Introduction

We strongly believe that the traditional benchmark-led approach to investing in emerging market debt can be far from optimal. There are two major flaws in being overly wedded to an off -the-shelf benchmark:

1. There are embedded characteristics, or betas, that may not necessarily be desirable. In particular, there is significant USD duration exposure associated with a hard currency1 strategy, typically managed relative to the EMBIG-D,2 while EMFX exposure is a major component of a local currency strategy, typically managed relative to the GBI-EMGD.3 It is often the case that an investor already has plenty of USD duration from other bond portfolios and EMFX exposure from emerging market equities, yet simply accepts these characteristics as part of an emerging debt investment because they are embedded in the benchmark. (A blended benchmark is somewhere “in between” from a beta standpoint, with lower durations than EMBIG-D, and EMFX exposure determined by the extent of GBIEMGD’s presence in the blended benchmark.)

2. If a manager’s opportunity set is constrained by their benchmark, potential alpha opportunities may be de-emphasized, or even ignored completely. For example, there can be limits on the amount of “off benchmark” holdings and exposures that a manager may take relative to their EMBIG-D, GBI-EMGD, or CEMBIB-D4 benchmark, regardless of how similar such exposures may be in practice relative to his stated benchmark. In theory, blended benchmarks relax this constraint, expanding alpha opportunities.5

We are increasingly having conversations with clients that are seeking to unlock the exciting return opportunities in emerging debt while being much more discerning about embedded betas. A single benchmark, or indeed a blend of benchmarks, can be determined to allow for whatever USD duration and EMFX exposure best suits the investor’s overall objective. Lately, with more emerging countries entering debt distress and/or default, the “quality” axis is also a topic of interest, with some clients preferring the stability of higher-quality credits, and others interested in leveraging our considerable skill in sovereign debt workouts among distressed/defaulted issuers (some of which are “frontier” markets). To us, these are the “big” asset allocation levers, although blended benchmarks are not the only way to achieve them given how trivial it is to target duration, USD/EMFX exposure, and/or quality in any setting. An obvious extension is to remove the beta associated with emerging debt benchmarks completely, and freely use the full combination of alpha sources to target a total return over cash. Indeed, whatever overarching objective is set, the ability to use all alpha sources coupled with a liberal approach to tracking error should ensure the best outcome. We already use this approach in the management of our existing long-only strategies.

As a manager with nearly 30 years managing a global emerging debt opportunity set, GMO is very well equipped to create variations across the spectrum from singlebenchmark, through blended-benchmark, and right across to total return solutions. Our skills are deep in sovereign and quasi-sovereign credit (in hard and local currency); as well as in managing local currency and interest rate exposures. In terms of expected return, a typical target would be 150-200 bps of net alpha relative to standard benchmarks, including blended ones, or cash + 7-9% for total return solutions.

Total Return – Arriving at Cash + 7-9%

GMO has a long and successful track record in alpha generation, ranking top eVestment quartile in each of its hard and local currency strategies over all relevant time periods as of 12/31/2021. A distinguishing feature of GMO’s approach is our alpha emphasis on bottom-up (“in country”) instrument selection over top-down exposures to countries, currencies, or duration, as well as a strong preference for relative value over timing (although one exception to this is our view of the credit spreads versus expected defaults). This alpha approach makes us well suited for total return applications.

In order to target a return of cash + 7-9%, we use a mix of credit (typically partially hedged), EMFX, and rates.

POTENTIAL EXCESS RETURN OF AROUND 4-6% FROM SOVEREIGN AND QUASI-SOVEREIGN CREDIT (TYPICALLY PARTIALLY HEDGED)

GMO is known for its extensive experience managing all aspects of sovereign credit, including performing, stressed, distressed, and defaulted issues. We are pioneers in this space, and regularly recognized as such. Within sovereign credit, the universe is broad both by country and by currency, including hard and the local currency of each country.6 More importantly, though, the universe is also broad by instrument type, including bonds, loans, credit derivatives, and project fi nance, among others.

Similarly, for quasi-sovereign investments, a dedicated team scours the entire investment universe for opportunities to add alpha relative to sovereign-only exposures. Under our broadest definition of quasi sovereigns, our universe covers more than half of the market cap of the CEMBIB-D, as state-owned entities feature prominently in emerging markets.7 Of the remaining “pure corporates” in the CEMBIB-D index, few have offered alpha potential for our portfolios, and some have proved interesting only after they have defaulted out of CEMBIB-D.8 In all cases, we carefully examine the documentation to understand our rights in adverse outcomes.

Of course, this return generated from credit spreads is a combination of alpha and beta – the credit spreads are, after all, embedded in benchmarks. It is worth noting that this EM credit spread beta is unique to – and possibly even the core essence of – the asset class, unlike the beta exposure to USD duration or EMFX that are also captured by benchmark. Given the nature of the issuers, hedging the credit risk can be non-trivial and mostly unadvisable. In most time periods credit spreads exceed expected losses, and our Quarterly Emerging Market Debt Update keeps track of this time-varying “credit cushion.” Thus, any hedging of credit risk focuses on limiting permanent losses from defaults rather than limiting mark-to-market volatility.

The shift from long-only benchmark-relative investing to total return, then, is twofold: 1) reducing the USD duration toward zero and 2) translating over/underweight benchmark-relative positions to leveraged long/short ones.

Because we do partially hedge credit risk, and also because the long/short nature off ers some protection against systemic credit risk, one could typically expect a residual credit beta to EMBIG-D in the region 0.2-0.8 depending on the view of the risk and reward trade-off .

POTENTIAL EXCESS RETURN OF AROUND 2% FROM CROSSSECTIONAL DURATION POSITIONING

Our current local rates process boasts a forecasted information ratio (IR) above 1.0, using a wide universe of interest rate markets encompassing two sub universes of high-quality markets and more idiosyncratic (typically higher-yielding) markets. The bulk of process alpha comes from cross-market positioning rather than overall duration timing. It is currently applied as an overlay to our GBI-EMGD-relative local debt strategy as well as providing select receiver and payer positions for our hard currency strategy. In a total return solution, we would expect to run this at roughly two times the exposures of the overlay in our local debt strategy. Although the IR of the strategy is high, rather than levering to a tracking error, we believe individual country duration contribution limits are a more prudent portfolio construction technique. After all, we still get occasional bolts-from-the-blue in emerging markets, most recently in Russia. Notably, the program is fl exible, allowing a country to shift from the quality universe to the idiosyncratic one as events unfold.

POTENTIAL EXCESS RETURN OF AROUND 1% FROM CROSSSECTIONAL EM CURRENCY POSITIONING

Our EMFX alpha strategy has a forecasted IR of close to 1.0, also using a wide universe of currency markets. Analogous to rates, these exposures are applied as an overlay to our local currency GBI-EMGD relative strategy, and select exposures are applied to our hard currency strategy. It is mostly U.S. dollar neutral, with small dollar timing. It is fully portable to total return solutions. In addition, we monitor a universe of 22 pegged, mostly frontier currencies for additional opportunities, some of which are unfunded (via non-deliverable FX forwards). Others require capital (FX-denominated, AAA-rated multilateral issues, for example). In these cases, the cost of capital is examined relative to alternatives coming from other holdings, such as sovereign credit.

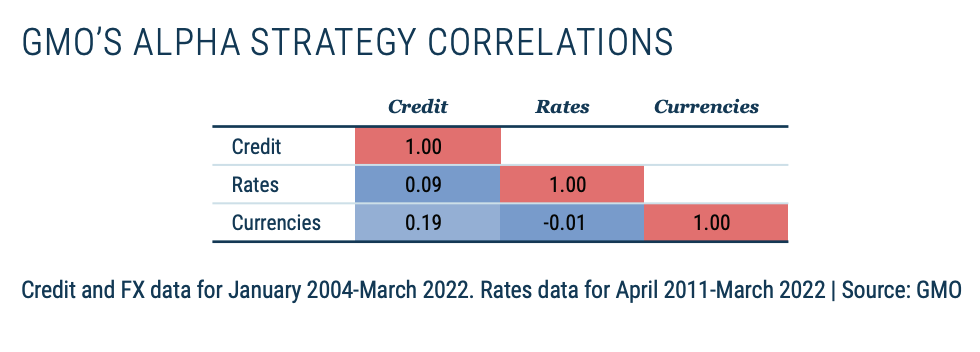

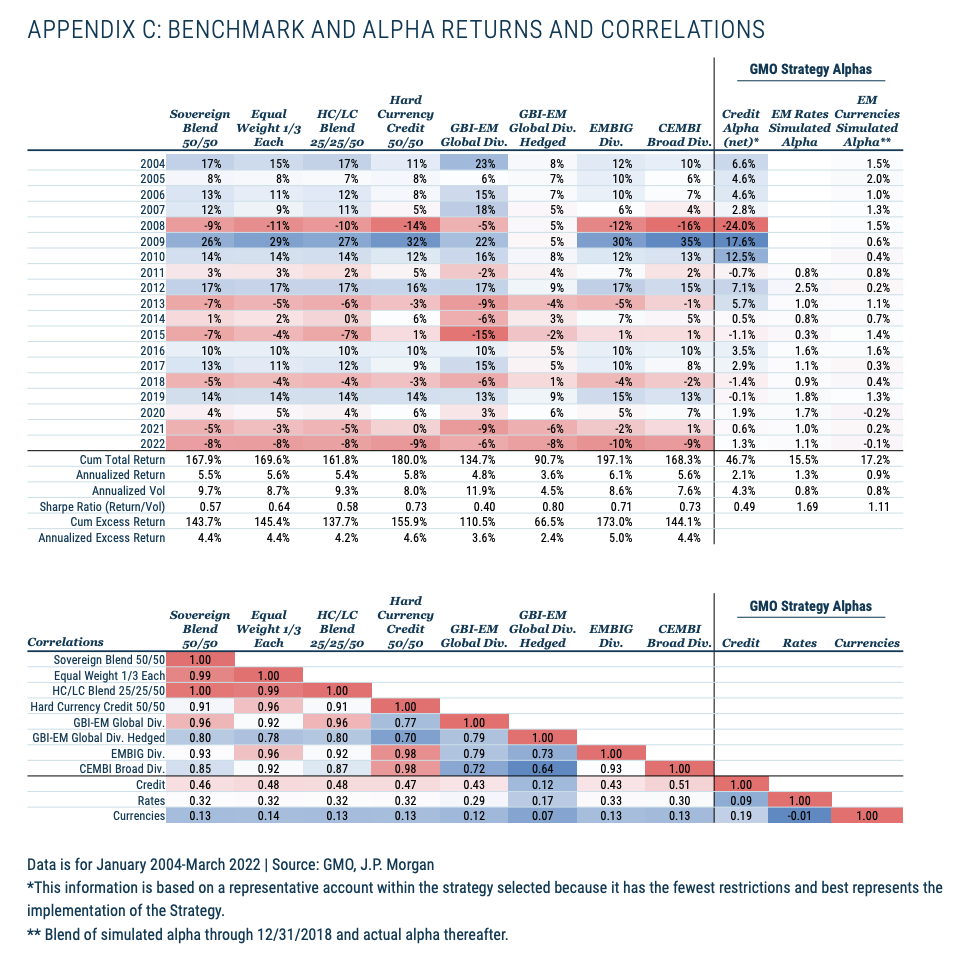

RETURN SOURCES IN COMBINATION In addition to our high confidence in each of the individual sources of return (gained through the team’s nearly 30 years of experience achieving market-leading results), we believe the real strength is to be found in their combination. The correlation profile is quite desirable among the strategies:

