Preferred Securities: Balancing Yield with Risk

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPreferred securities are a type of investment that generally offers higher yields than traditional fixed income securities, such as U.S. Treasury securities or investment-grade corporate bonds. However, the higher yields come with different risks.

Preferred securities are sometimes considered by investors seeking higher income. They were also one of the hardest-hit investments during the 2008-2009 global financial crisis and in the early stages of the 2020 COVID-19 pandemic. What should you be aware of now to decide whether preferred securities might be the right investment for you for a more-aggressive part of your income portfolio?

What are preferred securities?

Preferred securities are "hybrid" investments, sharing characteristics of both stocks and bonds. In fact, there are many types of preferred securities, each with their own set of characteristics or guarantees. Lately, the term "preferred security" has been used as a blanket term for an investment with a par value of $25, but they can rank as high as a senior bond or as low as traditional preferred stock.1

Bond-like characteristics:

Fixed par value. This is the value for which a preferred can be redeemed by the issuer. Preferred securities often have par values of $25, making it relatively easy for individual investors to invest in given the smaller denomination compared to the $1,000 par value for most corporate bonds. There are preferred securities issued in $1,000 denominations, however, but they tend to be targeted towards institutional investors. While preferreds have fixed par values, their prices still fluctuate in the secondary market.

Regular income payments. Preferreds generally make quarterly income payments, while traditional bonds usually make semiannual payments. Income payments can be either dividend income or interest income, and can be discretionary or non-discretionary, depending on the structure of the preferred.

Credit ratings. Many (but not all) preferreds are rated by agencies like Standard & Poor’s or Moody’s Investors Services.

Maturity date. This is a nuanced characteristic but tends to lean more on the "bond" side of the equation. Preferred securities generally have long maturity dates—like 30 years or longer—or no maturity date at all, meaning they are perpetual in nature.

However, most preferreds have a stated "call date" that the issuer may choose to redeem them, usually at the par value. Preferreds usually have "extraordinary" call features as well, allowing the issuer to redeem the securities for events like a change in the tax regime or capital regulations, but those types of calls are rare. There are a number of reasons why an issuer may call a preferred, but a common rationale is the current level of interest rates. If interest rates have fallen and an issuer can issue a new preferred with a lower coupon rate, it might consider calling in an existing preferred to save on borrowing costs.

Stock-like characteristics:

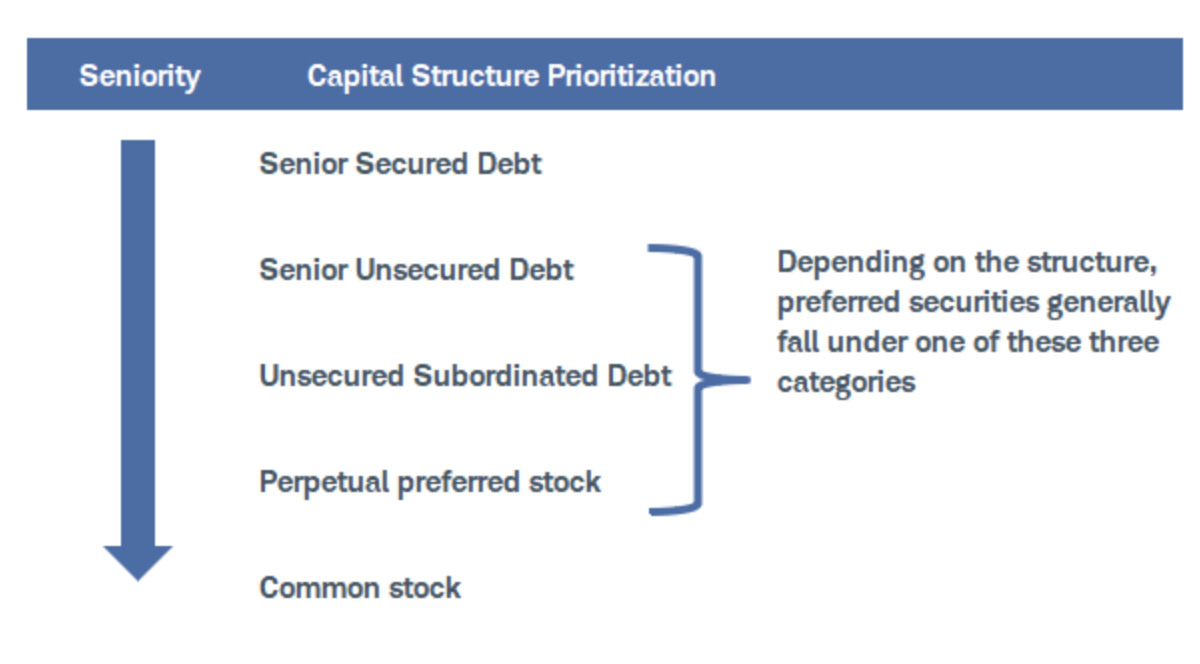

Low ranking. Most preferred securities rank below traditional debt in the issuer’s capital structure. In bankruptcy, for example, corporate bond owners are generally paid before holders of preferred securities.

Preferreds can rank as high as traditional senior unsecured bonds and rank above common stock

Source: Schwab Center for Financial Research and Standard and Poor’s.

Weaker obligations to pay income. Since they rank low in the capital structure, preferred securities generally don’t provide the same guarantees of income payments or payment at maturity as bonds. Income payments on preferred securities are often discretionary, like a traditional stock dividend. A missed interest payment on a bond usually triggers a default, but that’s not the case with many preferred securities. Deferrals of payments don't happen often—partly because a deferral would likely limit the appeal to investors, but also because a company isn't permitted to pay dividends on common stock while deferring payments on any outstanding preferred securities. In other words, payments on preferred securities must come before payments to common stock; hence the name "preferred."

Exchange-traded. Many (but not all) preferreds trade on an exchange, just like traditional stocks.

There is one additional characteristic that can fall under either stocks or bonds: tax treatment. Depending on the structure of the preferred, which we discuss below, the income payments can either be taxed as qualified dividends or taxed as interest income.

Preferreds tend to offer higher yields than traditional bonds due to these complex characteristics. Since they rank below traditional bonds, have very long maturities, and don’t enjoy the same income payment priority as traditional bonds, investors tend to demand higher yields to compensate for those risks.

Types of preferred securities

There are several varieties of preferred securities and the terms used to describe them can be complex. Here are the primary types, beginning with those that rank lowest in the issuer’s capital structure:

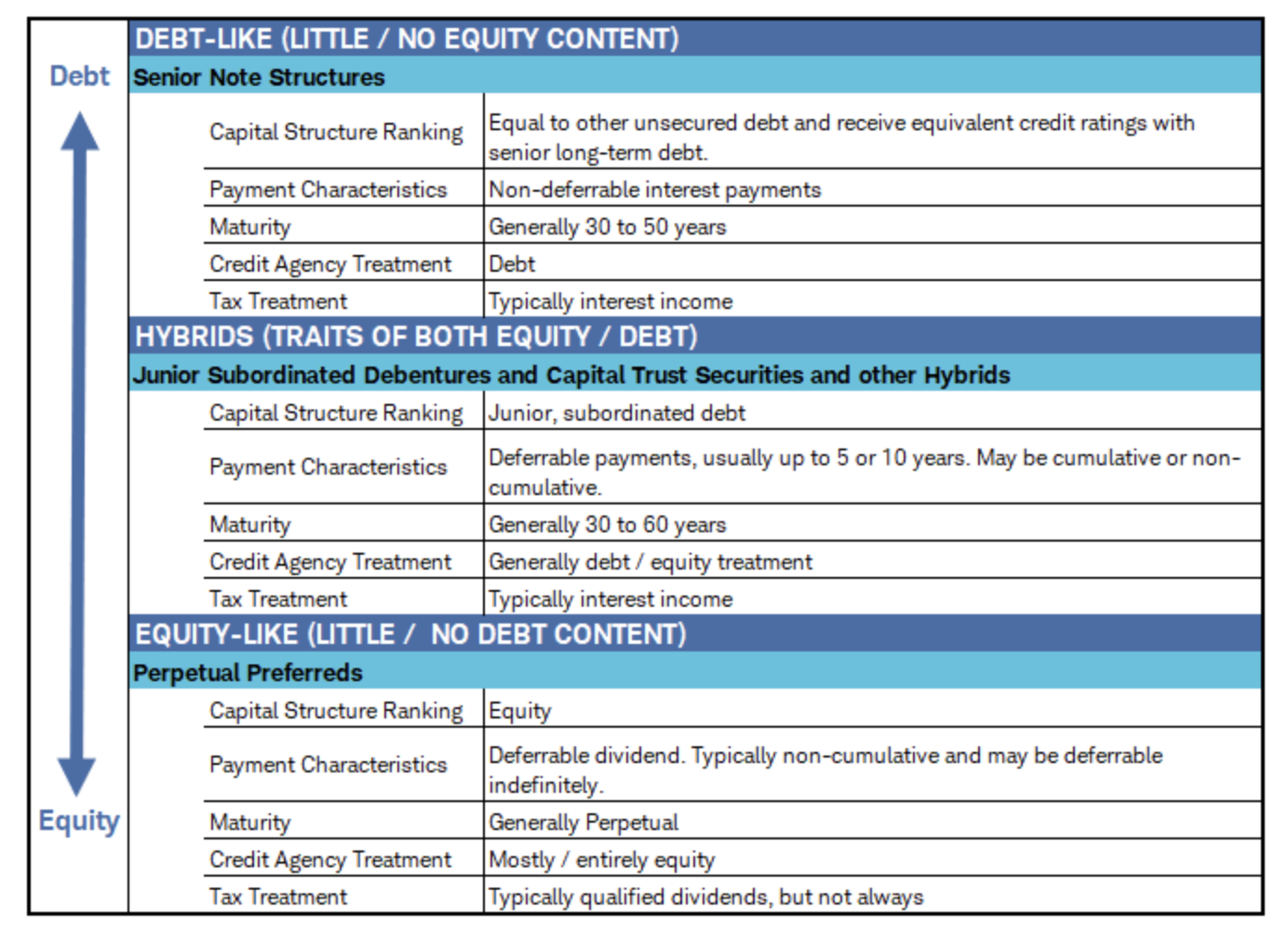

Preferred stock can be considered the most "traditional" type of preferred security, representing ownership in the issuing company. Unlike an issuer's common stock, preferred stock has a fixed par value. Dividends may be suspended at any time and are generally not cumulative, meaning they don't need to be paid back if they are deferred. As equity securities, the coupon payments of some of these preferreds may receive advantageous tax treatment, such as eligibility for qualified dividend income treatment. This is one reason many individual investors historically have chosen preferred stock; however, it's important to read the prospectus to understand whether the payments on any shares that you own are taxed at the qualified rate.

Hybrid preferred securities are next in line. In the firm's priority-of-payment ranking, hybrid preferreds generally rank below the issuer's senior unsecured debt, but above preferred stock. Examples of hybrids include capital trust securities and junior subordinated debentures. The interest payments can be deferred and can be either cumulative or non-cumulative. If payments are deferred for cumulative preferred shares, the coupons accumulate and must be paid back later, short of bankruptcy or default. This adds a bit of extra protection for investors, as well as incentive for the issuing companies to keep making payments, since they know they'll have to pay them eventually.

"Non-cumulative" means that if payments are deferred, they don't accumulate and won't be paid back later. This is a particularly unattractive feature, warranting higher yields for investors. Also keep in mind that deferred payments from hybrid preferreds can generate a "phantom" income tax, which makes the holder liable for income not yet received. Hybrid preferreds tend to pay interest, not dividends. They usually have fixed (though generally long) maturity dates compared to preferred stock, which is perpetual by nature. The income payments from hybrid preferreds tend to be taxed as interest income.

Baby bonds, or senior notes, are just that: senior unsecured obligations of the issuer. Like bonds, they pay interest, and any missed payments constitute a default. Unlike bonds, they usually have a par value of $25 instead of $1,000, and they usually trade on an exchange.. Just like income payments from a traditional corporate bond, the income payments from baby bonds are generally taxed as interest income.

Typical preferred security structures

Source: Schwab Center for Financial Research.

Why do companies issue preferred securities?

Companies generally issue preferred securities for flexibility. The primary issuers tend to be financial firms, such as banks or real estate companies, which need easy access to debt markets to operate. But other companies, such as utilities and industrial companies, often issue preferred securities as well. Preferred securities provide these companies with flexibility as an extra financing tool in addition to common stock and more-traditional corporate bonds.

Banks, which have strict regulatory requirements, are also able to use preferred securities as a source of capital "cushion" between their bonds and common stock. Bank regulations require certain levels of capital reserves, and preferreds can help meet that objective. The degree of capital treatment varies depending on the type of preferred security.

Preferreds do come with additional risks

Higher yields may be appealing, but they almost always come with the additional risks described below. However, lower yields that other investments offer can also be risky—in terms of maintaining purchasing power, meeting living expenses and so on. So there are tradeoffs. Which risks are most important to you?

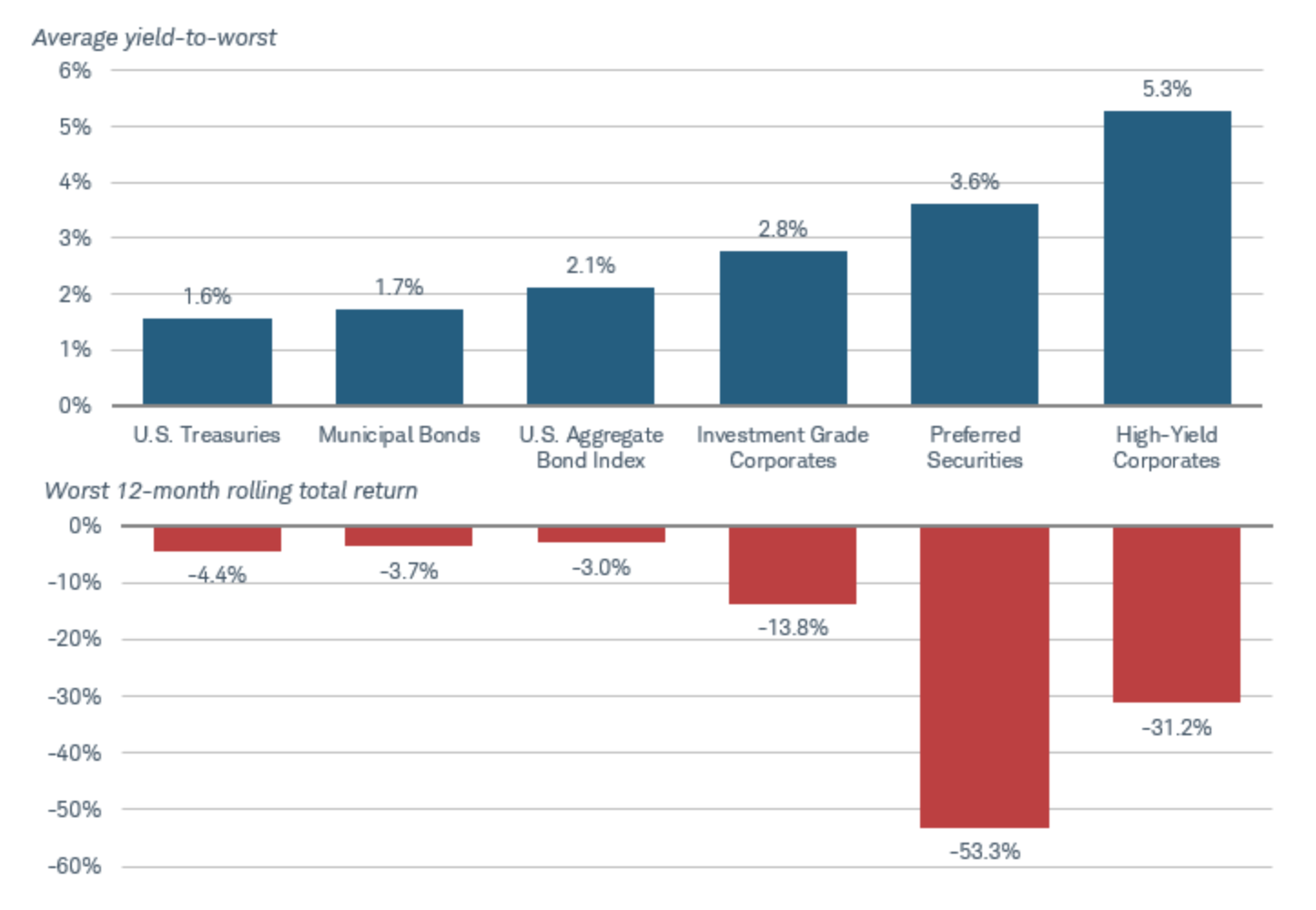

Risk of large drawdowns. This doesn’t necessarily happen often, but preferred prices can fall sharply if market conditions deteriorate. That happened during the global financial crisis in 2008 and then again in the first few months of 2020 during the early stages of the COVID-19 pandemic.

Higher yields come with greater risks

Source: Bloomberg, as of January 31, 2022. Worst rolling 12-month total returns are from 12/31/99 to 1/31/22 using monthly data. Indexes used are the Bloomberg U.S. Treasuries Index (LUATTRUU Index), Bloomberg Municipal Bond Index (LMBITR Index), Bloomberg U.S. Aggregate Bond Index (LBUSTRUU Index), Bloomberg U.S. Corporate Bond Index (LUACTRUU Index), ICE BofA Fixed Rate Preferred Securities Index (P0P1 Index), and the Bloomberg U.S. Corporate High-Yield Bond Index (LF98TRUU Index). Past performance is no guarantee of future results.

Fewer diversification benefits than traditional bonds. High-quality bonds, like U.S. Treasuries, tend to have a low or negative correlation with stocks, so adding Treasuries to a portfolio can provide diversification benefits, helping limit volatility.2 That’s not the case with preferreds. Preferreds generally have a stronger relationship with the stock market than the bond market. That can be good when stocks are rising, but it can hurt portfolios if stock indexes are falling. This is important when building a well-diversified portfolio because preferred securities don’t offer the same diversification benefits that highly rated bond investments can provide.

Sector concentration in banks and finance companies. If you buy individual preferreds, this can lead to inadvertently concentrating your portfolio in specific financial firms as well as in the financial sector as a whole. When investing with individual preferred securities, we suggest limiting exposure to any single issuer to no more than 10% of your portfolio.

Lower credit ratings than the issuer's bonds. An issuer's preferred securities will usually have a lower rating than the firm's senior, unsecured bonds. Also, preferred securities are often compared to sub-investment grade, or high-yield, bonds, given the higher income opportunities. But remember, high-yield bonds, by definition, carry speculative-grade ratings, so they do come with credit risk. Investors who research carefully can still find preferred shares from investment-grade companies, thus providing higher credit quality than junk bonds. Many preferred securities these days, however, are rated "BBB" (the lowest rung of the investment grade spectrum) or "BB" (the highest rung of the sub-investment grade spectrum.)

High interest rate risk. Since preferred securities have long maturities, or no maturities at all, they tend to have high interest rate risk, or the risk that prices will fall when yields rise. Given that, preferreds should always be considered long-term investments since fluctuating interest rates can have outsized effects on preferred security prices

Overall, investors with higher appetites for credit risk may consider allocating up to 20% of their overall portfolio to more aggressive income investments. Along with preferred securities, that could include high-yield bonds, bank loans, or emerging market bonds.

Again, preferred securities may not be appropriate for all investors. Those who do choose them should learn about some of the risks and use them strategically as a higher-risk part of their income portfolio.

Find out more about individual preferred securities

Finding good information about preferred securities can be difficult, and there are many details to understand before investing. The best source of information will always be a security's prospectus, which you can obtain from a Schwab fixed income specialist, or from data repositories available online. Schwab clients can access our Preferred Stock Screener.

Don't just screen for the highest yields—also screen based on attributes such as credit rating, and then augment it with more information about the issuing company, the security listed, specific characteristics of the preferred shares (whether they coupon payments are cumulative or non-cumulative, for example, which is often listed in the security description) as well as call dates and other details. Don’t just look at the issue’s current yield—if a preferred is priced above par, it’s important to find out its yield-to-call. A preferred with a price above its $25 par value that has an upcoming call date may result in a negative total return if it’s redeemed at that call date. A fixed income specialist can help identify that yield.

If you'd like a diversified solution without too much exposure to any single preferred stock or issuer, consider preferred-stock exchange-traded funds (ETFs) or mutual funds. Clients can search for "preferred stock" funds in the "taxable bond" category using the Schwab ETF Screener or the Schwab Mutual Fund Screener. Clients can also consider a separately managed account for an allocation to preferred securities, but keep in mind that they have higher investment minimums than ETFs or mutual funds.

¹ Par value, also known as face value, is the amount the issuer promises to pay the bondholder when the bond matures.2 Correlation is a statistical measure of how two investments have historically moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits