Most investors need little persuading that emerging markets offer exciting opportunities. The emerging-market (EM) corporate bond market in particular presents a tantalizing prospect for investors: Its size and strong historical performance make it impossible to ignore.

But emerging markets also pose significant and complex challenges. Some challenges—such as inconsistent regulations and a lack of standardization across countries—reflect the diverse nature of emerging markets. But others, such as the seemingly intractable problems of pollution and corruption—are ESG risks.

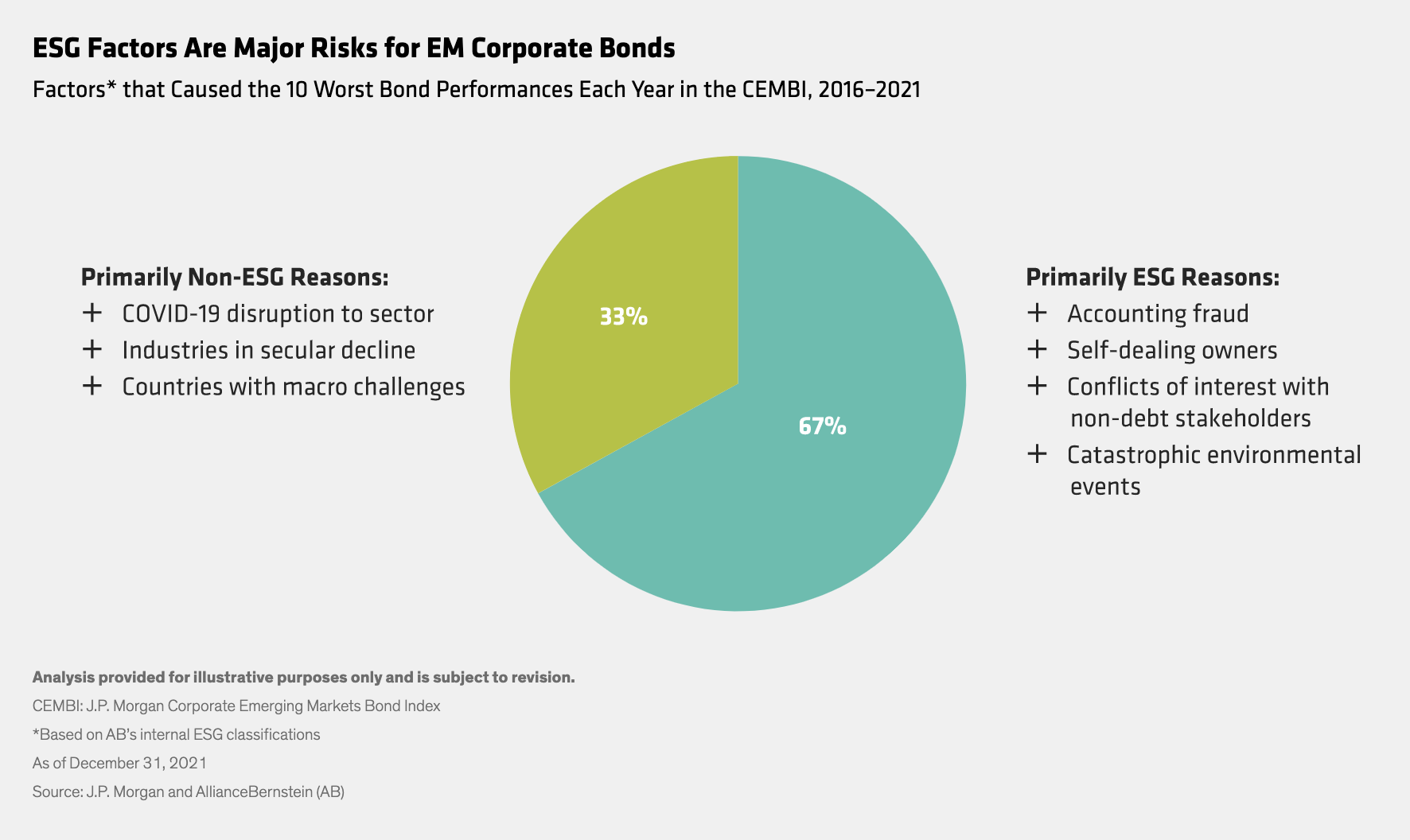

These risks can be material. Our analysis shows that, from 2016 through 2021, two-thirds of the worst-performing credits in the J.P. Morgan Corporate Emerging Markets Bond Index (CEMBI) were those with weak ESG practices.

Take NMC Healthcare, a private healthcare provider based in the United Arab Emirates. NMC Healthcare illustrates how governance risk can adversely affect investors. The company understated its borrowings by US$4 billion over several years. When the extent of its poor governance came to light in 2019, it was placed in administration and bondholders suffered an 80% loss. Similarly, Chilean coal-fired power company Guacolda Energia saw its bond price—and bond ratings—plunge when it resisted diversifying away from coal toward renewable resources, which led to difficulty securing long-term contracts. Investors who can thoroughly assess a company’s ESG risks can get ahead of such bad news.

At the same time, efforts by conscientious companies to improve their ESG practices can pay off handsomely for investors. ContourGlobal, a UK-based power generation company with operations in Brazil, Bulgaria and Africa, enhanced its governance and environmental risk profiles by carrying out an initial public offering—making it subject to increased scrutiny and standards of transparency—and committing to not build new coal plants. These initiatives resulted in a significant decline in the company’s cost of funds, and investors in the company’s bonds saw their holdings outperform.

Of course, ESG risks to investing in EM debt should be kept in perspective. For example, emerging countries’ per capita carbon emissions are much lower than those of developed countries. And not all EM companies are ESG laggards; some are leading the charge to slash emissions. Mexican chemical company Orbia Advance, for example, has some of the lowest emissions and most ambitious carbon-reduction plans in the industry—indeed, better than those of many leading US and European chemical companies.

The bottom line? ESG isn’t an alternative approach to traditional sovereign or corporate-credit analysis. It’s the foundation on which long-run economic performance is built. That’s why the key to unlocking opportunity in emerging markets lies in fully integrating ESG factors into bottom-up research and the investment process. We think that bond investors—whether or not they are driven by explicit responsible-investment objectives—are likely to see the merit of such a win-win proposition.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein