Stock prices and bond yields have been moving in opposite directions this year. It is possible that bond yields may soon level off after the rapid climb in the 10-year U.S. Treasury yield to near 3% from 1.5% at the start of 2022. Yet, stock market investors may still desire ways to hedge against the risk of any further rise.

Short duration stocks

In the bond market, favoring shorter duration bonds may provide some protection against rising rates. Likewise, in the stock market, short duration stocks may provide a hedge against rising yields. The duration of a stock is defined as the average time until its cash flows are received, weighted by their present values. In other words, when markets pursue a theme driven primarily by rising interest rates, it tends to favor stocks with more immediate cash flows (shorter duration) and punish stocks that are expected to deliver a higher proportion of cash flows in the distant future (long duration).

Unlike bonds, which are debts with regular payment schedules, stocks represent ownership of the company and cash flows can be irregular and not guaranteed. To measure duration for stocks we use the price to cash flow ratio. By ranking the stocks in the MSCI World Index by this ratio, we can see that short duration stocks (the 20% of stocks with the lowest price to cash flow) continued to outperform the overall market and their long duration counterparts (20% of stocks with the highest price to cash flow) in April, as they have done since interest rates began to rise in August 2020.

Short duration stocks outperforming long duration stocks

High price to cash flow = top 20% of stocks ranked by price to cash flow in MSCI World Index. Low price to cash flow = bottom 20% of stocks ranked by price to cash flow in MSCI World Index.

Source: Charles Schwab, FactSet data as of 4/20/2022. Past performance is no guarantee of future returns.

Falling rates pose a risk

Short duration stocks dramatically outperformed both long duration stocks and the overall MSCI World Index when bond yields climbed from their low in August 2020. However, short duration stocks lagged the overall index and their long duration peers when yields retreated slightly (from April through December of 2021), highlighting a risk to this theme.

Cumulative performance of short and long duration stocks since yields bottomed

Source: Charles Schwab, FactSet data as of 4/20/2022. Past performance is no guarantee of future returns.

10-year Treasury yield

Source: Charles Schwab, FactSet data as of 4/20/2022. Past performance is no guarantee of future returns.

Finding potential opportunities

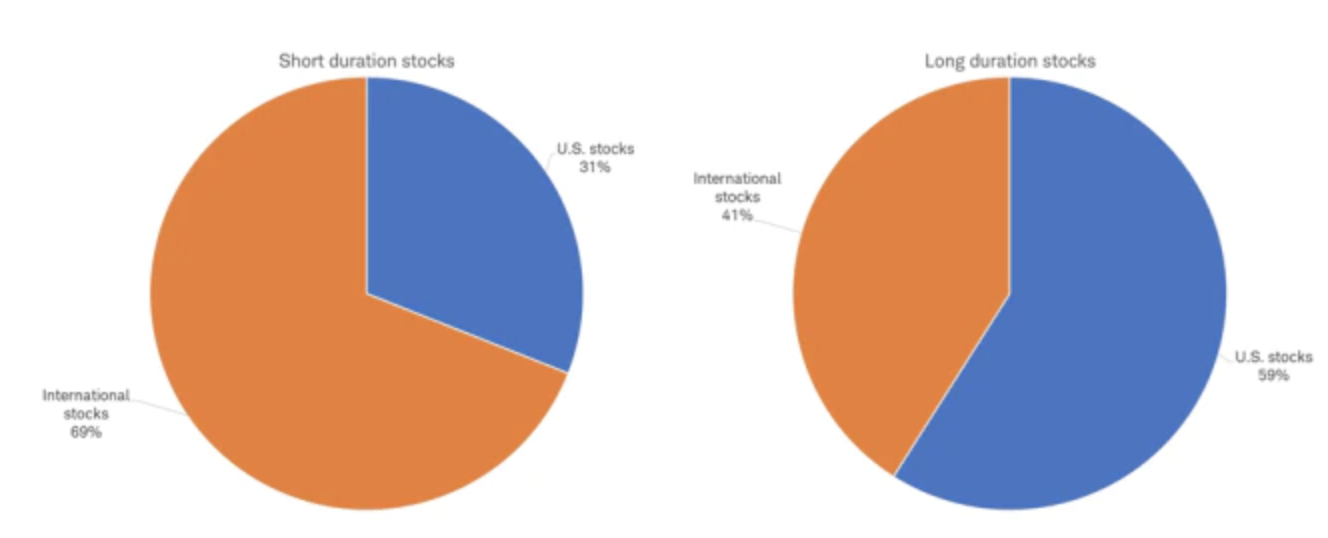

Low price to cash flow stocks can be found in all sectors and countries. But they tend to be more concentrated in the indexes of international markets. Although 39% of the 1,539 stocks in the MSCI World Index are U.S.-based companies, U.S. stocks make up 59% of long duration stocks and only 31% of short duration stocks. The remaining short duration stocks (69%) are international companies.

Short duration stocks are more prevalent internationally

Based on stocks in MSCI World Index. Source: Charles Schwab, FactSet data as of 4/20/2022.

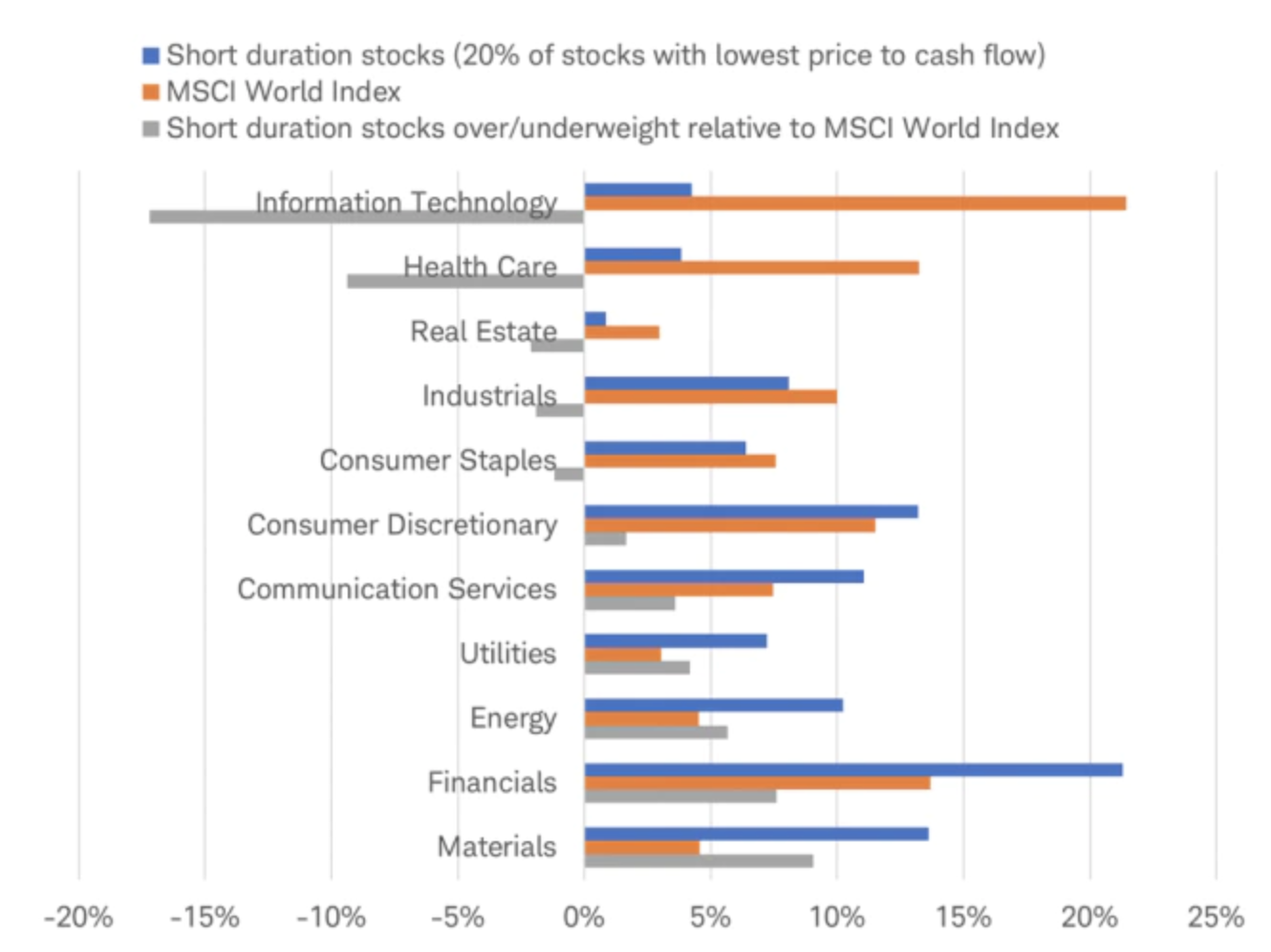

Balancing sector exposure

When using a filter, like low price to cash flow, to find stocks that may fare better in an environment of rising interest rates, it is also important to consider diversification across sectors. An equal-weighted portfolio only consisting of the 20% of stocks with the lowest price to cash flow contains stocks from all sectors, but would lead to sizable underweights in information technology and health care, with overweights in materials and financials, relative to the MSCI World Index.

Percentage of stocks by sector

Source: Charles Schwab, FactSet data as of 4/20/2022.

Reflecting on potential opportunity

Ultimately, there can be no guarantees as to where interest rates are headed. For investors considering hedging some of the risk of higher interest rates in their stock portfolios, the mindful addition of short duration stocks may be an effective way to manage risk while remaining invested in the markets.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.