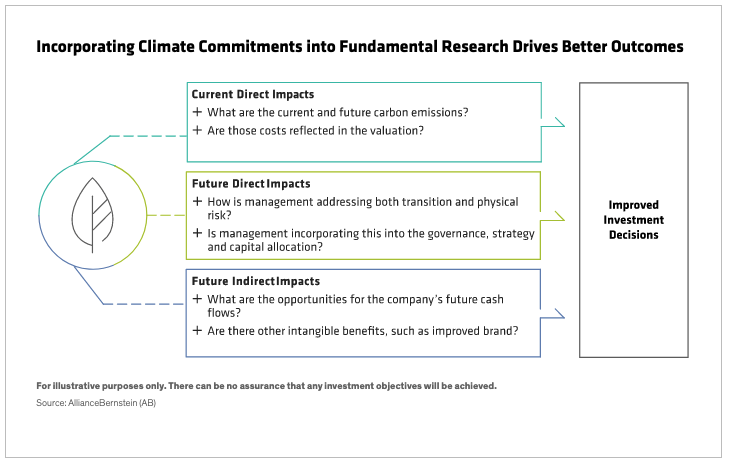

Assessing a company’s climate-risk exposure requires a broad, forward-looking approach based on scenario analysis. This means systematically thinking through how a wide range of potential scenarios could affect different types of companies. For example, changes in the physical environment or new policies and technologies could hasten the transition to a low-carbon economy. In our opinion, the investment opportunities that can withstand so many possible dangers are only discoverable by asking the right questions (Display).

Decarbonizing Helps Performance, if Quality Is There Too

Tendered pledges at COP26 may have earned some merit, but action gets results, and it’s needed now. Measurable targets like net-zero, 1.5 degrees Celsius and others will eventually help reverse the planet’s dangerous course. But they also create new ideas and inroads for company innovation and investment in the means and methods to transition to a low-carbon economy.

In our view, low-carbon investing can both help improve the environment and generate alpha over time. We believe the “E” in ESG isn’t a performance tradeoff but a strong support component in a strategic equity asset allocation. And, when comprised of an optimal mix of actively selected, high-quality companies with reasonable valuations, we believe a low-carbon portfolio can help investors achieve their goals of developing greener approaches to profitability and long-term returns.

Kent Hargis is Portfolio Manager—Global Low Carbon Strategy, Sammy Suzuki is Portfolio Manager—Global Low Carbon Strategy and Roy Maslen is Chief Investment Officer—Australian Equities at AllianceBernstein (AB)

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein