Markets appear to be reacting to military developments in Ukraine. Russia’s stock market usually trades in sync with oil prices. But recently, as oil hits new highs, Russian stocks have fallen into a bear market, likely tied to the rising risk of a Russian incursion into Ukraine.

Stocks and oil prices

Russia’s buildup of military forces around Ukraine is larger in scope than the exercises of March 2021 and echoes the Russian invasions in Georgia in 2008 and Ukraine in 2014. As in 2014, both the U.S. and NATO have communicated that they are not considering the deployment of their forces to Ukraine to repel a Russian invasion.

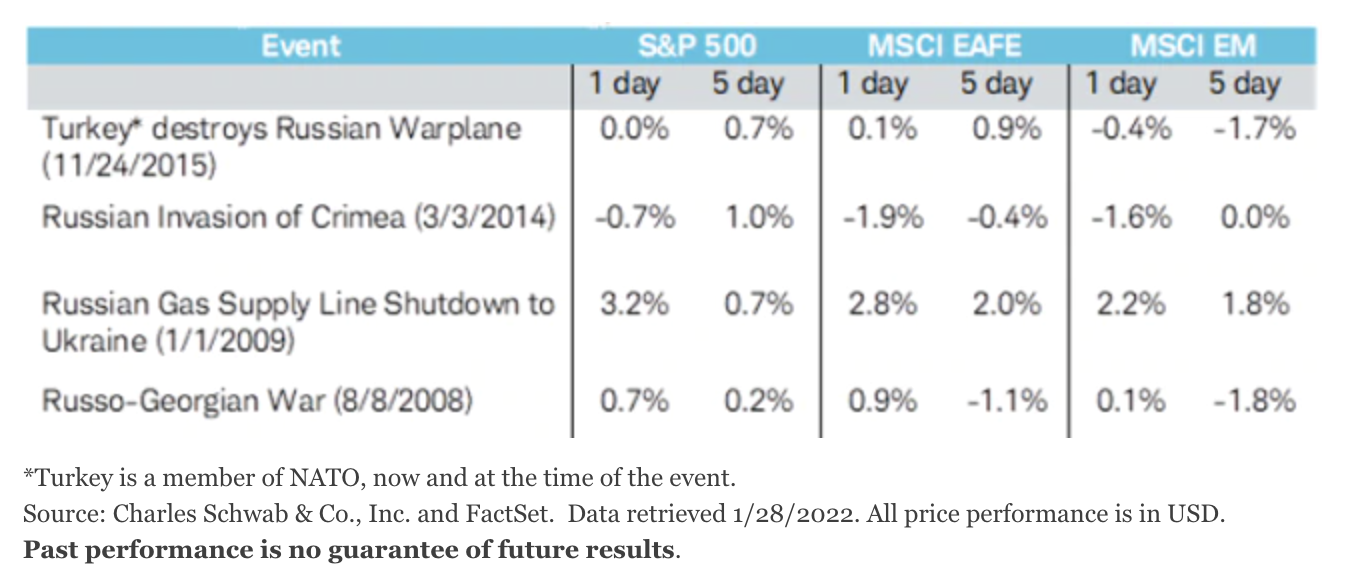

The human costs of military action are unmeasurable. Yet, the stock market reaction to an incursion or invasion of Ukraine may echo those of the past with little measurable impact for diversified investors. Previous incidents involving Russia had little impact to the markets. Most similarly, Russia’s invasion and subsequent annexation of Crimea from Ukraine in 2014 saw the S&P 500 and other developed and emerging markets around the world dip less than 2% on the day it occurred and rebound at least partially during the following five days.

Historical Geopolitical Events involving Russia

Russia has very small equity exposure in the global indexes, making up only 3.2% of the MSCI Emerging Markets Index and just 0.4% of the global stock market measured by the MSCI AC World Index. Ukraine has no exposure in either index.

Sanctions

Any sustained market impact could be influenced by economic sanctions imposed on Russia.

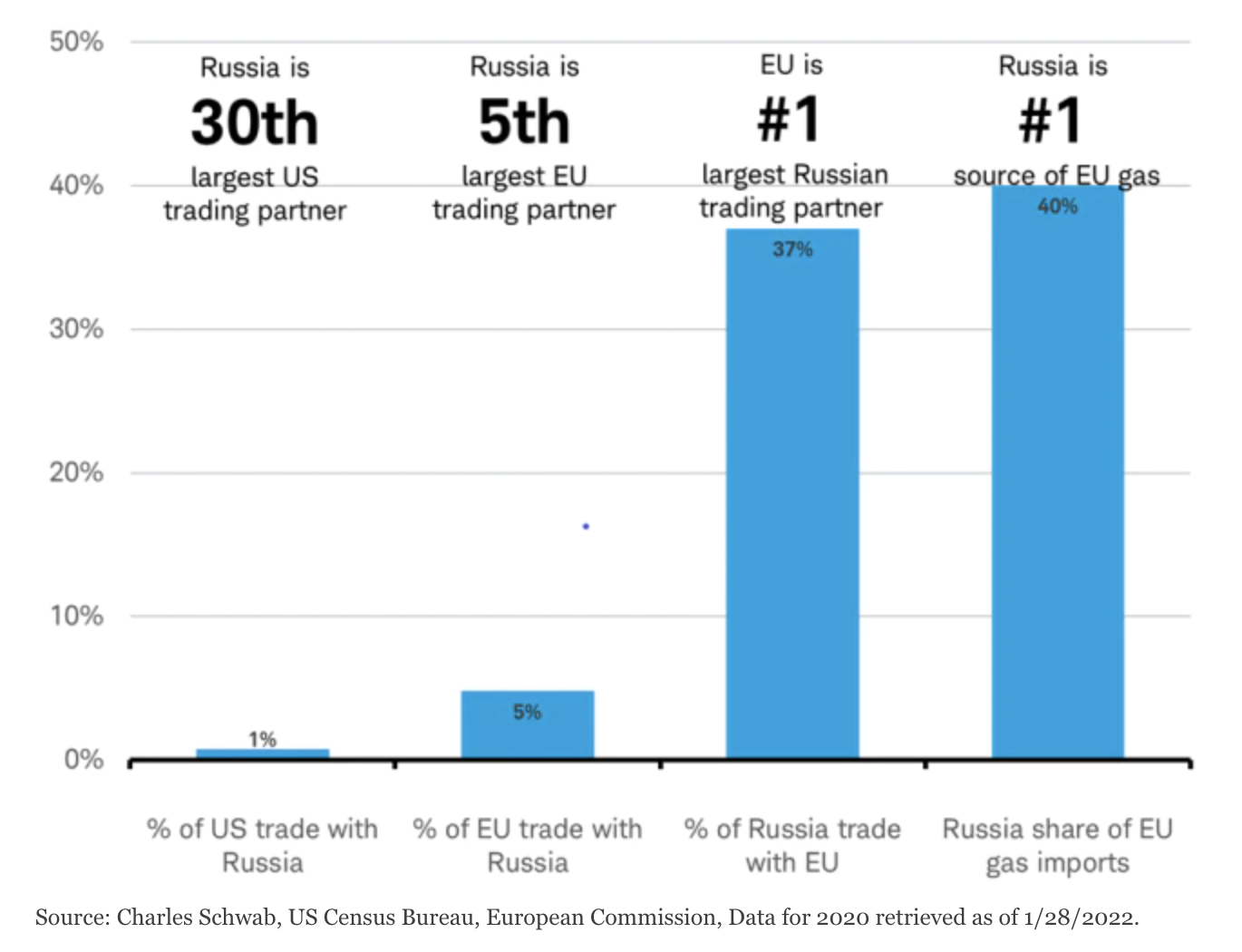

The United States has discussed with its allies measures that include cutting off Russia’s largest financial institutions from global transactions to hurt Russia’s businesses and imposing an embargo on American-made technology to exert pressure on Russia’s military and its consumers. But there isn’t unanimous support for these measures among U.S. allies. Russia is the U.S.’s 30th largest trading partner—that is pretty far down the list. But that isn’t true for Europe. Russia is Europe’s 5th largest trading partner—and accounts for 40% of the Europe’s gas imports.

Trade relationships

European officials worry that the proposed U.S. sanctions might prompt Russia to retaliate by cutting off natural gas and oil flows to Europe, something Russia has done previously to exert its influence. Europe is very dependent upon Russia for its energy supplies and has not been able to build up its reserves for the winter heating and energy demands. While both the U.S. and Qatar have already stepped-up production to meet increasing shortages, supplies remain tight.

Instead of U.S.-led sanctions, a key lever for sanctions in Europe may be Germany’s willingness to halt the certification of the Nord Stream 2 pipeline should there be an invasion of Ukraine. The Nord Stream 2 bypasses Ukraine in its delivery of natural gas from Russia to Europe, depriving the country of the approximately $2 billion in annual transit fees Russia currently pays to use the first Nord Stream pipeline. These tariffs contribute to the Russia-Ukraine hostilities. The Nord Stream 2 pipeline construction was finished in September, but German regulators have yet to issue the final legal permission Russia needs to begin operations. Germany’s new Chancellor, Olaf Scholtz, has said he may not approve it if Russia invades Ukraine.

Impact of sanctions

Russia has taken steps in recent years, such as building up foreign currency and gold reserves (Source: Central Bank of the Russian Federation) and bolstering relationships with China, to minimize the impact of financial and trade sanctions on its economy after being subjected to them for almost a decade.

- The 2014 sanctions imposed by the Obama administration on Russia, after its invasion of Crimea, remain in effect.

- Additional sanctions imposed by the Trump administration after Russian meddling in the 2016 U.S. election remain in place.

- Further sanctions were applied by the Biden administration in 2021 after the SolarWinds cyberattack, which exposed data from both the U.S. government as well as hundreds of American companies.

Any further sanctions imposed are unlikely to have meaningful economic impact on the U.S., due to limited economic exposure. There has been little impact on the U.S. economy from the sanctions listed above. U.S. exports to Russia are primarily agricultural and are unlikely to have any measurable impact on the U.S. market indexes.

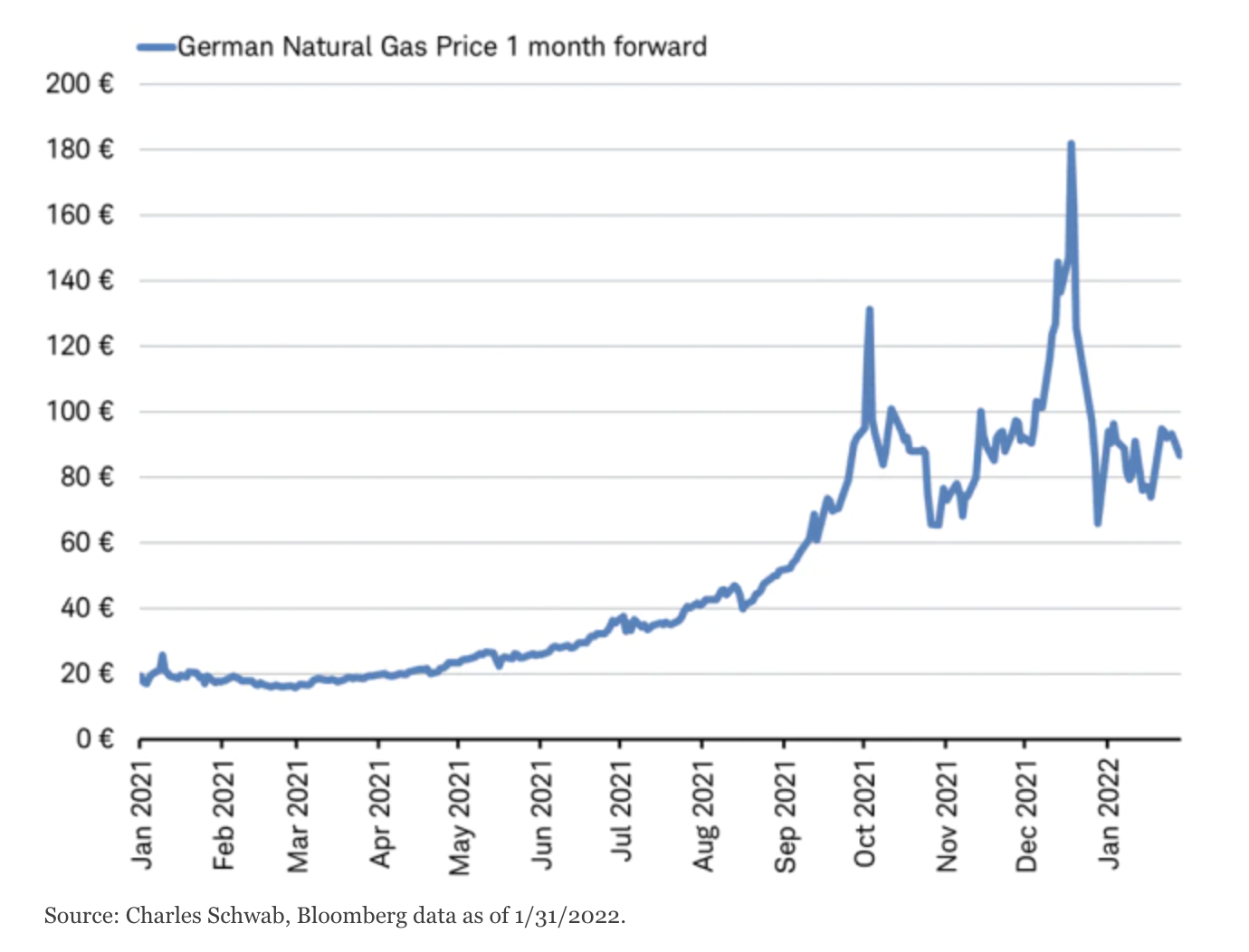

In Europe, the main economic impact is likely through energy prices. However, a lot of the impact to energy prices may be already priced in from politically motivated Russian supply cuts last year. Oil and gas prices have soared in Europe over the past year and are contributing to inflation and weighing on growth. To counteract this, the government in France, and others in Europe, have put freezes on consumer energy prices to try to lessen the impact.

Natural gas prices in Europe

European growth is set for a strong pace in 2022 at 3.9% according to the International Monetary Fund, despite the risks that include high energy prices. This should lend support to European stocks, especially with price-to-earnings multiple for the MSCI Europe Index which is in line with the 20 year average, in contrast to the still historically high valuations for U.S. stocks represented by the S&P 500. So far this year, European stocks have outperformed the U.S. market. A risk to continued outperformance is that the higher natural gas prices climb, the more utilities in Europe may struggle to quickly pass on those costs to consumers.

China-Taiwan

On the surface, there seem to be similarities between Russia invading Ukraine and China’s threats to invade Taiwan. But, they are fundamentally different, and we should not assume anything about one from the other.

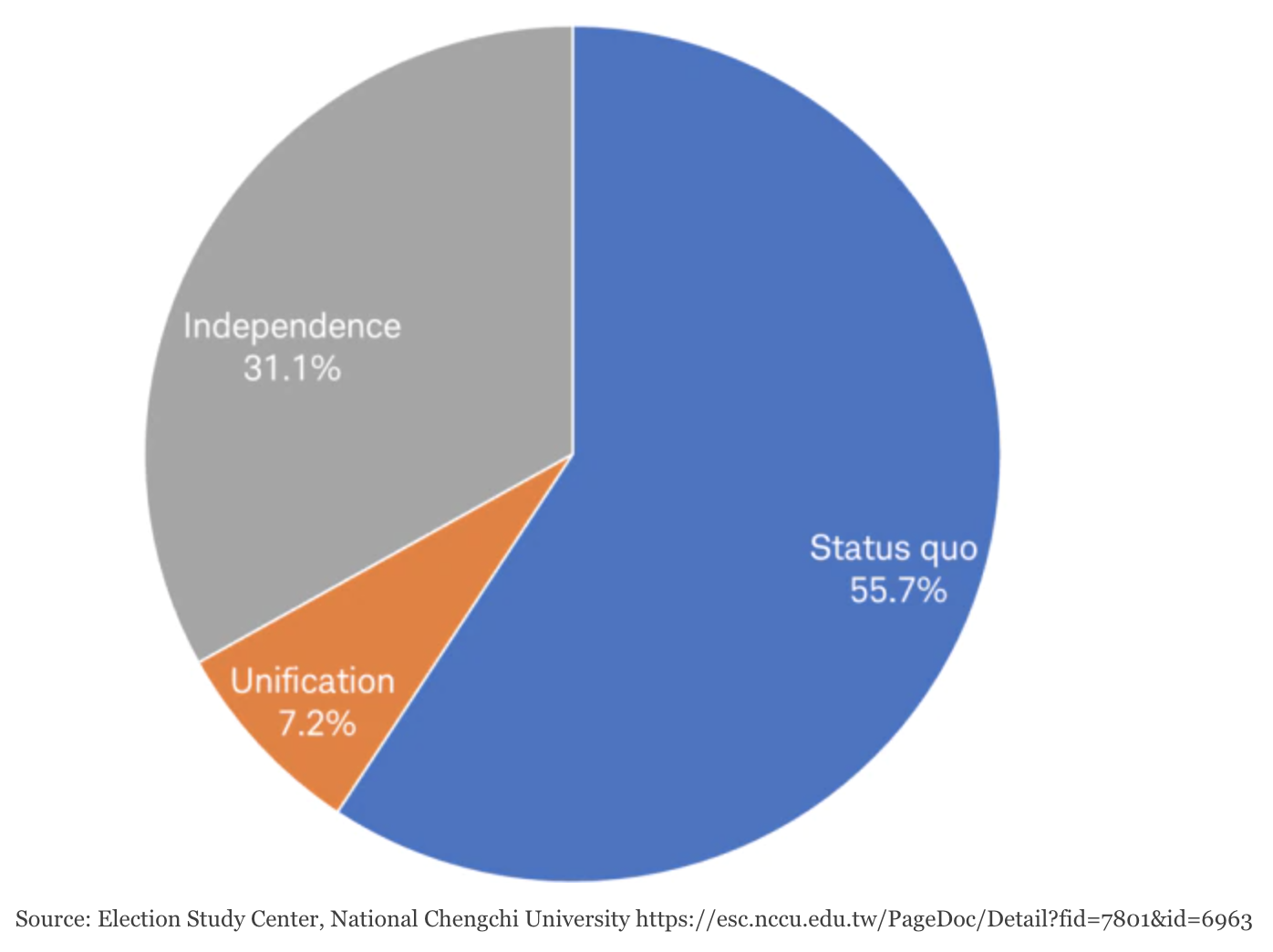

Unlike the situation in Ukraine, a Chinese invasion of Taiwan would most likely bring China’s industry to a halt as semiconductor shipments flatline and might invoke a sympathetic backlash in other Chinese territories and may bring global military action from Taiwan’s allies that are also dependent upon its manufacturing output. Additionally, Taiwan seems unwilling to make moves toward independence that would provoke China. A June 2021 survey conducted by Taiwan’s National Chengchi University showed that only 31% support independence—not enough to empower Taiwan’s leaders to break away from China, despite the impression given by the recent headlines. Most in Taiwan support the status quo, which is China’s preference.

Survey: Taiwan Independence vs. Unification

The kinds of events that could likely push China to take military action against Taiwan include:

- A formal declaration of independence by Taiwan (unlikely given the limited support for independence noted above).

- The end of negotiations surrounding unification by all of Taiwan's main political parties (unlikely since the Chinese Nationalist Party in Taiwan has a friendly stance toward the mainland).

- Formal defense agreements with Taiwan signed by Western allies (possible, but the United States currently does not have such an agreement with Taiwan).

- The widespread acceptance of Taiwan as a country and/or equal partner in multiple international organizations, like the United Nations (50 years ago the United Nations admitted the People’s Republic of China and expelled Taiwan, re-entry is not likely in the near-term).

None of these appear to be on the verge of happening.

Takeaway

We don’t believe that diversified investors need to take actions to protect portfolios from the market risks tied to potential invasion in Ukraine.

Michelle Gibley, CFA®, Director of International Research, and Heather O’Leary, Senior Global Investment Research Analyst, contributed to this report.

© Charles Schwab

Read more commentaries by Charles Schwab