The prospect of rising interest rates has clouded the outlook for global bond investors in 2022, but it’s not all bad news. Our research suggests that strong fundamentals in corporate credit may help investors weather the storm—as long as they are selective about where to take risk.

Inflation and the pressure that it’s putting on central banks to normalize policy frame the outlook for 2022—particularly the early part of the year. After that, we expect global economic growth, though still above average, to slow as higher rates take effect.

Investors in government bonds worry that rising yields will cause capital losses, while investors in corporate bonds worry that slower growth, even at an above-average level, will weaken earnings and make it harder—especially when rates are rising—for companies to service their debt.

Our research suggests, however, that corporate bond issuers in many markets and sectors are well positioned to navigate the uncertainties, for a number of reasons: business dynamics are strong, balance sheets have been improving, risk factors are low or manageable, free cash flow is expanding, and companies are maintaining relatively conservative financial policies.

Earnings and Balance Sheets Improve

Businesses have benefited as economies have re-opened after the first waves of the pandemic. Most of the world’s companies—including US and European high-yield and investment-grade issuers, as well as many emerging-market corporations—are recovering and expanding.

Over the year, we expect many of the sectors now in the recovery phase to enter the next stage of the credit cycle. While progress won’t be uniform across all countries and sectors—Europe’s economy remains sluggish relative to the US, and Asia’s previously strong growth is slowing—it’s likely that most of the world’s corporate credits will be in expansion mode.

Expansion is positive for sales and earnings, but it puts credit investors on their guard. Companies often respond to optimistic outlooks by taking on more debt to fund mergers and acquisitions (M&A), or by increasing returns to shareholders. When the cycle turns down, they might be left with too much debt or too little liquidity, putting them at risk of ratings downgrades and, possibly, defaults.

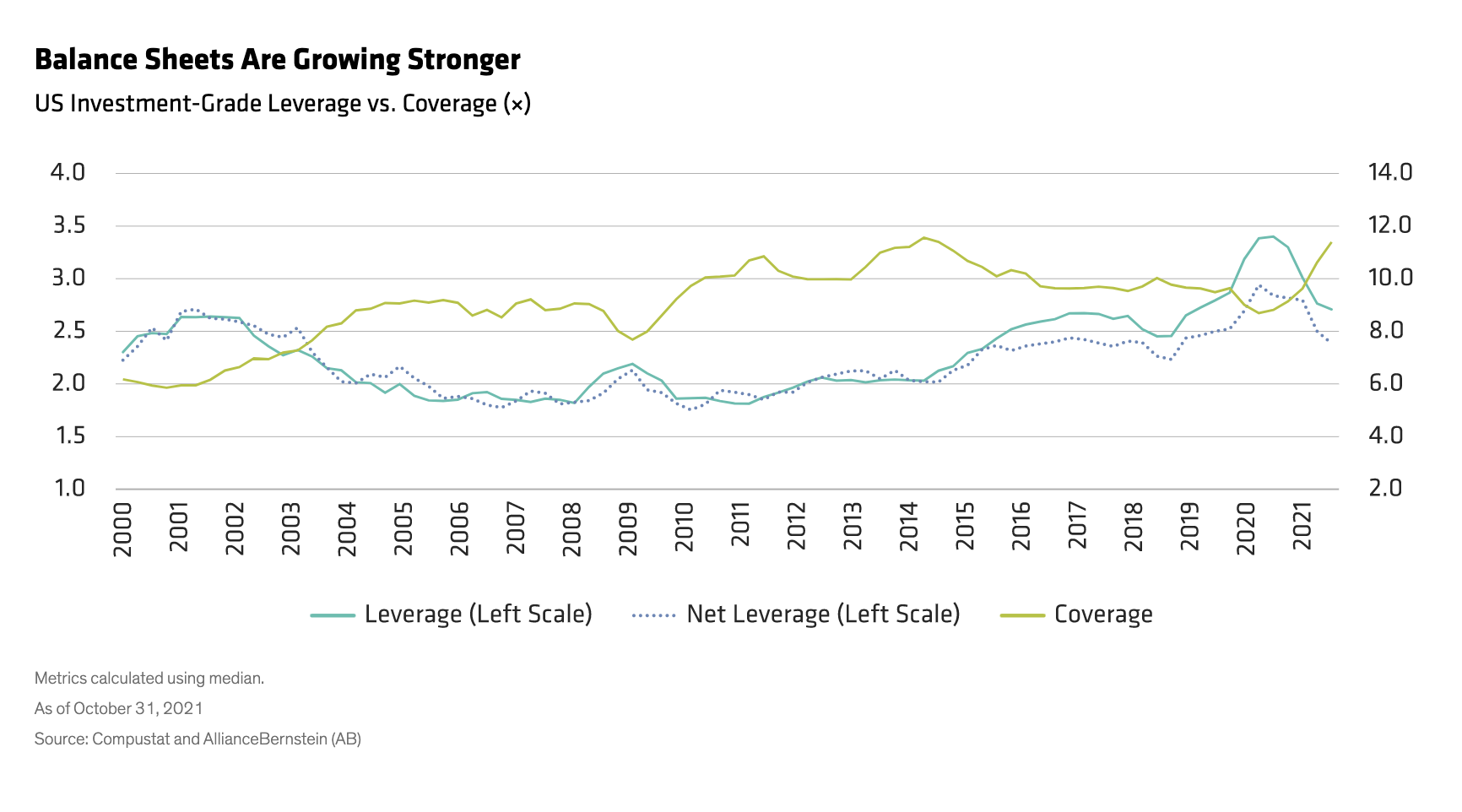

In this cycle, however, the opposite has happened. The uncertainty caused by COVID has led companies to manage their balance sheets and liquidity conservatively, even as sales and earnings have recovered. As a result, leverage has meaningfully improved from the levels it reached early in the pandemic and, where M&A has occurred, it’s had little effect on leverage (Display).

This is also true for US high-yield bonds and for European investment-grade and high-yield debt and helps underpin the global credit sector’s positive outlook.

Forward Ratings Return to Pre-COVID Levels

We assess the health of the corporate credit universe through our proprietary credit ratings for US and European investment-grade and high-yield corporate bonds. As the first wave of COVID-19 took hold in April 2020, for example, our net weighted average forward ratings for US investment-grade bonds fell across 14 out of 19 industry sectors. Now, all but four are back to pre-COVID levels or higher.

Two sectors—consumer cyclical and integrated energy—have higher ratings than they did pre-COVID. Consumer cyclical includes companies like Amazon, which has benefited from the structural shift to online retailing (a trend that seems likely to outlive the pandemic). Integrated energy companies have been helped by strong energy prices, a conservative approach to capital spending and sound balance-sheet management.

The four sectors still rated below their pre-COVID levels are capital goods (Boeing’s challenges are keeping the sector’s weighted average ratings low), oil field services (most companies don’t have the pricing power to benefit from higher oil prices), oil refiners (high oil prices are a headwind) and insurance (COVID-19 mortality rates have hurt life insurers).

M&A Risks to Ratings Are Muted

As noted earlier, we regard the risk of companies overborrowing to fund M&A activity or increased returns to shareholders as low for this stage of the credit cycle. We base this view on trends in liquidity, leverage and coverage, our assessment of companies’ financial policies now and over the next 12 months, and our current and forward credit ratings.

Our classification of financial policies as conservative, neutral or aggressive provides a guide to companies’ likely appetite to borrow more. Currently, in our analysis, financial policy is neutral in half of investment-grade sectors and conservative in the other half. The same would be true for the high-yield market, except that we regard financial policy in one sector—technology—as aggressive.

Over the next 12 months, financial policy is likely to become “more aggressive” (that is, relatively rather than absolutely aggressive) in all investment-grade sectors except communications, where we expect it to remain neutral. In high yield, we expect no change other than in two sectors—basic industry and energy—which are likely to become more aggressive.

To put this in context, our forward credit ratings relative to our (already quite strong) current ratings are stable for more than half of investment-grade issuers, and we expect improvements in credit profiles to outnumber deteriorations in all investment-grade and high-yield sectors but one (investment-grade capital goods).

In other words, not only is the likelihood of re-leveraging for M&A low, but there is also scope for some change in company financial policies without too much impact on credit ratings. This doesn’t preclude activity by private-equity funds with large cash balances pursuing leveraged buyouts, but for now the favorable outlook for corporate fundamentals outweighs the risks of re-leveraging via non-strategic buyers. Further, even where we’ve seen private-equity activity, the impact to bond market metrics has been muted.

An Important Source of Diversification

For credit investors, strong business dynamics, improving balance sheets, manageable risks and conservative financial policies suggest that corporate issuers will be resilient as central banks normalize policy in 2022. In diversified fixed-income portfolios, the different characteristics of duration (government bonds) and credit, and the low correlation between them, are an important source of diversification, particularly during periods of uncertainty. For this reason, we regard the outlook for credit during the next 12 months as encouraging for active investors with a selective approach to risk.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein