As one of the fastest-growing bond sectors, emerging-market (EM) corporate debt has become too big to ignore. With US$2.7 trillion outstanding across more than 600 companies, it’s now larger than the entire EM sovereign sector and is equal to the US-dollar and euro high-yield markets combined. For bond investors who’ve had a tough time finding opportunities for attractive yield and potential return, that’s good news.

Unfortunately, many investors hesitate to buy EM corporates because they’re holding onto outdated notions about these issuers—especially when it comes to environmental, social and governance (ESG) risks. In our view, investors need to cut through the confusion around ESG in EM to access a rising sector with a compelling risk/reward profile.

Below, we debunk the four most common ESG misconceptions about EM corporates—from wanton pollution to hopeless complexity.

Myth #1: EM companies are bad actors when it comes to the environment.

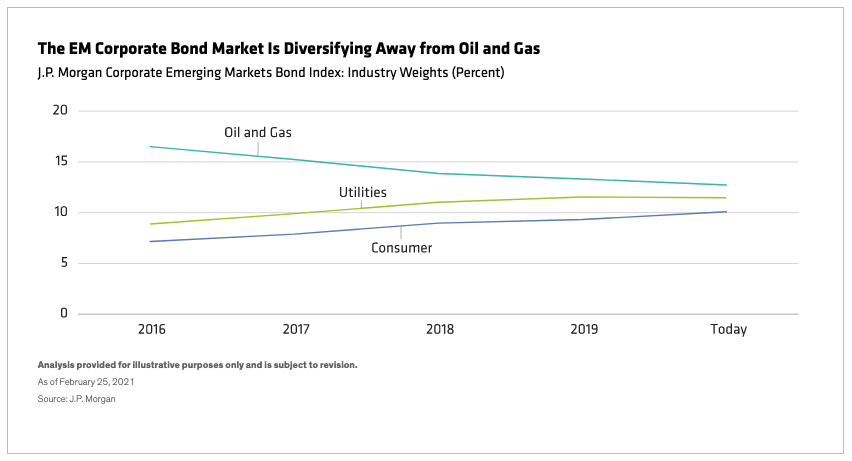

The first common misconception is that EM companies are all old-industry bad actors. It’s true that EM corporations were once heavy polluters, but that’s no longer the case. In just the last five years, the EM corporate bond universe has shifted away from traditional polluters such as oil and gas producers toward more ESG-friendly sectors. These include the utilities sector, where many companies are transitioning to renewable energy sources, and the consumer sector, including healthcare and some e-commerce enterprises (Display).

And certainly not all EM companies are ESG laggards; some are leading the global charge to slash emissions. Mexican chemical company Orbia Advance, for example, has some of the lowest emissions and most ambitious carbon-reduction plans in its industry—indeed, better than those of many major US and European chemical companies.

Further, emerging-market corporations lead the world in developing the resources needed to drive the transition to a cleaner-energy future. For example, they produce 80% of the world’s copper—demand for which is expected to rise 50% during the next 20 years—and more than half of all lithium, for which demand is expected to double by 2024, according to the International Copper Association. Both metals are used in batteries and other green technologies.

Lastly, the EM corporate universe has improved dramatically by sustainability measures thanks to the burgeoning issuance of ESG bond structures such as green and sustainability-linked bonds. Green bonds finance a green project within a given framework and timeline, while sustainability-liked bonds provide financial incentive for the issuing company to meet specific sustainability targets.

Putting it all together, emerging-market corporates are in fact part of the solution for a greener environment.

Myth #2: EM corporations have a terrible governance track record.

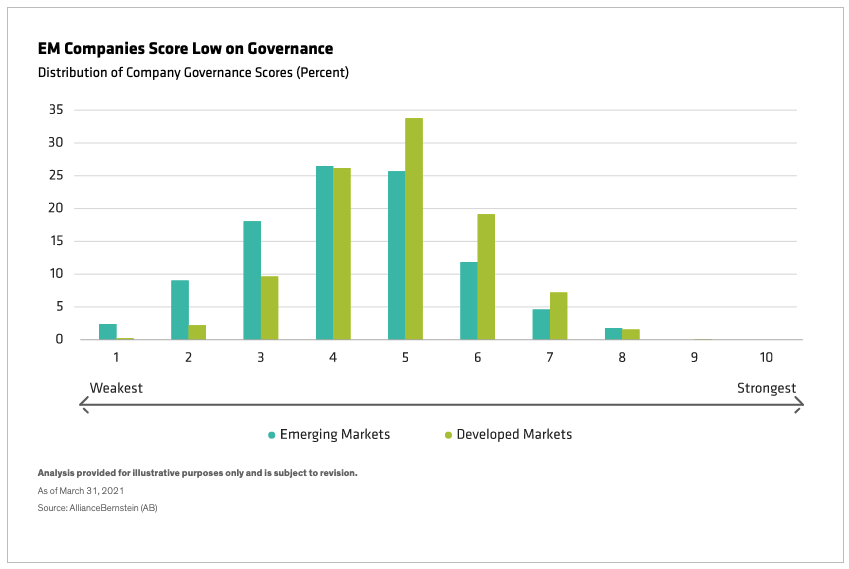

The second common misconception is that EM corporate governance meaningfully lags that of developed markets (DM). On the whole, EM corporates have just slightly lower governance levels than DM corporates—but there is wide dispersion in both groups (Display).

Sorting out good governance practices from bad ones is crucial to successful investing, because the stakes can be high. NMC Healthcare, a private healthcare provider based in the United Arab Emirates, illustrates how governance risk can adversely affect investors. The company understated its borrowings by US$4 billion over several years. When the extent of its poor governance came to light in 2019, it was placed in administration and bondholders suffered an 80% loss.

But the stakes can be high in a positive way too. For example, efforts by conscientious companies to improve their governance can pay off handsomely for investors. ContourGlobal, a UK-based power generation company with operations in Brazil, Bulgaria and Africa, enhanced its governance and environmental risk profiles by carrying out an initial public offering—making it subject to increased scrutiny and standards of transparency—and committing to build no new coal plants. These initiatives resulted in a significant decline in the company’s cost of funds, and investors in the company’s bonds during this period saw their holdings outperform.

Thus, governance issues shouldn’t weigh too negatively for EM corporations compared to their DM counterparts. But sorting out good from bad governance is indeed tricky, which brings us to our third myth.

Myth #3: Applying ESG to EM corporate bonds is too complicated.

Because ESG risks in this arena can seem impossibly opaque or complex, many investors don’t do the extensive due diligence required to differentiate within the EM corporate sector. However, it’s possible to identify and manage the ESG and other risks associated with EM corporates, given a sufficiently robust research methodology and investment process.

In particular, a 360-degree approach to collaboration across teams of economists, analysts, portfolio managers and specialists in responsible investing ensures the collection and assessment of relevant and timely information.

Such capabilities can identify opportunities as well as risks, making EM corporate bonds a rational and attractive proposition—not only for investors who are explicitly targeting responsible-investment outcomes but also for those who are primarily concerned with capturing competitive risk-adjusted returns.

Myth #4: ESG is too new and too niche to be effective with EM corporates.

ESG terminology may be new, but ESG risks aren’t—and they are real credit risks. Our research has shown that about two-thirds of the EM corporate bonds that underperformed over the past 10 years did so specifically because of ESG reasons, from catastrophic environmental events to accounting fraud. On the flip side, financing terms can be better for companies with strong ESG practices, which strengthens an issuer’s bottom line.

That means that, even if ESG isn’t top of mind for investors, they should incorporate ESG factors into the analysis, because it impacts every EM corporate issuers’ bottom line. And if ESG is top of mind, investing in emerging-market companies can help finance the world’s transition to greater social empowerment and environmental sustainability.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein