The Russian invasion of Ukraine overturned a lot of assumptions about the near-term direction of the global economy. “Black swan” events like this don’t happen often, but we’re in the middle of one now, and the situation is changing daily.

For global stocks, the key question is whether the conflict will result in a European recession. Historically, global stocks have recovered and posted gains after periods of armed conflict—except when a recession followed. U.S. stock market investors are keeping a close eye on soaring energy prices and rising inflation, which typically hurt household spending. The U.S. household savings rate is already at its lowest point since 2013, providing little cushion for consumers.

Meanwhile, the Federal Reserve is caught in the middle just before a March 15-16 meeting at which it has been widely expected to begin raising rates. The Fed has been signaling tighter monetary policy for months, and if it fails to follow through, it could lose its inflation-fighting credibility. On the other hand, if it tightens policy too much or too fast, it could push the economy into a recession.

The conflict also was a catalyst in ending the perennial standoff in Washington over the federal budget. More than $13 billion in aid for Ukraine was added to the massive government funding bill, and a bipartisan desire to get aid to Ukraine quickly led to the massive spending agreement getting across the Congressional finish line.

Global stocks and economy: War in Eastern Europe

The Russian assault on Ukraine continues to intensify, with attacks on cities and infrastructure. Russia seems determined to continue the assault, and while NATO military action remains unlikely, further steps on sanctions look increasingly inevitable. Europe is the main focus of investor concern due to its proximity to the conflict and its dependence on Russian energy. The escalation raises the potential for further energy price inflation and economic recession in Europe.

Over the longer term, a lengthy history of geopolitical events suggests that diversified investors may not need to take defensive actions in their portfolios—unless we enter a recession. Stocks recovered and posted gains after periods of armed conflict during the past 30 years (1991, 2001, 2003, 2014), except when a recession followed (2008). These conflicts differed, but there were similarities in their economic backdrop and all of them involved major energy exporters. For example, recessions preceded the conflicts in 1991 and 2001. Oil prices doubled in the runup to the conflict in 2003. Economic sanctions on Russia were applied in response to the wars in 2008 and 2014. The Fed prompted a “taper tantrum” when it signaled tightening ahead of the conflict in 2014. This means a key question for investors is: Will the current conflict result in a recession?

Performance of European stocks surrounding periods of armed conflict

European stocks measured by STOXX 600 Europe Index.

Source: Charles Schwab, Macrobond data as of 3/9/2022. Past performance is no guarantee of future results.

Europe’s economy is currently being challenged by higher energy prices and tighter lending conditions in the wake of the Ukraine invasion. Energy prices have the potential to rise, with or without sanctions, if global deliveries of Russian energy products are refused in a de-facto boycott. This could result in higher costs for companies in many sectors.

Yet, there are some factors mitigating the odds of recession:

- The European economy strengthened in February as the economy rebounded from an omicron-driven slowdown. Measured just before the invasion, the composite purchasing managers index (PMI) for February rose to 55.5, a level historically consistent with an above-average 2.6% pace of gross domestic product (GDP) growth.

- Uncertainty makes a rate hike by the European Central Bank less likely, meaning current monetary policy support stays in place. So far, financial conditions have tightened rapidly but remain within the range of non-recessionary periods of the past 10 years.

- European governments are further boosting fiscal spending, illustrated by Germany’s €100 billion increase in defense spending.

- European consumers have excess savings well above average resulting from the COVID-19 restrictions, helping cushion the impact of higher consumer energy prices on overall spending.

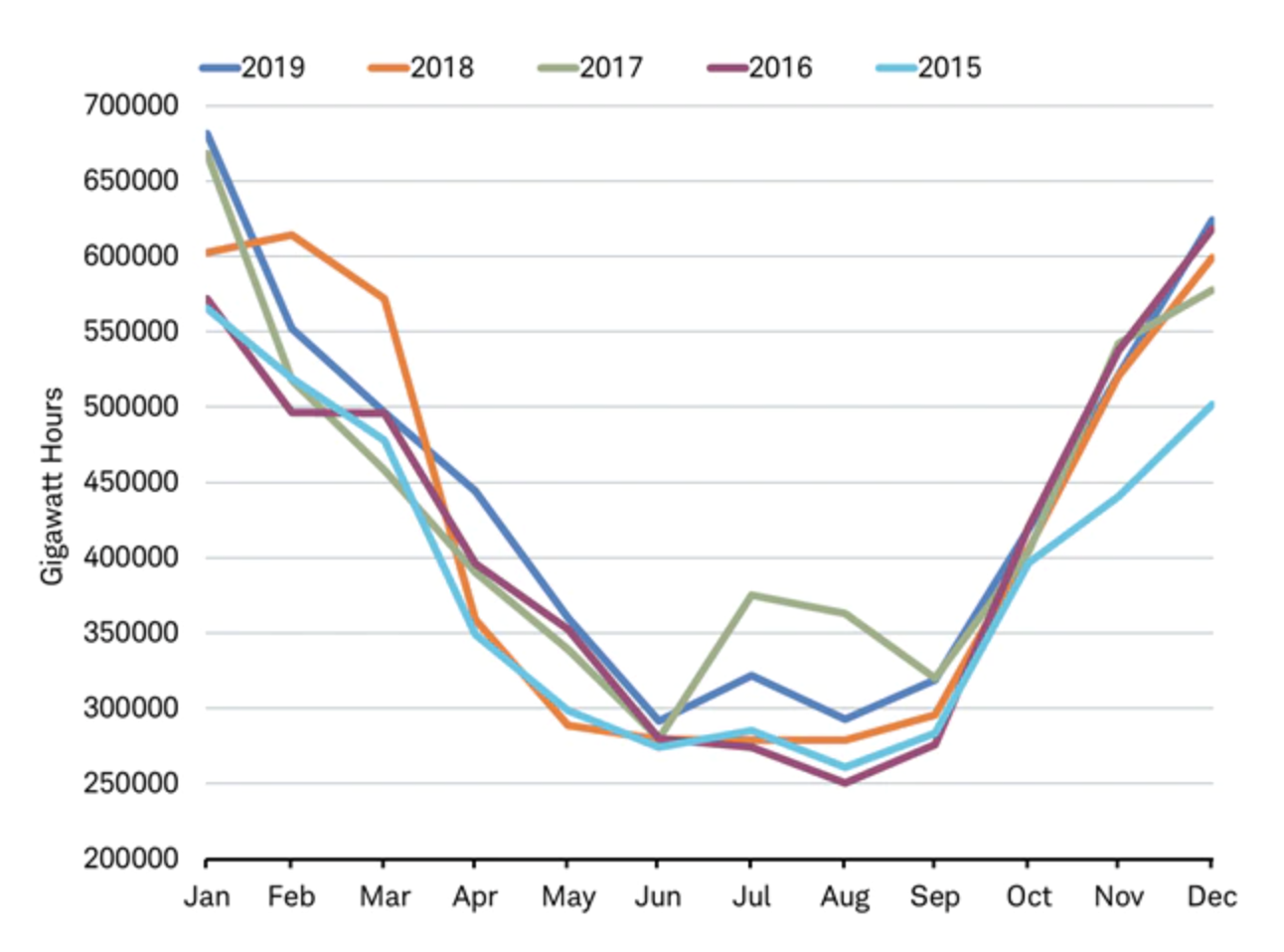

- Natural gas consumption in Europe, where the pressures on energy supply are most acute, is in seasonal decline as prices surge. The chart below shows the seasonal pattern of gas use in Europe over the past five years prior to the pandemic and how it tends to fall by half from Jan/Feb to Apr/May.

Natural gas use in Europe seasonally declines as winter ends

Source: Charles Schwab, Bloomberg data as of 3/4/2022.

The escalation raises the potential for higher inflation and an economic recession in Europe. Any de-escalation could lead to a relief rally and the release of pent-up consumer demand. Having a high degree of confidence in any particular outcome in the near term, for better or worse, is challenging.

Fixed income: Central banks in a bind

The Russia-Ukraine war has resulted in two seemingly contradictory market reactions: rising inflation and lower bond yields. Commodity prices have soared as sanctions on Russia reduce the flow of energy products, metals and grains to the global markets, sending inflation sharply higher. However, the supply-side shock produced by the crisis is simultaneously reducing growth expectations and boosting demand for safe-haven assets like U.S. Treasuries. This leaves the Federal Reserve and other major central banks in a bind.

Late last year, the Fed was surprised by strong growth coming out of the pandemic and rising inflation due to limited supplies of goods. It was clear that the policy setting for the U.S. was too easy given the strength of the economy, and the Fed indicated in December that it was going to shift to tighter policy in early 2022. Fed Chair Jay Powell expressed that the committee wanted to return its policy setting to “neutral”—a level that is appropriate for steady economic growth without generating inflation. The Fed’s longer-run target for the neutral rate is 2.5%. Given the prospect of a series of rate hikes, bond yields were on the rise, with 10-year Treasury yields rising above 2%.

Ten-year yields had been rising

Source: Bloomberg. U.S. Generic 10-year Treasury Yield (USGG10YR INDEX). Daily data as of 3/7/2022.

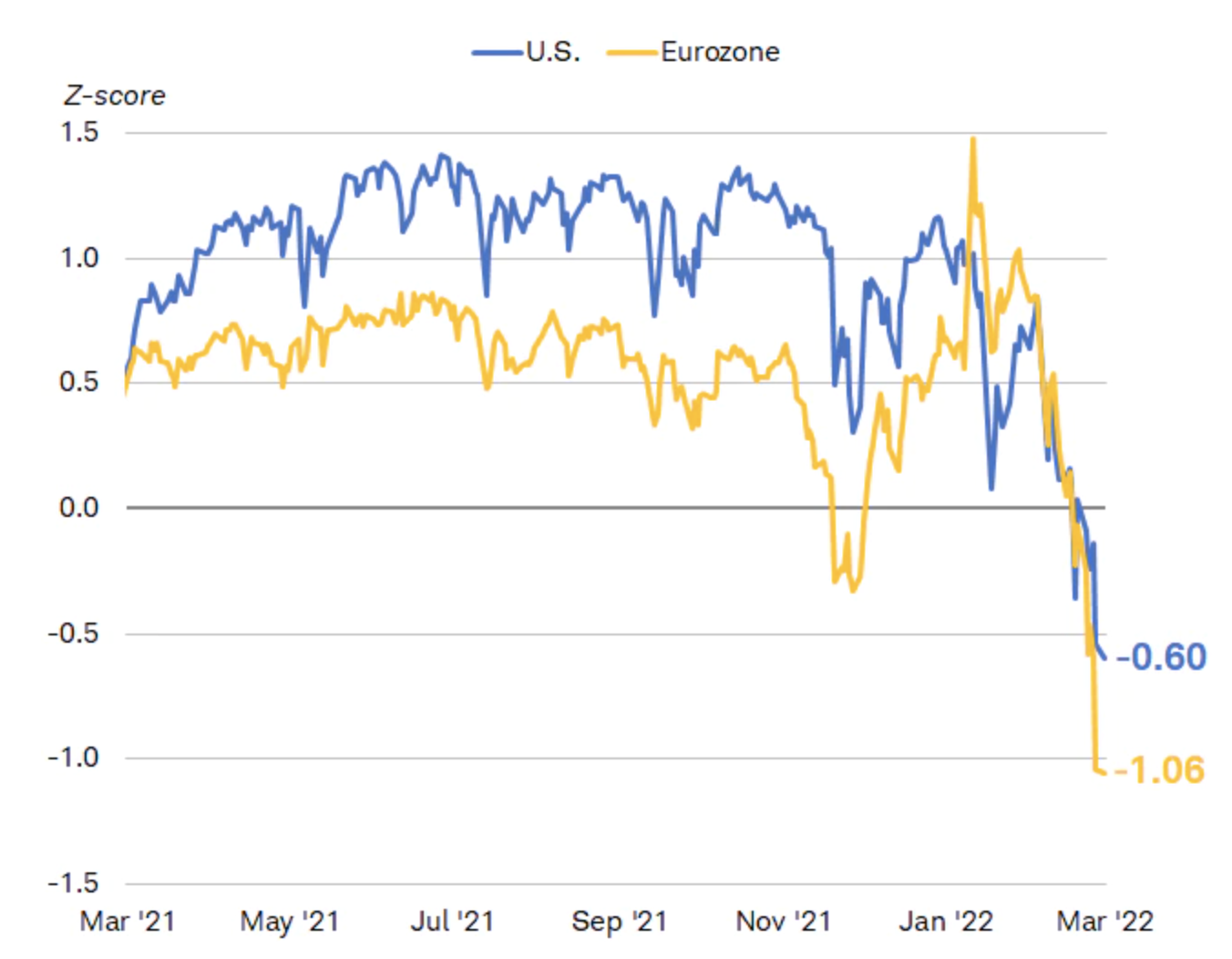

Now we’re in a different world where the global economic outlook is much weaker. High energy costs will likely act as a tax on consumers and reduce business investment longer term. Moreover, financial conditions are tightening on the back of a stronger dollar and widening credit spreads as investors become more risk-averse. Tighter financial conditions often precede slower growth.

Financial conditions in the U.S. and Europe are tightening rapidly

Source: Bloomberg. Bloomberg U.S. Financial Conditions Index and Bloomberg Eurozone Financial Conditions Index (BFCIUS Index, BFCIEU Index). Daily data as of 3/7/2022. The Z-Score indicates the number of standard deviations by which current financial conditions deviate from the average. A positive value indicates accommodative financial conditions, while a negative value indicates tighter financial conditions.

With that backdrop, the Fed is in a tough spot. If it fails to follow through on tightening, it could lose its inflation-fighting credibility. On the other hand, if it tightens policy too much, too fast it could push the economy into a recession. Moreover, it will be tightening policy during a period of turmoil in global markets that will likely lead to lower growth and reduced liquidity.

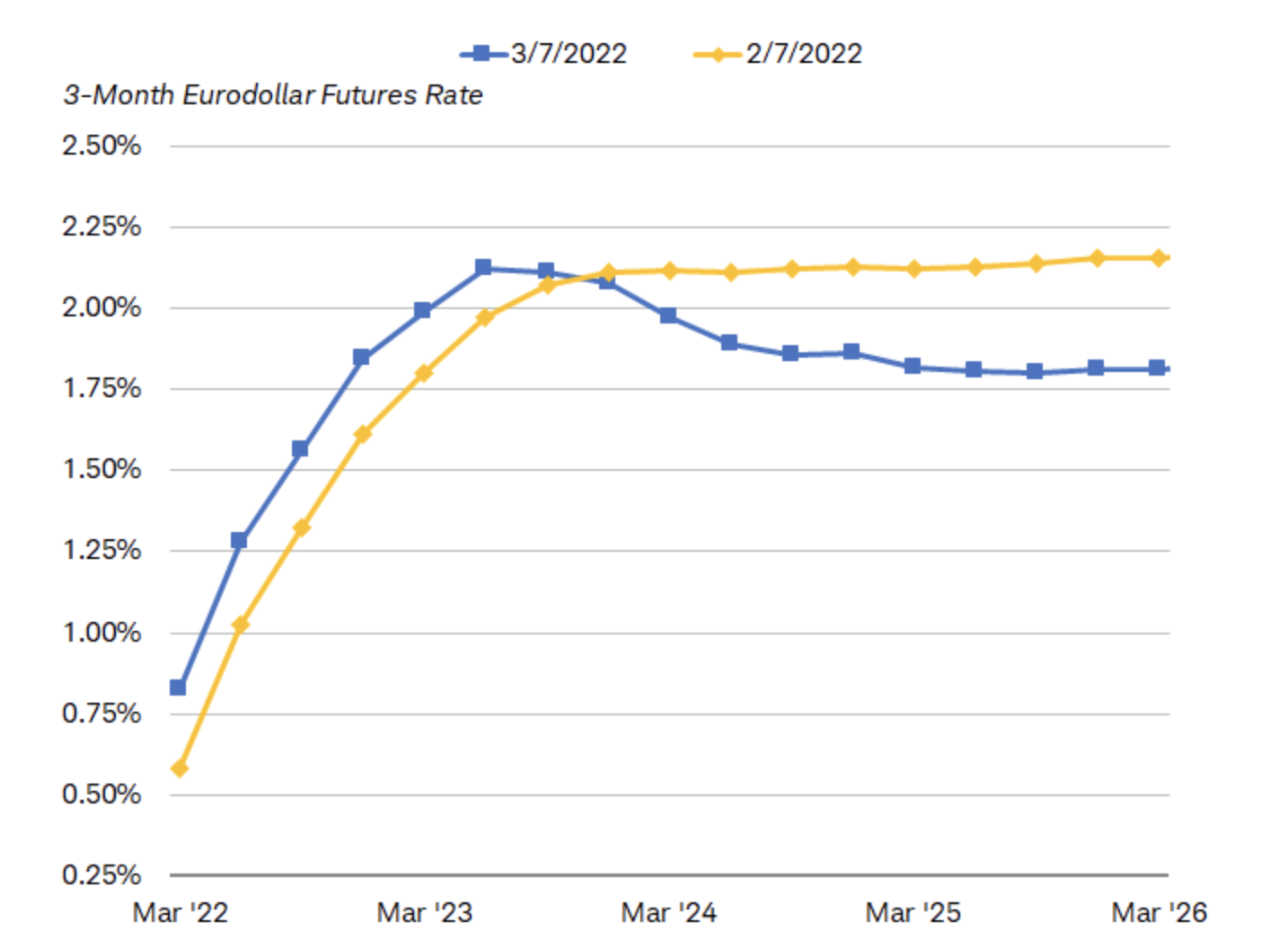

Markets are already showing doubts about the ability of the Fed to reach its “neutral rate.” The implied path of short-term interest rates has shifted in the past few weeks. The five-year forward short-term interest rate (which measures the expected inflation rate over the five-year period that begins five years from today) has dipped below the one-year forward rate. In the past, that has happened near the peak of Fed tightening cycles—not before they begin. Based on the futures market, expectations are for the Fed’s rate hikes to peak in 2023 and then decline.

Markets expect the federal funds rate to peak in mid-2023

Source: Bloomberg. Market estimate of the federal funds rate using eurodollar futures. Eurodollar futures typically price at levels that reflect implied rates in the forward rate market, which indicates where market participants expect short-term rates to be in the future. As of 3/7/2022.

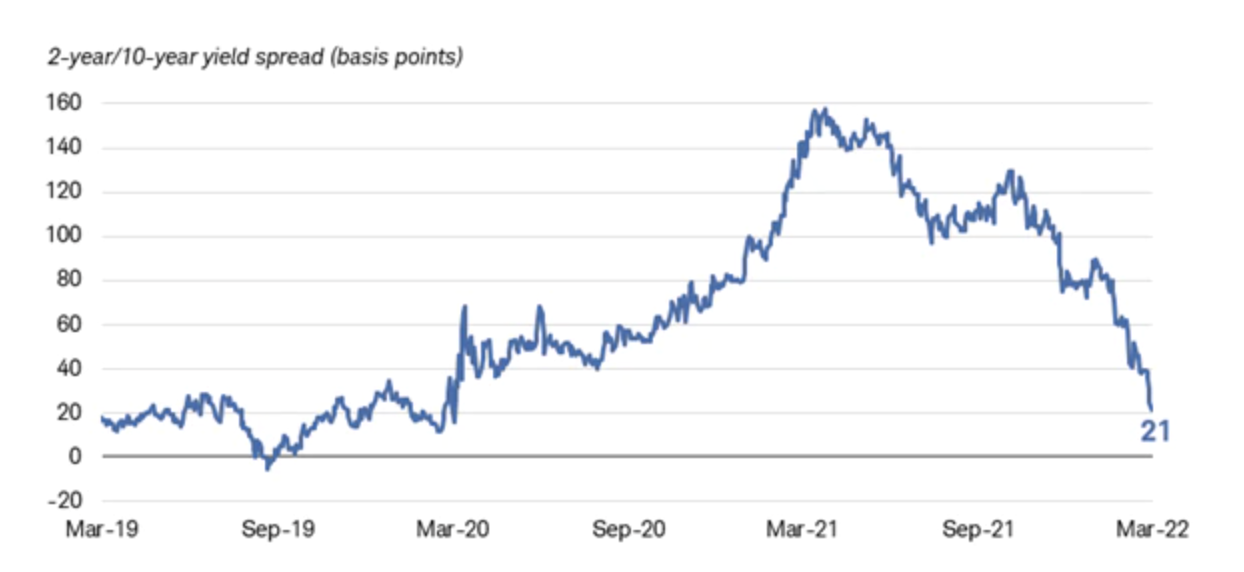

Moreover, the yield spread between 10-year and two-year Treasury securities has fallen to less than 25 basis points, below the zone that often signals policy is tightening too fast. Historically an inverted yield curve has been a reliable recession indicator.

The yield curve is flattening

Source: Bloomberg. Daily data as of 3/7/2022.

Note: The rates are composed of Market Matrix U.S. Generic spread rates (USYC2Y10). This spread is a calculated Bloomberg yield spread that replicates selling the current two-year U.S. Treasury note and buying the current 10-year U.S. Treasury note, then factoring the differences by 100.

The Fed does have options. It could announce a “dovish rate hike.” In other words, it could follow through on the 25-basis-point rate hike widely expected on March 16 but indicate it is still assessing the path going forward given the uncertainties growing out of the war. It could also postpone or slow the pace of its planned balance sheet reduction until the “fog of war” clears. However, it’s a high-wire act.

If the Fed indicates it is ready to move ahead with an aggressive tightening in monetary policy, we expect long-term yields to fall on the risk that the Fed’s moves would trigger a recession. If the Fed indicates a more cautious approach, long-term yields might rebound. The Fed and bond markets are now in a position of reacting to the Russia-Ukraine war.

U.S. stocks and economy: Infectious energy

The Russian invasion of Ukraine—and the subsequent economic and financial ripple effects—has become the chief driver of the market’s swift and volatile moves (to the downside and upside) since the end of February. Volatility has spiked across virtually every asset class, with ruptures in the commodity space sparking the latest discomfort.

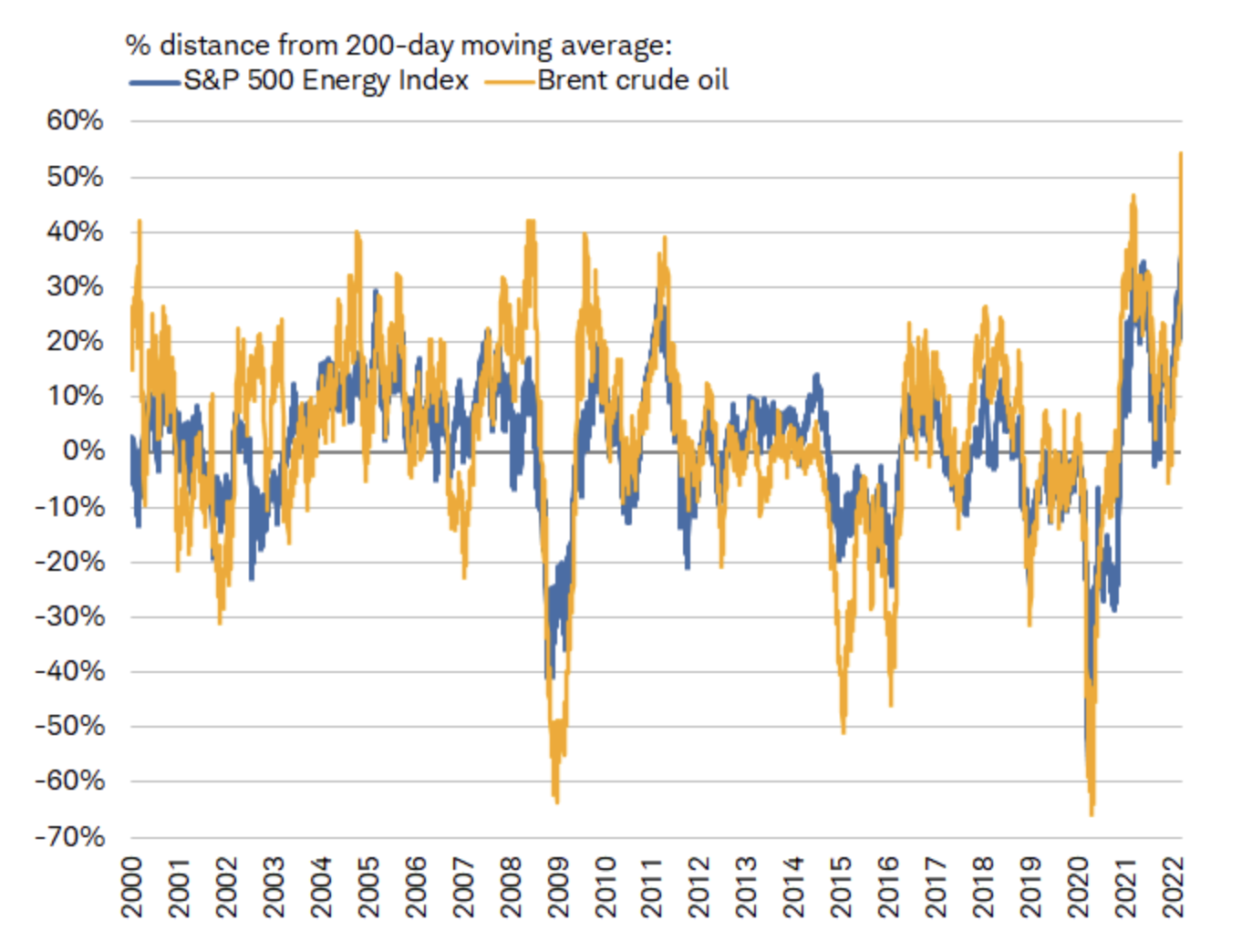

Until Tuesday, when the U.S. announced it would ban Russian energy imports, Western sanctions on Russia had excluded the energy sector, mainly due to several European countries’ high dependence on Russian oil and natural gas. But Brent crude oil prices soared anyway, as investors priced in the possibility of sanctions and supply disruptions. In fact, the price per barrel recently surged beyond its 200-day moving average by more than 50%, as you can see in the chart below.

Oil prices and Energy stocks surged

Source: Charles Schwab, Bloomberg, as of 3/8/2022. Past performance is no guarantee of future results.

That has been consistent with strong performance in the S&P 500 Energy sector, which recently climbed to 30% above its 200-day moving average. Energy is currently the top-performing sector by a considerable margin.

While no other sector has come close to matching Energy’s gains this year, there has been consistent leadership among factors across several sectors. In fact, high-quality value factors, such as high earnings yield and high revenue relative to price, have been among the top performers this year within the Energy and Tech sectors. Despite the Energy sector having outperformed Tech by nearly 52% this year, factor leadership within both has looked almost identical, confirming that investors can find stability without having to make an all-out sector call.

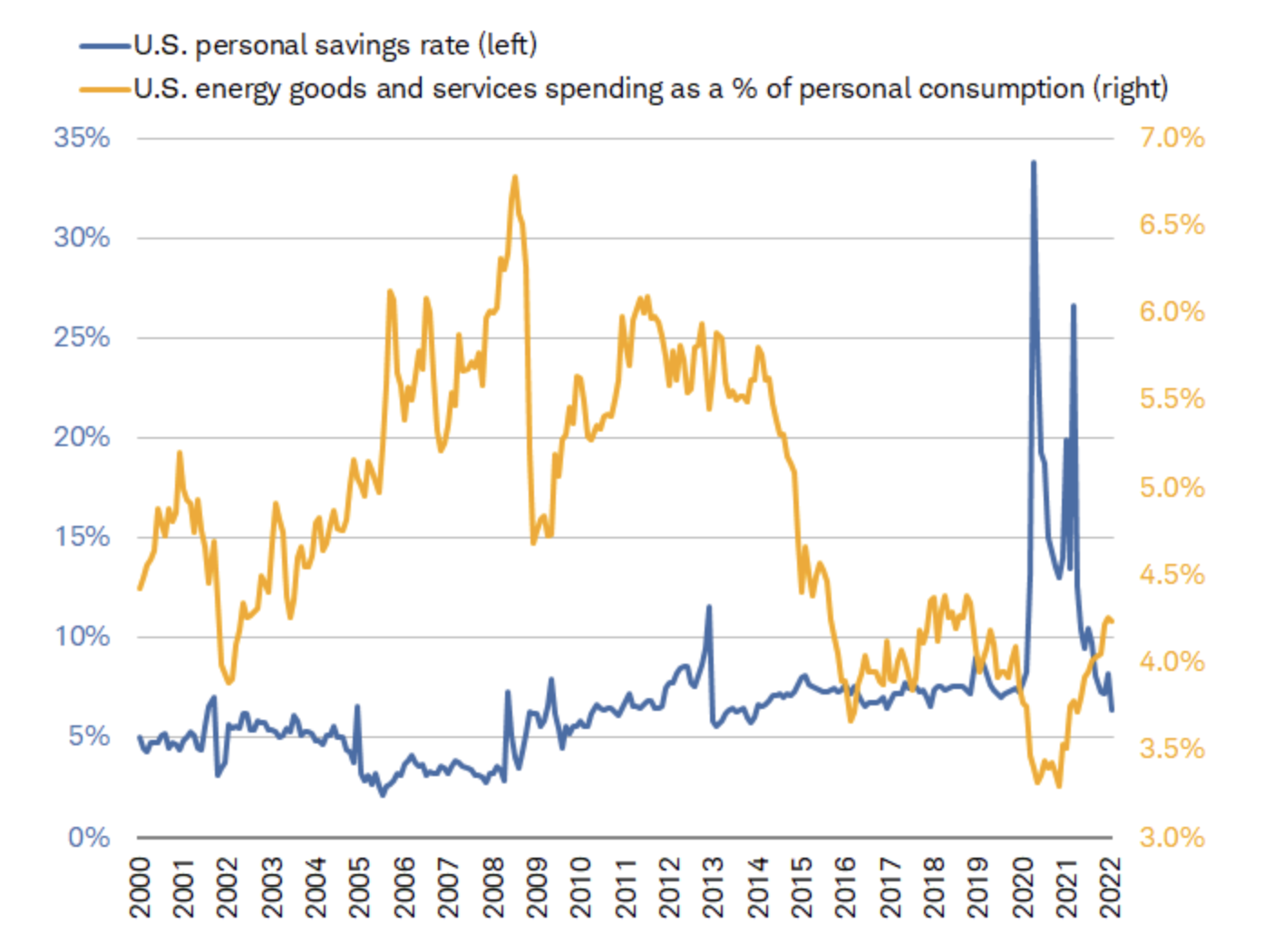

High energy prices in conjunction with high and rising inflation tend to dampen households’ spending power. Although energy spending makes up a smaller share of overall consumption relative to the Global Financial Crisis era, it still acts as a regressive tax on consumers (especially those on the lower end of the income and wealth spectrum).

In addition, as you can see in the chart below, the savings rate has plummeted from its pandemic peak and fallen to its lowest level since 2013. As such, households’ cushion against inflation is waning.

Pressure building from low savings

Source: Charles Schwab, Bloomberg, as of 1/31/2022.

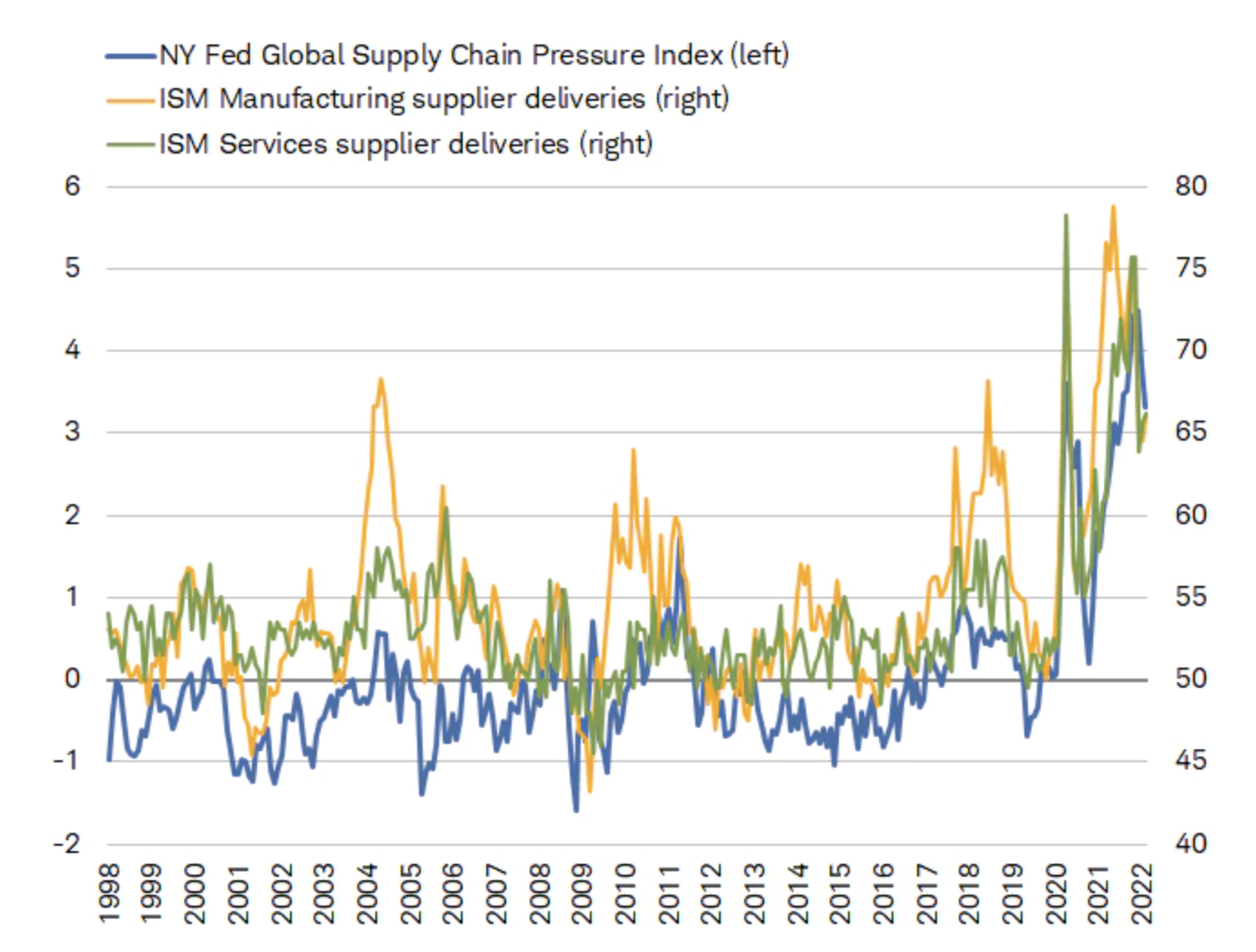

Looking ahead, there is some good news on the inflation front. Excluding the surge in energy prices, there are signs of thawing in other areas. Supply chain pressures, which helped drive prices to multi-decade highs, look to be easing. As you can see in the chart below, the New York Fed’s Global Supply Chain Pressure Index has fallen sharply from its recent peak. While that has been accompanied by a slight increase in the supplier deliveries components of both U.S. ISM purchasing manager indexes, both are well off their pandemic peaks.

Thawing of frozen supply chains

Source: Charles Schwab, Bloomberg, as of 2/28/2022. The New York Fed’s Global Supply Chain Pressure Index integrates a number of commonly used metrics with an aim to provide a more comprehensive summary of potential disruptions affecting global supply chains. The index is normalized such that a zero indicates that the index is at its average value with positive values representing how many standard deviations the index is above the average value. ISM supplier deliveries levels above 50 indicate delivery times are lengthening; levels below 50 indicate delivery times are shortening.

The inflationary stresses that have plagued the economy may continue to be exacerbated by the current energy shock, but the improvement under the surface and among several supply segments supports the prospect for a slowing inflation rate throughout the year. In addition, a continued surge in energy and food prices—which would keep headline inflation elevated—would likely put more significant downward pressure on demand for most other components of traditional inflation indexes.

Washington: Ukraine aid drives government funding compromise

On March 9, Congress unveiled the long-stalled government funding bill, which includes a $13.6 billion package of humanitarian and military aid for Ukraine. The 2,741-page bill outlines funding for every federal agency and program for the remainder of Fiscal Year 2022, which runs through September 30. The massive bill faced a deadline of March 11 in order to avert a government shutdown. Congress has avoided a shutdown to date by passing a series of short-term extensions of government funding since the beginning of the fiscal year on October 1, 2021, as lawmakers struggled to reach a compromise on the 12 appropriations bills that must be passed annually to fund government operations. But bipartisan support for getting aid to Ukraine as quickly as possible was critical in breaking the logjam on Capitol Hill over the government spending agreement. Votes are expected in both the House and Senate later this week. Both the House and Senate approved the bill on March 10.

Kevin Gordon, Senior Investment Research Specialist, and Michael Townsend, Managing Director of Legislative and Regulatory Affairs, contributed to this report.

© Charles Schwab

Read more commentaries by Charles Schwab