The COVID-19 pandemic looked set to batter the world’s banks—and yet banks’ balance sheets are now the strongest they’ve been since the global financial crisis (GFC). That surprising outcome is particularly good news for investors in subordinated bank debt.

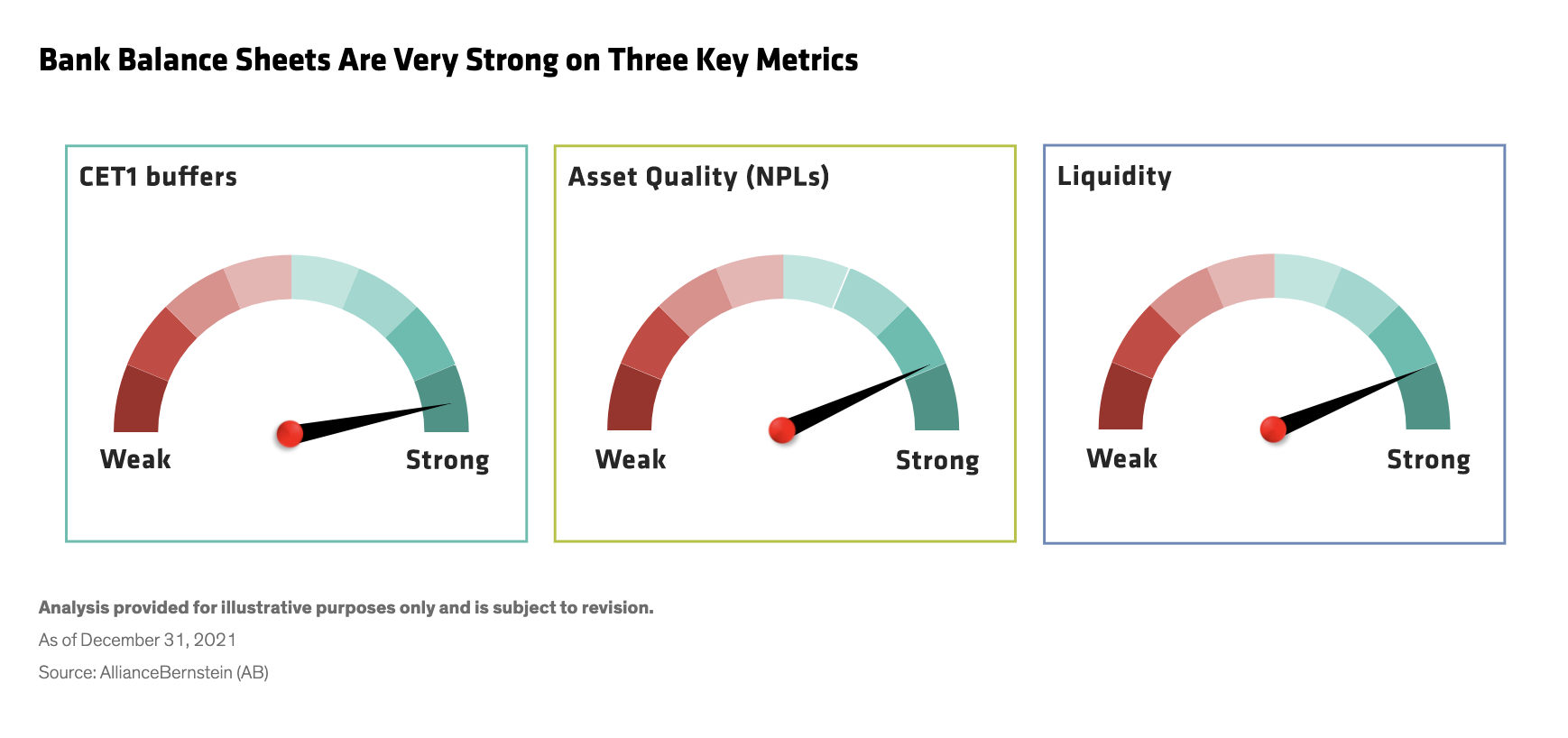

Post GFC, regulators globally forced a reboot of bank balance sheets through stricter solvency requirements. Now, almost 15 years later, bank fundamentals have risen to peak levels (Display).

Analysis provided for illustrative purposes only and is subject to revision.

As of December 31, 2021

Source: AllianceBernstein (AB)

Common Equity Tier 1 capital buffers are close to all-time highs. Asset quality (measured by the percentage of nonperforming loans) is very robust. And balance sheet liquidity is exceptionally strong, boosted by a combination of unprecedented access to central bank funds (particularly in Europe), huge customer deposit inflows and muted loan growth.

Bank credit ratings have returned to pre–COVID-19 levels and there is potential for further upward rerating as agencies recalibrate their rating methodologies. Looking forward, we expect the banks will return some capital to shareholders, reducing balance sheet strength. Even so, we still think bank capital will remain buoyant—and highly supportive for bondholders.

Government Intervention Has Helped Enormously

The banks mostly entered the crisis in a financially strong position. The intervention of governments and their central banks has also been crucial. Massive support programs and stimulus packages have in many cases averted the worst-case outcomes from the impact of COVID-19 for businesses and individuals. That in turn has reduced the pressure on banks across the developed world.

On that basis, the large loan-loss provisions for COVID-19–related damage that the banks made in 2020 now look overly prudent, and some have already been written back. The banks appear to have fully provided for a potential increase in loan losses in 2022 and 2023. And if anything, they should have scope to reverse more of their provisions in the second half of this year as previous economic assumptions continue to be revised upward.

Bondholders Are Beneficiaries—but Face Some Threats Too

Although equity profitability remains muted—constrained by low rates, competition, the costs of digital capex and (in the short term) loan-loss provisions—the shift to a rising-rate environment should help boost banks’ profits. But for banks’ bondholders, profitability is not so important, except insofar as it affects banks’ ability to raise fresh equity capital. Their main concern is the strength of the equity buffers that protect them from capital losses. And the current very healthy state of bank balance sheets benefits the riskiest bonds—subordinated credits including contingent convertible bonds such as Additional Tier 1 (AT1) securities—the most.

Banks’ bondholders enjoy some further advantages in a post-COVID world. For instance, legacy issues such as GFC-era lawsuits are mostly resolved. More credible regulatory stress-testing (now including climate risks) gives more comfort than pre-GFC, and greater regulatory support for mergers and acquisitions (especially in Europe) should make for stronger banks and better-protected bondholders.

Also, bank business models are becoming better diversified, with a greater focus on fee-generating activities. And the worldwide transition to greener business models should create more opportunities for profitable lending.

But banks’ bondholders face some new threats too. Banks will now be looking to return what they deem to be excess capital to shareholders in the form of dividends and buybacks, with US banks likely the most aggressive. But although we expect CET1 buffers to weaken a little, we think regulators will stop the banks eroding them too close to the minimum requirements.

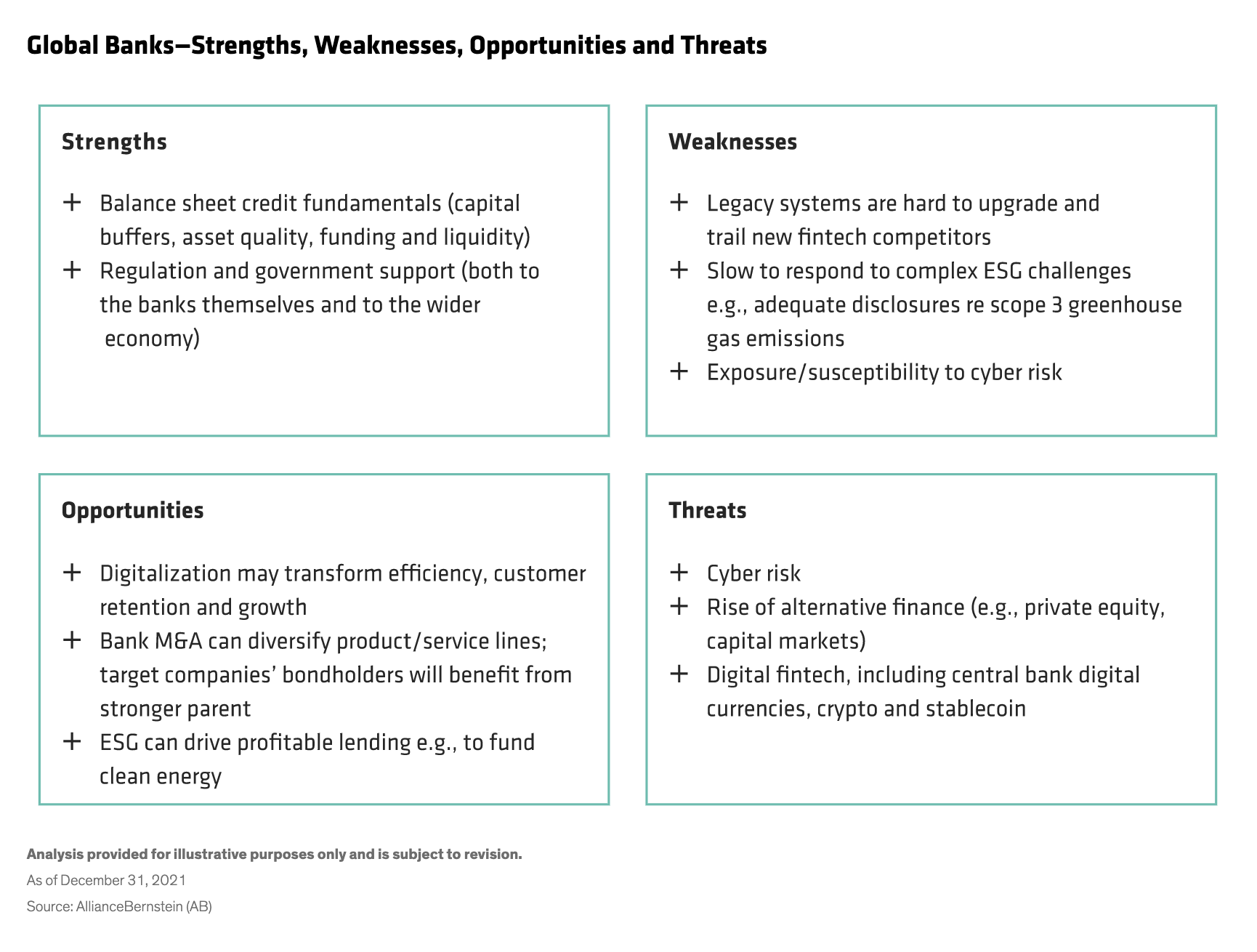

That said, the next crisis could prove harder to weather: governments have extended extraordinary levels of support during the pandemic but are unlikely to be able to respond to emergencies so generously in future. Also, technological advances can drive profits but may also fuel new competitors. The banks have done well to fend off challengers so far, but disruptive new entrants are still a risk. Lastly, the possibility of a major cyber incident remains a serious and unquantifiable threat (Display).

Analysis provided for illustrative purposes only and is subject to revision.

As of December 31, 2021

Source: AllianceBernstein (AB)

For now, however, the main risks remain mostly medium to longer term, and so are less likely to trouble bondholders. That’s not to say 2022 will be all plain sailing. We expect a more volatile year ahead, with potentially lower total returns for bondholders than in 2021. Even so, the high income from subordinated bank debt in particular still looks very attractive.

Subordinated Bank Debt Represents Compelling Relative Value

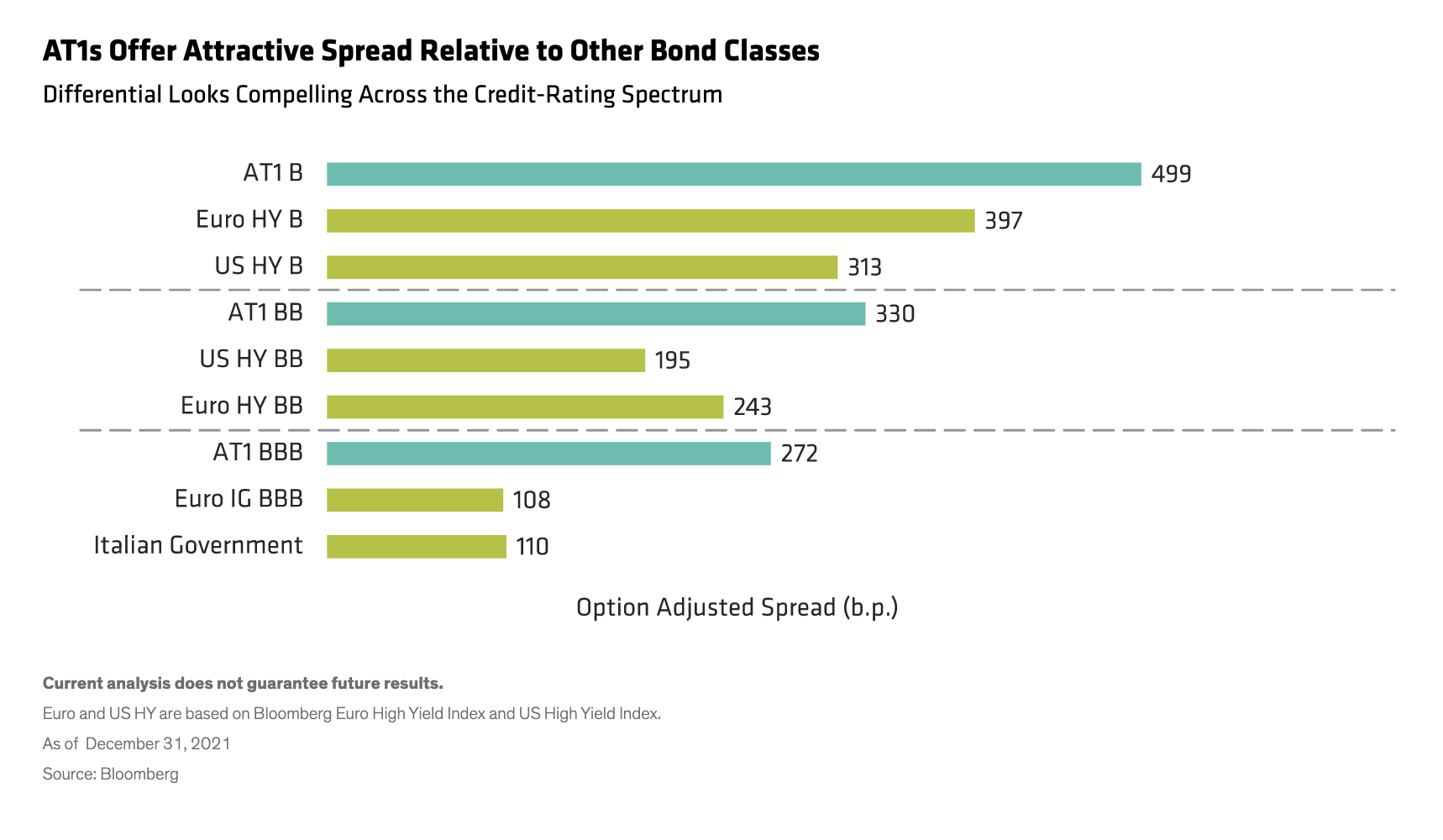

Current valuations of banks’ senior preferred and non-preferred debt already reflect much of the good news. Moreover, we expect an uptick in issuance of European senior preferred bonds later this year because of upcoming changes to the terms of the European Central Bank’s lending subsidy scheme (TLTRO). But net supply for subordinated financial bonds will likely be at or close to zero, and they remain attractively priced, in our view. Specifically, AT1s look compelling versus comparable high-yield credits (Display). We think AT1s issued by the stronger European banks offer the best trade-off between maximizing return and mitigating risk.

Current analysis does not guarantee future results.

Euro and US HY are based on Bloomberg Euro High Yield Index and US High Yield Index.

As of December 31, 2021

Source: Bloomberg

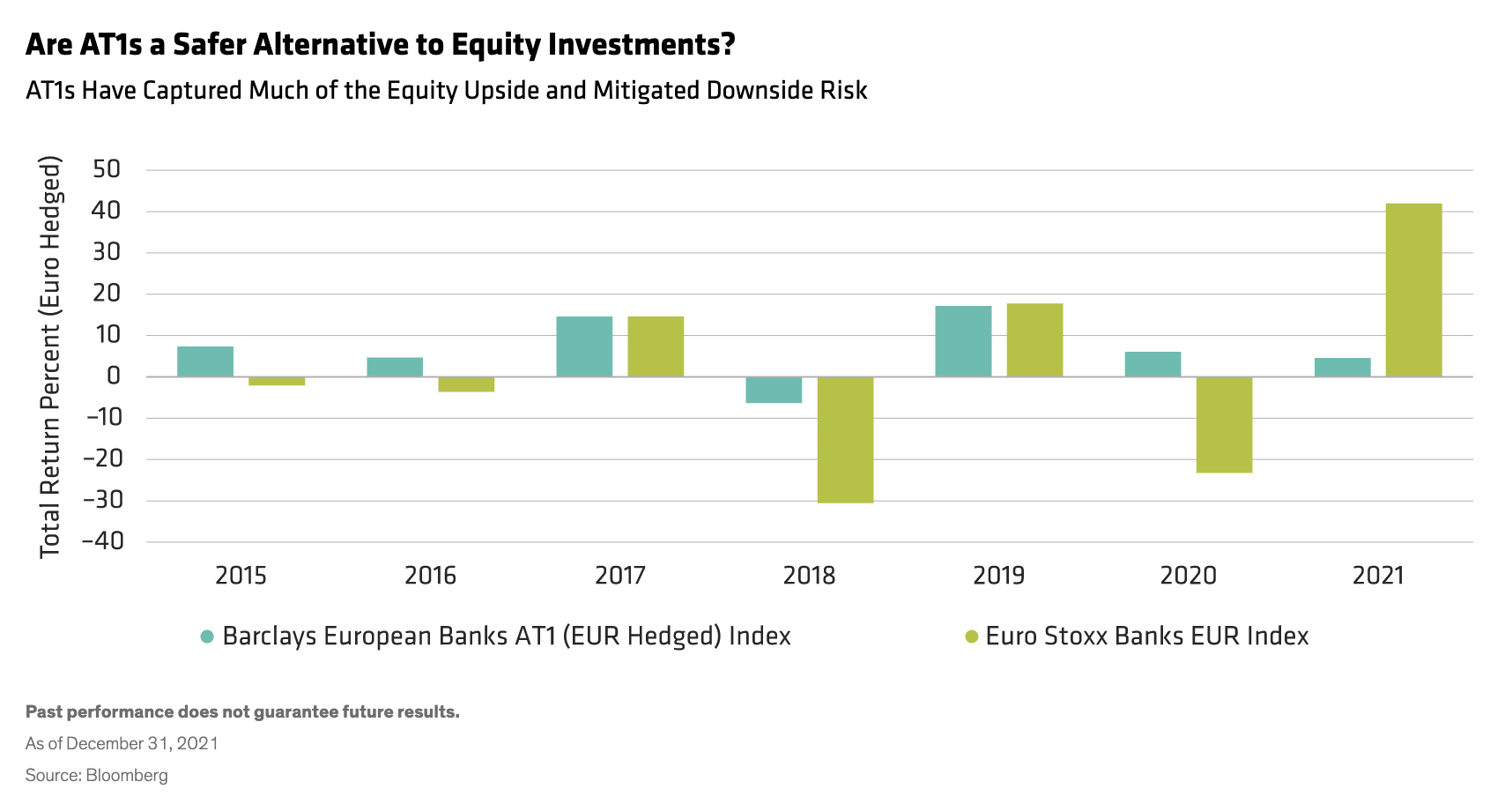

Not only do AT1s represent better value at each point on the credit-rating spectrum, but their realized risks versus bank equity have been lower too (Display). And while the high-yield default rate over the last five years has been 3%–4% annually, not a single AT1 has converted to equity and only a handful have extended their repayments.

Past performance does not guarantee future results.

As of December 31, 2021

Source: Bloomberg

Of course, those statistics will change over time. But while banks’ balance sheets remain so strong, we see the balance of risk continuing to favor subordinated financial credits.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein