Most investors are probably less diversified than they think they are. For one thing, investing in U.S. companies with international sales exposure is not equivalent to international stock exposure. In addition, many major countries (like the U.S.) perform like just one sector of the stock market, leaving investors with a large home bias and potentially a lack of diversification. Finally, the start of a new economic cycle with a rising inflation outlook may signal a switch to international stock market outperformance in the years ahead.

Home bias

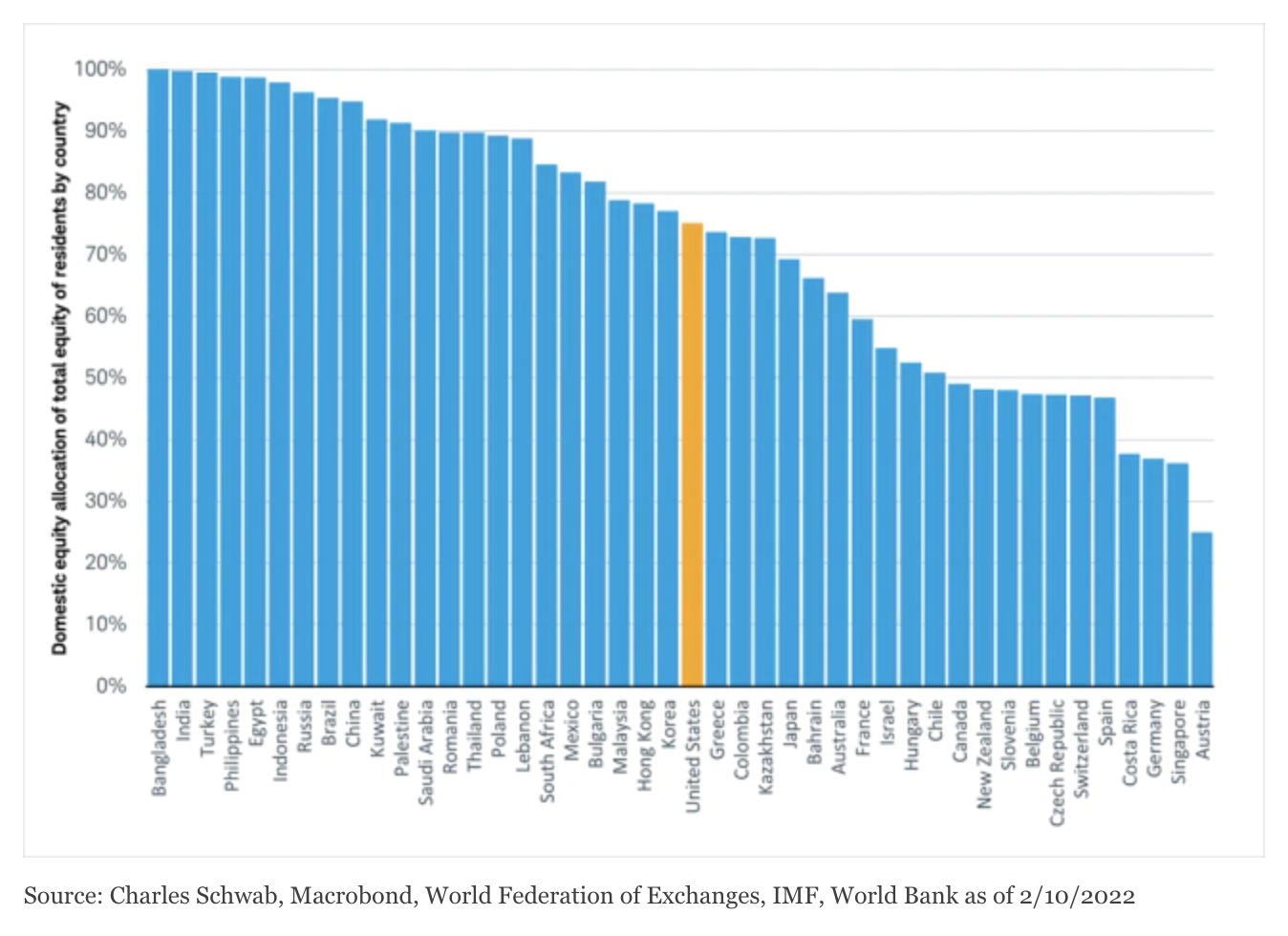

When investors talk about the stock market, they are most often referring to an index that tracks stocks only in their home country. This home bias is often evident in the make-up of investors’ stock portfolios. Investors around the world tend to hold mostly domestic stocks, regardless of their country’s global market capitalization, as you can see in the chart below. U.S. investors, for example, tend to put 75% of their equity holdings in domestic stocks, despite U.S. stocks only making up 58% of global market capitalization. American investors with holdings based entirely in the U.S. are missing out on about half of the world’s investable universe.

Home bias: Investors’ portfolios tend to overweight their home country no matter where they live

Investors with a large home bias are not only concentrated geographically, but also may not be nearly as diversified across sectors as they believe and might risk missing their financial goals as longer-term trends shift with the start of a new global economic cycle.

Can’t get there from here

In a more globally connected world, where items we consume on a daily basis can originate from anywhere, it is reasonable to believe that U.S. firms have international exposure through their sales. Yet, it isn’t possible to simply invest in U.S. companies with international sales exposure and get international stock exposure.

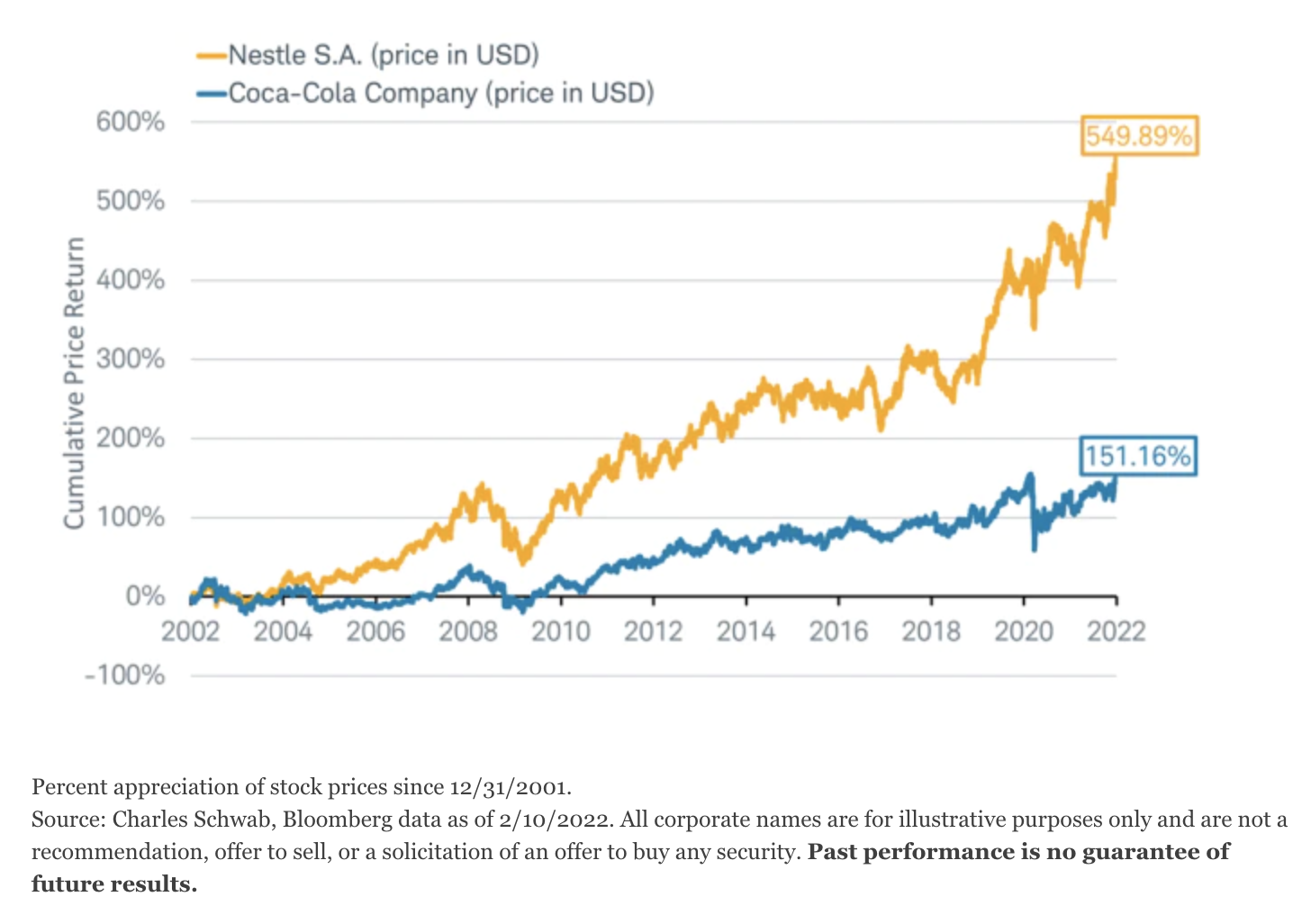

Big companies in the same sector or industry typically serve the same global customer base. For example, U.S.-headquartered Coca Cola and Nestle, a Swiss-headquartered company, have the same geographic distribution of sales by region, to within a few percentage points. They both get about 25-35% of their revenue from the U.S., about 20% from the rest of the Americas, 20-25% from Europe and another 20-25% from Asia, and about 5-10% from Africa and the Middle East.

Coca-Cola and Nestle both sell beverages and snacks to the same folks around the world. This similarity seems to suggest that there shouldn’t be much difference in the performance of stocks in the same industry that are headquartered inside or outside the United States. But, in truth, there is a difference. Over the 20 years ending in December 2021, Nestle’s stock rose 550%, vastly outpacing Coca-Cola’s gain of 151%. Why? Because there are many factors that drive stock performance besides revenue allocation.

Similar customers, different performance

Dollar direction

Returns can also differ across borders due to movement in currencies. By holding an investment denominated in another currency, an investor will experience both the change in the asset price (in that currency) but also the change in the value of the currency, when measuring a portfolio in dollars. Since currency valuation can move as much as the stock price, it’s an important factor to consider. The U.S. dollar is the world’s most-used currency, but that doesn’t mean its value is a constant.

When the dollar falls relative to other currencies U.S. dollar-based investors in international stocks tend to benefit. Here is an example: In July 2020, European stocks fell -1.5%, as measured in euros; the U.S. dollar also fell versus the euro by 4.8%. The overall effect was European stocks posting a gain of +3.3%, as measured in U.S. dollars. That’s a big effect.

Currency contribution

Sector surprise

No one country offers complete global stock market exposure across all sectors. It may be surprising to know how closely some major countries’ stock markets perform like a single sector of the global stock market, and a portfolio with a large home bias may be providing you with an unintended sector concentration.

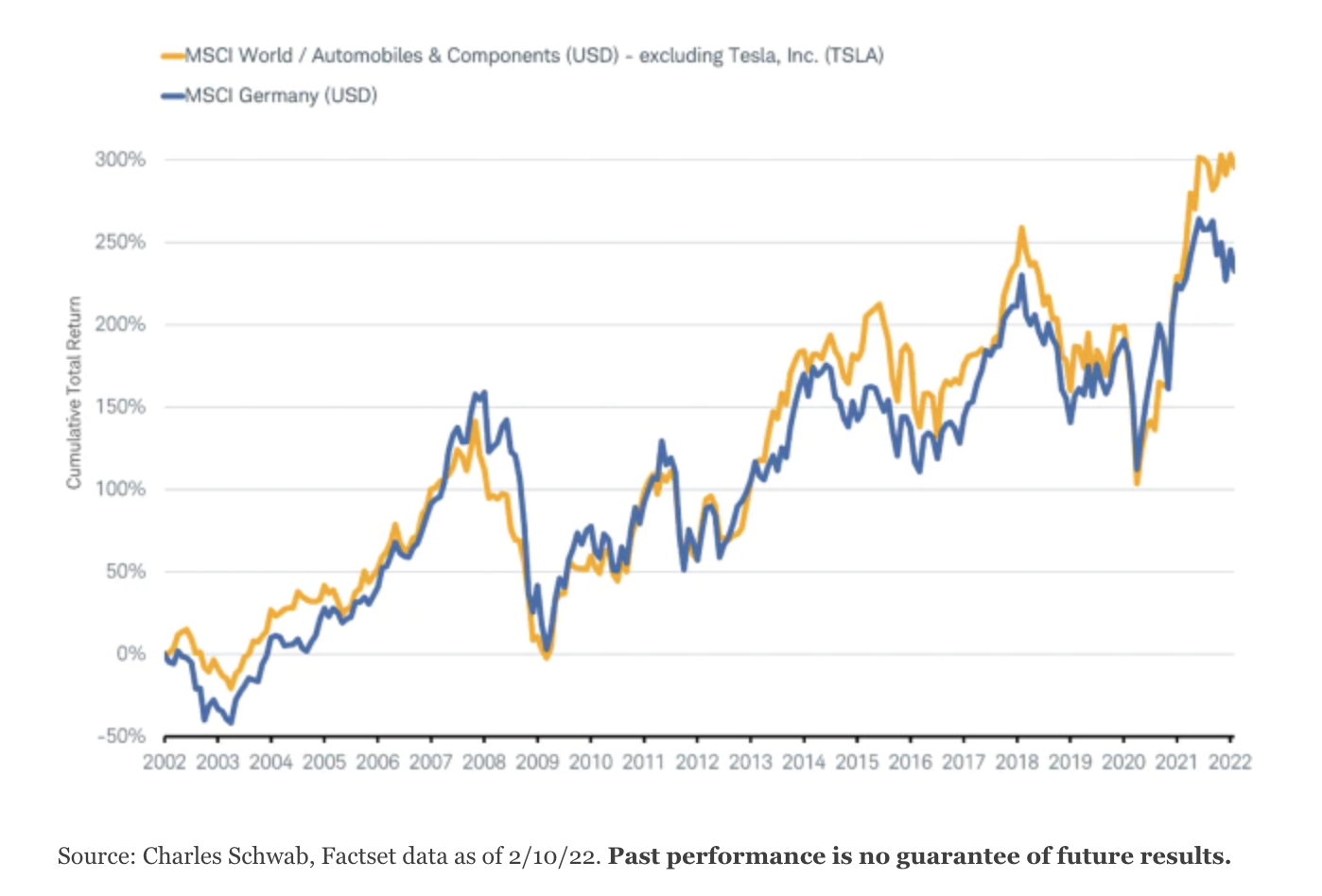

For example, although only 12% of the value of the stocks in the MSCI World Automobiles Index are German companies, the German stock market has closely tracked the performance of auto stocks for most of the past two decades.

Germany driven by autos

Other examples of the lack of diversification owing to high sector correlation among major markets include:

- The Canadian stock market performs much like the energy sector. The Canadian economy is more reliant than most on natural resources, where even the banks are tied to the commodity cycle.

- In Japan, the stock market closely tracks the global financial sector. Even though the financial sector is not the largest in Japan’s stock market, the influence of global financial conditions on all types of Japanese companies is evident in their performance.

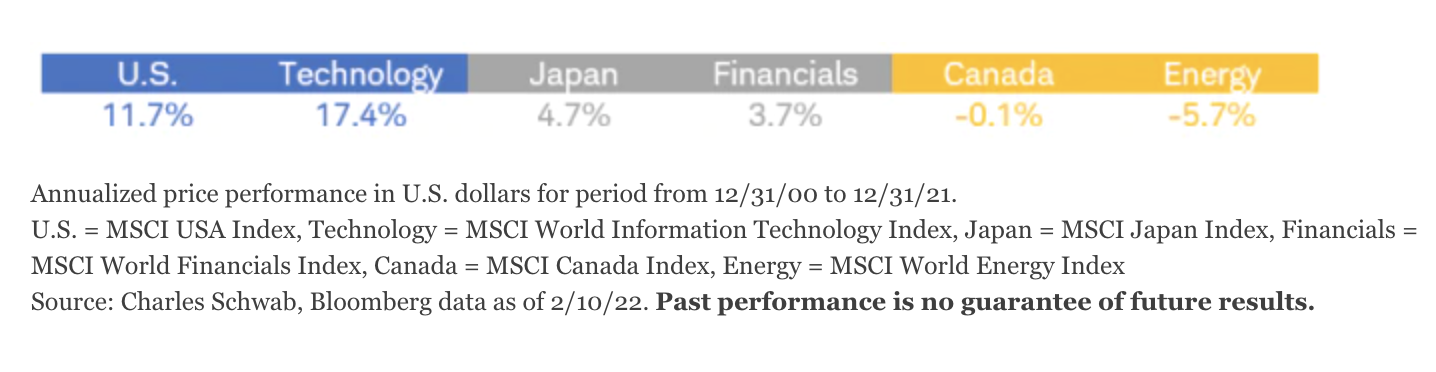

- In the United States, the largest sector of the stock market, technology, seems to drive overall performance. The U.S. market acts a lot like one big technology fund.

Differences in stock market performance by country seem to be driven by these sector influences, more than by politics or economics. The United States has performed the best since the start of the 2000s as it tracked the run up in the world information technology sector. The United States was followed by Canada, fueled by the world energy sector. Japan was the weakest, held back by the poor performance of the world financials sector.

Countries and sectors

Global diversification can help with exposure to whatever sector is performing the best, rather than being tied to the sector that happens to drive the performance of your home country.

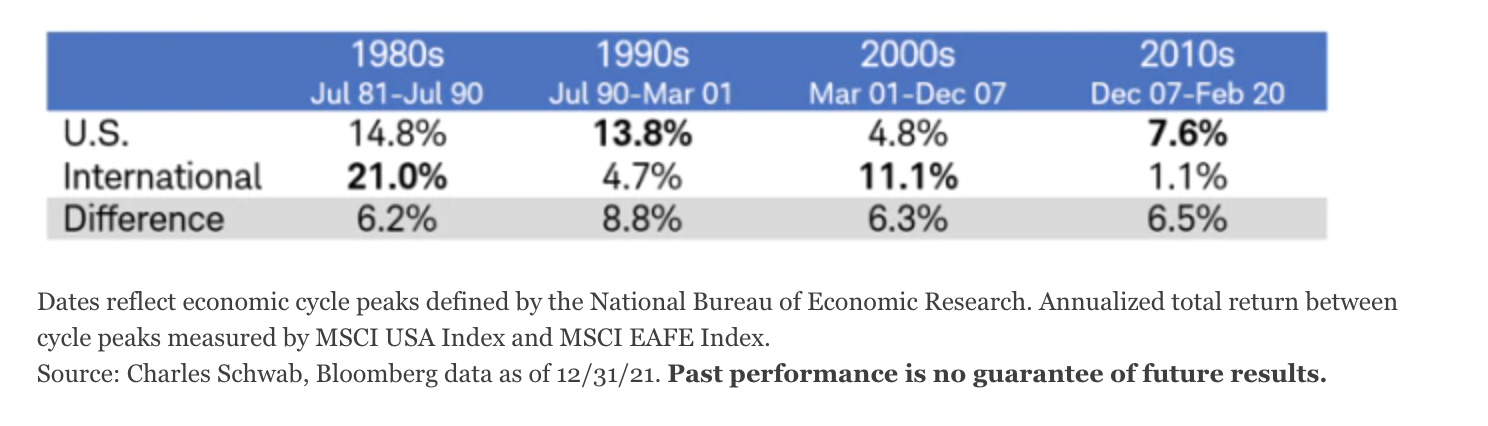

New cycle, new leadership?

Market leadership tends to last for many years, even a decade, before reversing. It usually switches between U.S. and international stocks at the start of a new cycle. For example, after international stocks outperformed in the 1980s, the 1990 recession saw a shift to U.S. outperformance, then the 2001 recession saw a switch back to international outperformance, then the 2008 recession flipped the switch again to U.S. outperformance. These changes in leadership result from behavioral as well as fundamental factors. After a full cycle of outperformance, relative valuations and earnings expectations become stretched and begin to reverse with the catalyst of a new cycle. And now, the start of a new cycle may once again signal a switch to international stocks in the years ahead.

Annualized performance by economic cycle

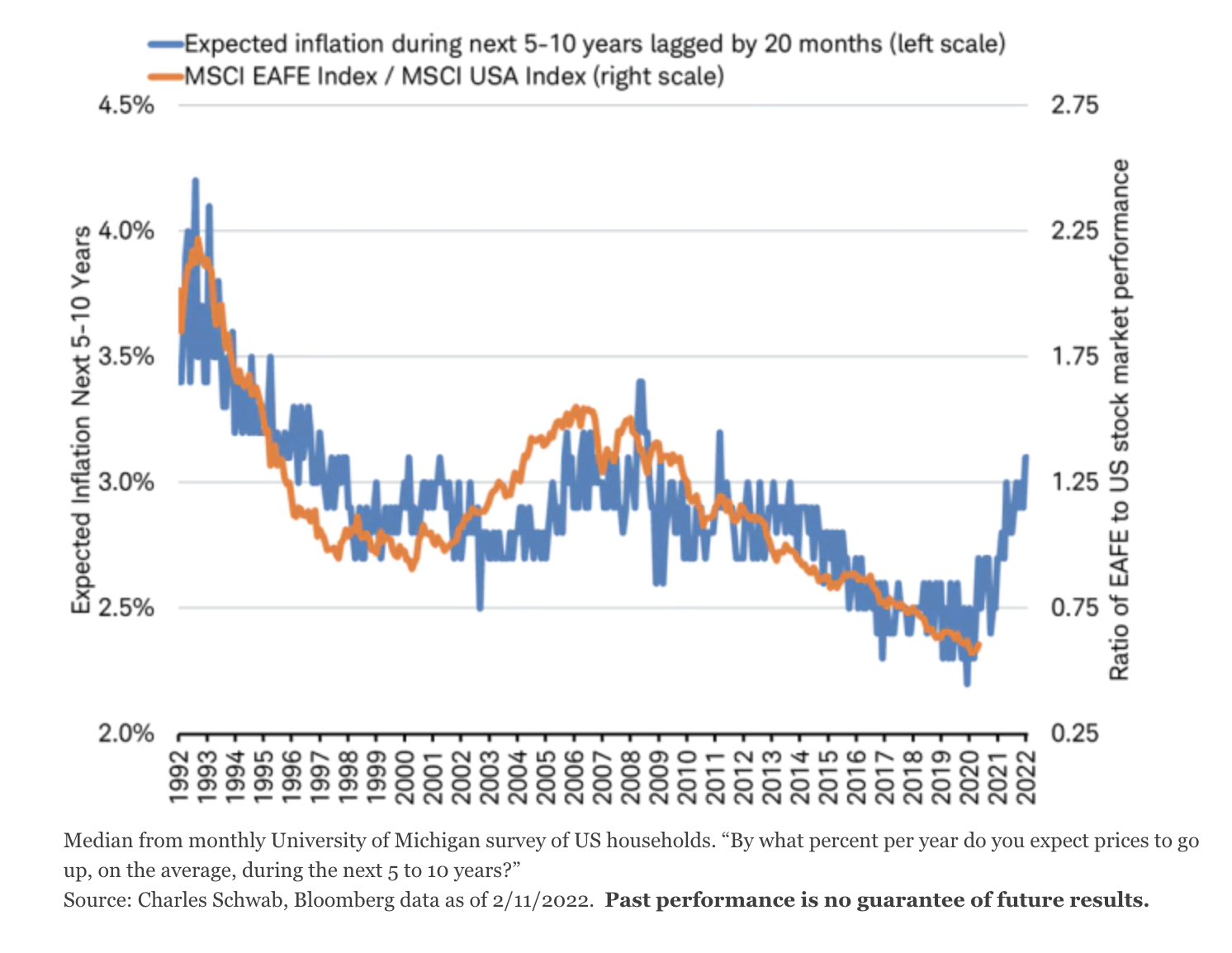

Changing global economic conditions in a new cycle also contribute to a change in leadership. Historically, when long-term inflation expectations are rising, U.S. stocks tend to underperform international stocks with turning points lagging by about two years, as you can see in the chart below. This suggests we may now be at a turning point favoring the relative performance of international stocks due to their greater inflation sensitivity.

Inflation expectations and international stocks’ relative performance

Global investing

Fortunately, as many investors around the world consider reducing their home bias, obtaining global diversification has never been easier or less expensive.

How much exposure outside your home country should you have in your portfolio? The answer depends on your risk tolerance and time horizon. It is clear from the data that most investors can broaden their opportunity set and diversify their portfolios simply by significantly boosting the international portion of their stock portfolios. Now may be a good time to consider rebalancing portfolios back toward international stocks since years of U.S. stock outperformance may have caused a drift away from longer-term targets.

Michelle Gibley, CFA®, Director of International Research, and Heather O’Leary, Senior Global Investment Research Analyst, contributed to this report.

© Charles Schwab

Read more commentaries by Charles Schwab