Treasury Inflation-Protected Securities: FAQs about TIPS

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsInflation continues to be a concern these days, and many investors are looking for investments that can keep pace with, or hopefully beat, the rate of inflation. As a result, Treasury Inflation-Protected Securities, or TIPS, have become a popular investment option.

But investing in TIPS isn't always straightforward. They have many unique characteristics that can make the investing experience a bit confusing. Here are answers to some of the most frequently asked questions about the TIPS market:

1. What are Treasury Inflation-Protected Securities?

Treasury Inflation-Protected Securities, or TIPS, are a type of U.S. Treasury security whose principal value is indexed to the rate of inflation. When inflation rises, the TIPS’ principal value is adjusted up. If there’s deflation, then the principal value is adjusted lower. Like traditional Treasuries, TIPS are backed by the full faith and credit of the U.S. government.

Although there are many measures of inflation, TIPS are referenced to one specific index: the Consumer Price Index, or CPI.

2. Will TIPS coupon payments fluctuate with the level of inflation, as well?

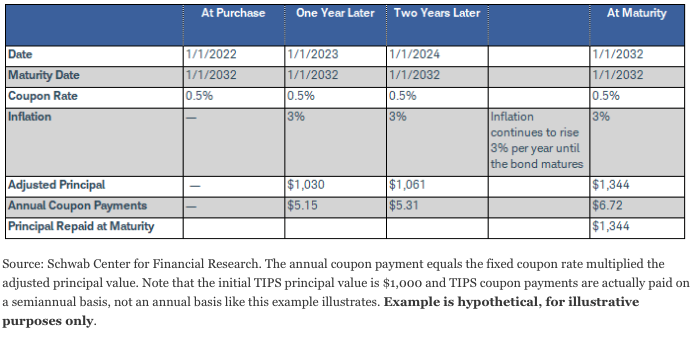

Yes. The coupon rate won’t change but the coupon payment will. TIPS have fixed coupon rates, which are based on the principal value of the security. If inflation rises, that rate is based off a higher principal amount. If inflation rises, so do the coupon payments. The table below provides a hypothetical look at a TIPS principal value and coupon payment based on a constant 3% rise in inflation.

How TIPS principal values and coupon payments can adjust to inflation

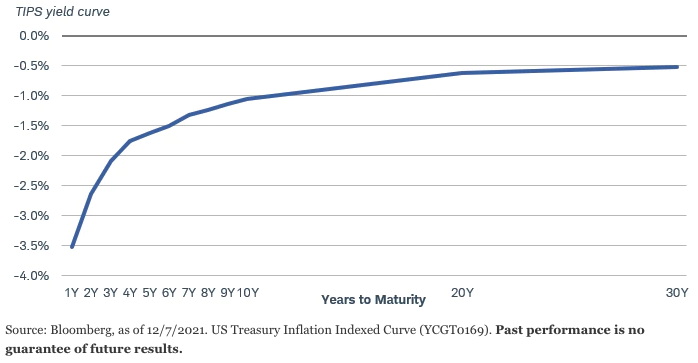

3. What sort of yields do TIPS offer today?

All TIPS yields are negative today.1 While that might surprise many investors, consider the yields of nominal (non-inflation-protected) Treasuries. The 10-year Treasury yield is still positive at around 1.5%, but after the rate of inflation is accounted for, that inflation-adjusted yield is also well below zero.

All TIPS yields are below zero today

4. TIPS yields are negative? Doesn’t that mean investors would lose money?

Not necessarily, because nominal returns can still be positive. A nominal return doesn’t account for the effects of inflation, while a “real” total return incorporates the effect of inflation.

By investing in an individual TIPS with a negative “real” yield and holding that TIPS to maturity, an investor would be locking in a loss relative to the rate of inflation. In this case, TIPS can help the investor keep pace with inflation, but not beat inflation.

Nominal total returns can still be positive, however. For example, assume a 10-year TIPS has a real yield of negative 1.0%. If inflation averaged over 1% per year, the nominal total return on this TIPS would still be positive, as the annual inflation adjustment would offset that annualized negative real yield. The higher inflation goes, the higher the nominal total return of a TIPS can go; the same can’t be said for the total return of a traditional Treasury.

5. How can I compare TIPS to traditional Treasuries?

Breakeven rates. A breakeven rate is the difference between the yield of a TIPS and the yield of a traditional Treasury of a comparable maturity. That difference is what inflation would need to average over the life of the TIPS for it to outperform the traditional Treasury.

For example, a five-year TIPS offers a yield of roughly negative 1.6% today, compared with a 1.2% yield for a traditional five-year Treasury. That difference is 2.8% (note that the TIPS yield is negative). If the CPI were to average more than 2.8% per year for the next five years, then that TIPS would provide a higher total return than the traditional Treasury. If inflation averaged less than 2.8%, then the traditional Treasury would outperform the TIPS.

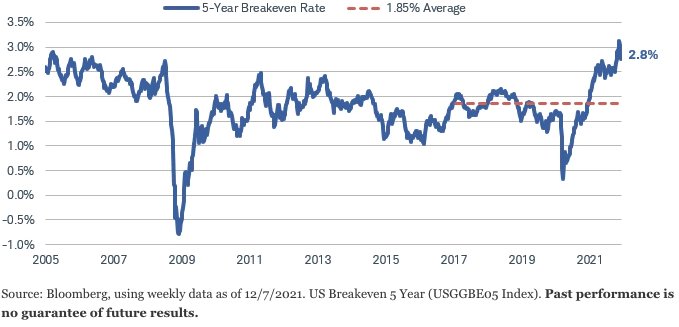

When evaluating TIPS, the breakeven rate matters just as much as your outlook for inflation. Breakevens have fallen from their recent highs but are still elevated compared to history—the average five-year breakeven rate since inception is 1.85%.

Five-year breakeven rates are off the all-time highs but still remain elevated

6. Would an investor beat inflation with TIPS?

It’s not likely to beat inflation with individual TIPS at today’s yields that are held to maturity. For investors who purchase individual TIPS, the negative yields mean that they are essentially locking in that negative yield regardless of how high (or low) inflation goes. Even if inflation surges, the TIPS principal value is simply rising by the same rate as inflation, but not enough to offset the premium the investor paid (that premium that resulted in a negative yield.)

It also depends on the time horizon. With negative yields, it’s still possible for returns to beat inflation over the short run. Whether one holds individual TIPS or invests using a mutual fund or exchange-traded fund (ETF), total returns over short investing horizons can beat inflation. Although past performance is no guarantee of future results, note that in the 12 months ending November 30, 2021, the Bloomberg U.S. TIPS Index delivered a total return of 6.8%, even though the starting yield was negative.

7. If inflation rises sharply, will TIPS perform well over the short term?

It depends. In addition to the inflation adjustments, TIPS performance over the short run is also driven by price appreciation or depreciation depending on any change in the TIPS’ yields.

If yields rise enough where a TIPS’s price declines enough to offset the inflation adjustment, total returns can be negative. Likewise, if yields fall further and prices rise in the short-run, total returns may be strong given both price appreciation and the inflation adjustment.

With yields so low, however, we do see a risk in yields moving modestly higher into 2022, which may limit the total return potential for TIPS investments.

For that reason, we stop short of calling TIPS a good inflation “hedge,” especially over the short run. Over the long run, however, TIPS are one of the most straightforward ways to protect against inflation.

8. What’s the best way to invest in TIPS?

You can invest in TIPS either by holding individual bonds, or through a mutual fund or ETF. There are pros and cons to each approach. By holding individual bonds, you can plan to hold to maturity, meaning any short-term price fluctuations might not matter. Individual TIPS also can be good planning tools. While the amount at maturity isn’t totally known in advance, given the principal adjustments, investors can expect a return of at least the original $1,000 principal plus or minus the principal adjustment.

With a mutual fund or ETF you can get more diversification than might be achieved by buying individual TIPS yourself, and usually at a low cost depending on the fund. You also get the benefit of professional management, and potentially better pricing on the bonds than you might get by investing in individual bonds yourself. Mutual funds and ETFs don’t usually have a maturity date, so their prices or net asset values (NAV) will fluctuate, and there’s no certainty about what that price or NAV will be at a point in the future.

9. When I look at various mutual funds or ETFs that hold TIPS, why are the stated yields so different?

TIPS mutual fund or ETF yields may appear distorted due to short-term fluctuations in the CPI, and they might not be reflective of the market yield of the underlying securities.

While individual TIPS yields are currently all negative2, the quoted yields of many TIPS funds are positive because they include inflation compensation. The discrepancy stems from how some of the yields are calculated, since calculations may differ across fund sponsors. The SEC 30-day yield looks at dividends and interest paid over only one month and annualizes it, showing what the yield would be if it persisted for 12 months. While it’s a standardized yield, it can overstate the actual yield if a very high monthly CPI reading results in a higher-than-expected monthly distribution. Likewise, a very low or negative yield could be attributable to the fall in inflation rate and might not be repeated.

Meanwhile, the distribution yield, or “trailing 12-month” yield is backward-looking, reflecting payments made over the last 12 months, and therefore might not be a strong indicator of what to expect in the future. As is the case with differing yield calculation conventions across fund sponsors, distribution schedules also differ across funds and fund sponsors. So at any point in time, distribution yield comparisons may reflect these differences

When considering TIPS mutual funds or ETFs, check for any other discrepancies with the stated yields. If a fund’s yield is dramatically different from the yield of the underlying holdings, try to figure out what’s causing the difference, so your expectations will be more accurate. If a distribution in a single month has distorted a bond fund’s yield, don’t let that distort your expectations going forward.

10. Why have the monthly income payments from my TIPS funds declined when inflation is still so high?

Every TIPS mutual fund or ETF is different, but there may be a lag from when a given month’s CPI is released and when it is considered for the distribution. For example, the CPI reading for the month of January won’t be released until mid-February, but then that inflation adjustment might not be reflected in the fund distribution until a month or two later.

“High inflation” is a relative term, of course. A given month’s change in CPI might be high by historical standards, but if it’s less than the previous month’s change, then the monthly distribution could decline.

Keep in mind that these are just high-level guidelines—there are a number of factors that go into a fund’s distribution, not just the level of inflation. Each mutual fund or ETF may also have its own guidelines for how it calculates its monthly distributions.

What to do now

TIPS are worth considering today, especially for those investors worried about inflation. Keep in mind that breakeven rates are very high today, so the cost of inflation protection is expensive. If actual inflation doesn’t meet the lofty expectations, TIPS could underperform traditional Treasuries.

Despite their current negative yields, TIPS are still one of the most straightforward ways to protect against inflation over the long run. For investors who currently have an allocation to high-quality, highly rated bond investments like Treasuries (but no exposure to TIPS), it makes sense to consider shifting some of that exposure to TIPS to help protect against long-term or unexpected surges in inflation. Just remember that they are still subject to the inverse relationship between their prices and yields like traditional Treasuries, and that they could underperform traditional Treasuries if inflation comes back down to more normal levels.

1 Source: Bloomberg, as of 12/7/2021. US Treasury Inflation Indexed Curve (YCGT0169).

2 Ibid.

Important Disclosures:

Investors should consider carefully information contained in the prospectus or, if available, the summary prospectus, including investment objectives, risks, charges, and expenses. Please read it carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the U.S. government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the U.S. government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

The Consumer Price Index (CPI) is an index that measures the weighted average of prices of a basket of consumer goods and services, weighted according to their importance.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(1221-142S)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All