GMO’s Approach to Blended (Long Only) – Alpha and Asset Allocation Implications

GMO’S ALPHAS ARE RELEVANT IN ANY BLENDED LONG-ONLY SETTING, LEAVING ASSET ALLOCATION CONSIDERATIONS TO DRIVE BLEND CHOICE

We’ve long said that we pursue a blended opportunity set regardless of the benchmark, concerned only with adding alpha relative to a benchmark with known asset allocation properties (i.e., duration, FX, quality). Our hard currency and local currency strategies routinely buy bonds from the “other” benchmark, hedging FX and/or rates exposures as appropriate. Both strategies buy quasi-sovereign and corporate bonds from EMBIG-D and CEMBIB-D. Therefore we’re benchmark agnostic from an alpha perspective, encouraging our investors to consider the big asset allocation questions when choosing their benchmark.

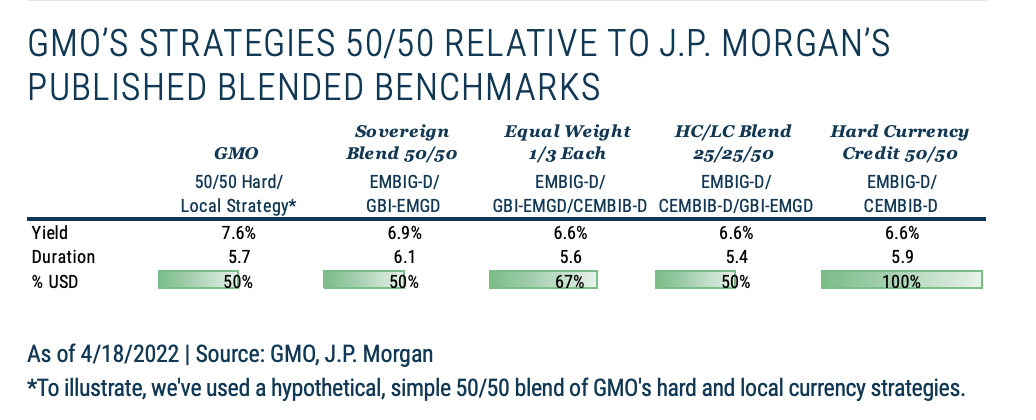

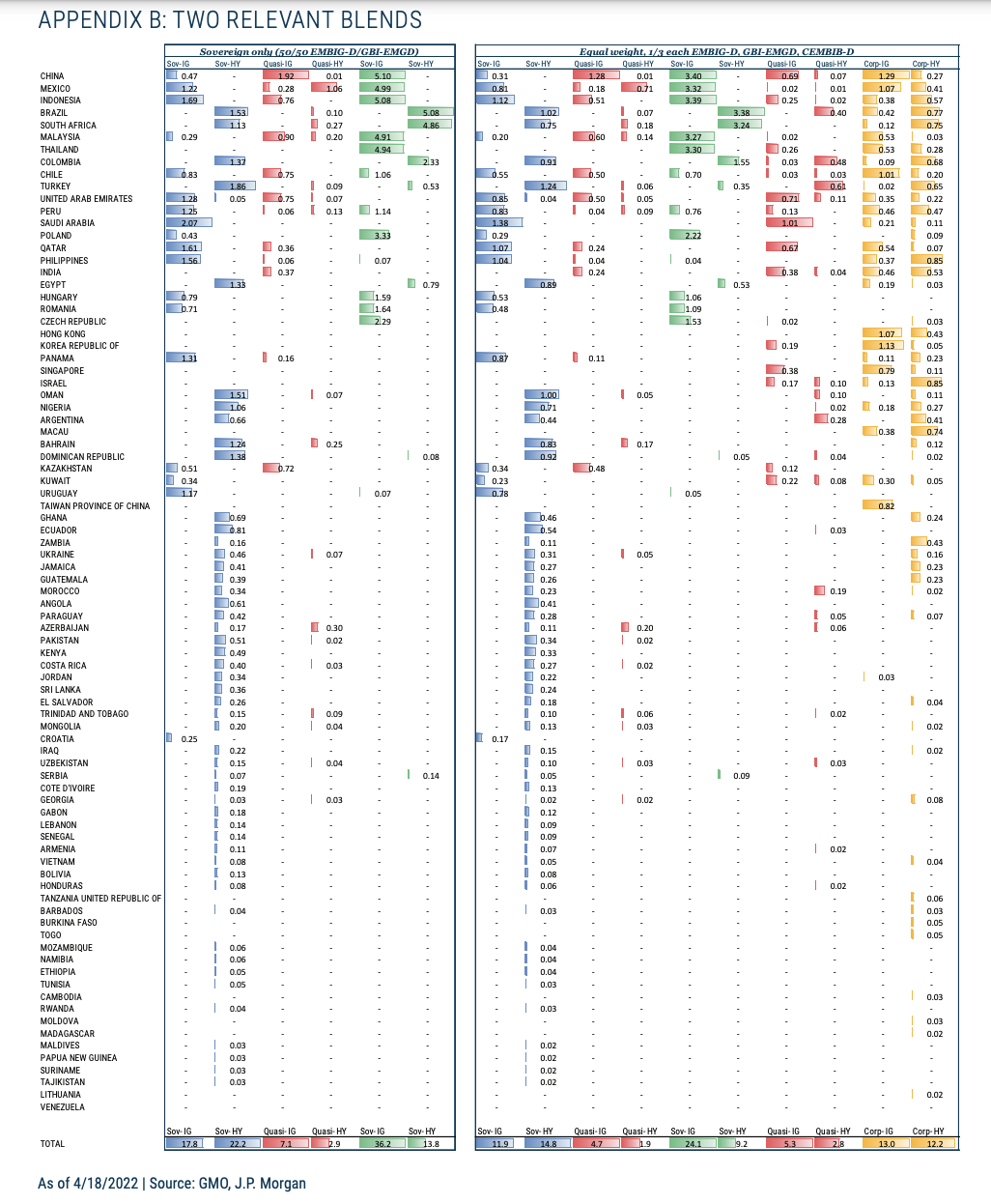

Combining in equal measure the exposures of our existing hard and local currency strategies, the table below shows that this blend looks similar to all the blends by duration,9 and the same as the “Sovereign Blend 50/50” and “HC/LC Blend 25/25/50” by USD vs. EMFX exposure (e.g. 50% USD, 50% EMFX). To us, these are the big asset allocation levers, although blending benchmarks is not the only way to achieve them given how trivial it is to target duration and USD/EMFX exposure in any setting.10

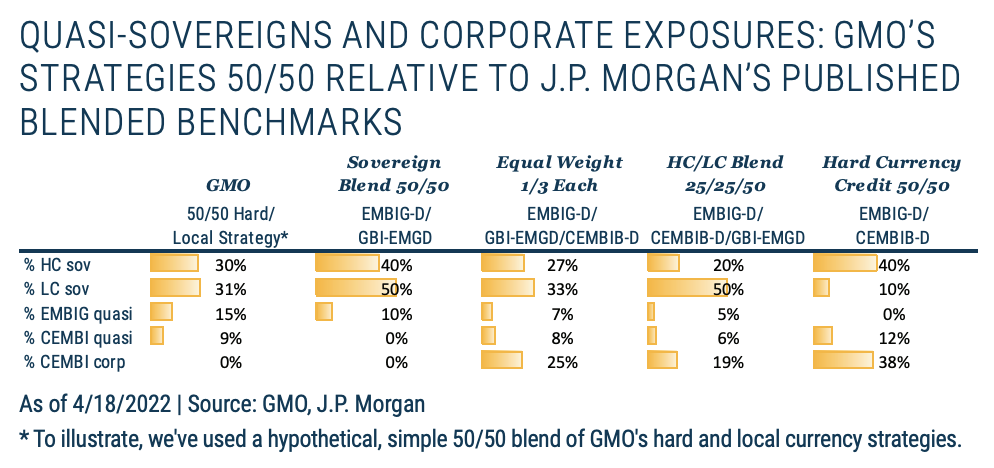

As for credit quality, note that the top countries have large weights in each benchmark, where the rank correlation of country weights is 95%+ across the individual and blended benchmarks. Therefore, all the blends end up fairly similar by country – and by credit rating distribution. The top 30 countries comprise 85-90% leaving the “tails” (discussed in the appendices) to drive much of the differences.

As for corporates, looking further under the hood of this 50/50 blend of GMO’s existing strategies, you will note that by sector we are currently overweight both EMBIG-D and CEMBIB-D quasi sovereigns which, in total, is closer to the “Equal Weight 1/3 Each” blend given a total non-sovereign weight of nearly 30%.11 If it adds alpha and comes from CEMBIB-D, we will buy it. This shows how liberally we use the opportunity set given within our existing strategies, allocating to CEMBIB-D issues when, and only when, they are attractive. Thus, although we haven’t off ered a stand-alone CEMBIB-D product, we are well equipped to select individual securities from CEMBIB-D and therefore to be measured against blends that include CEMBIB-D.

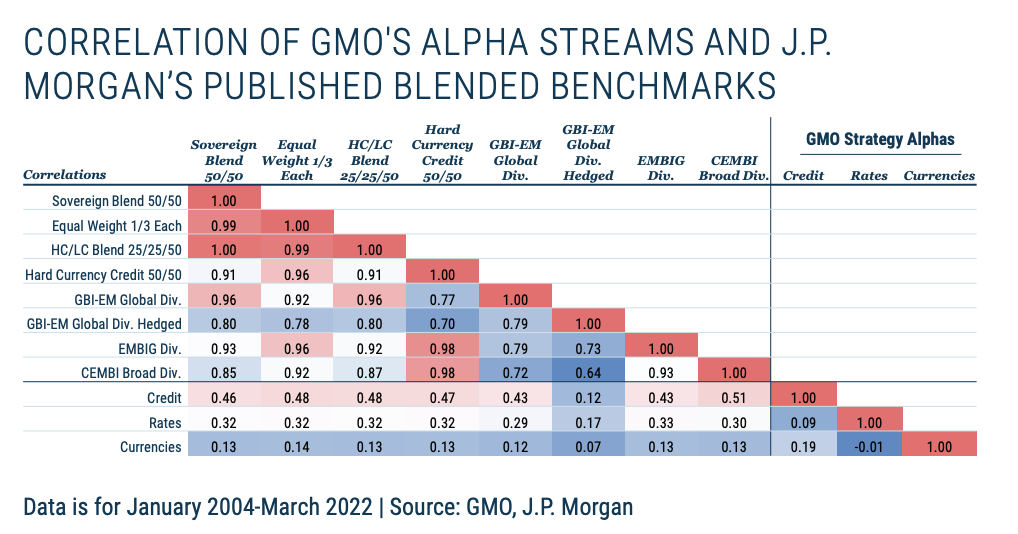

Importantly, when thinking about total return, consider the implications of hiring GMO as a blended alpha manager by looking at the correlation of our alpha streams with the various long-only options. While generally sub-0.5, it is not surprising that the most positive correlation is the credit alpha given our statement that credit spread might be considered to be a mixture of alpha and beta, whereas rates and FX alphas are more diversifying.

Conclusion

As an alpha manager with a global opportunity set, GMO is well equipped to create variations across the spectrum from single-benchmark, through blended-benchmark, and right across to total return solutions. Our skills are deep in sovereign and quasisovereign credit (in hard and local currency); as well as in managing local currency and interest rate exposures. With U.S. interest rates rising and the USD continuing to pose challenges to holding long-only EMFX exposure, now could be the appropriate time to consider a new approach to emerging debt investment. A total return solution can eliminate systemic exposure to U.S. duration and EMFX, while a blended solution can be tailored to capture only the amount of those beta exposures that is considered desirable. In terms of potential return, a typical target would be 150-200 bps of net alpha relative to standard benchmarks, including blended ones, or cash + 7-9% for total return solutions.

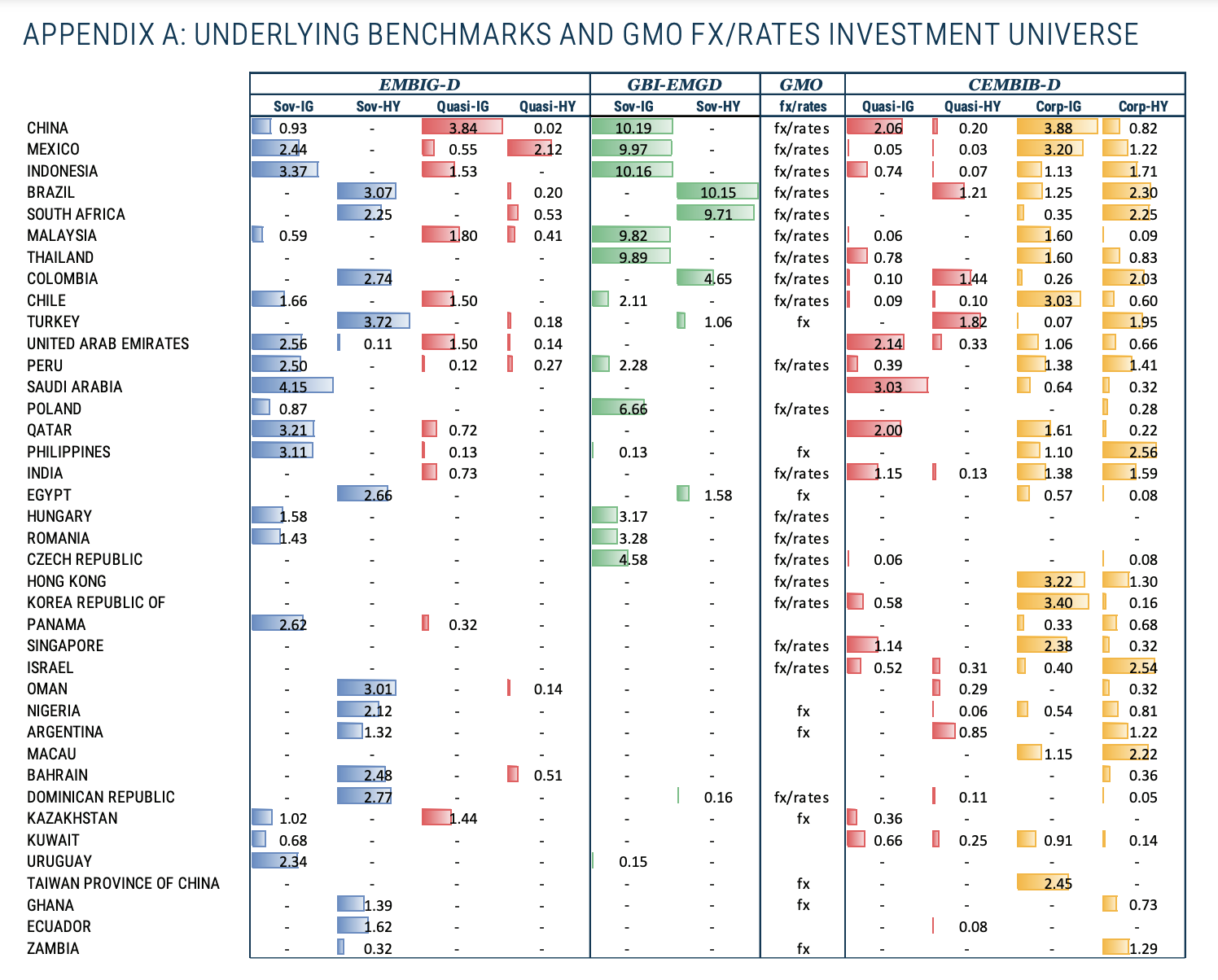

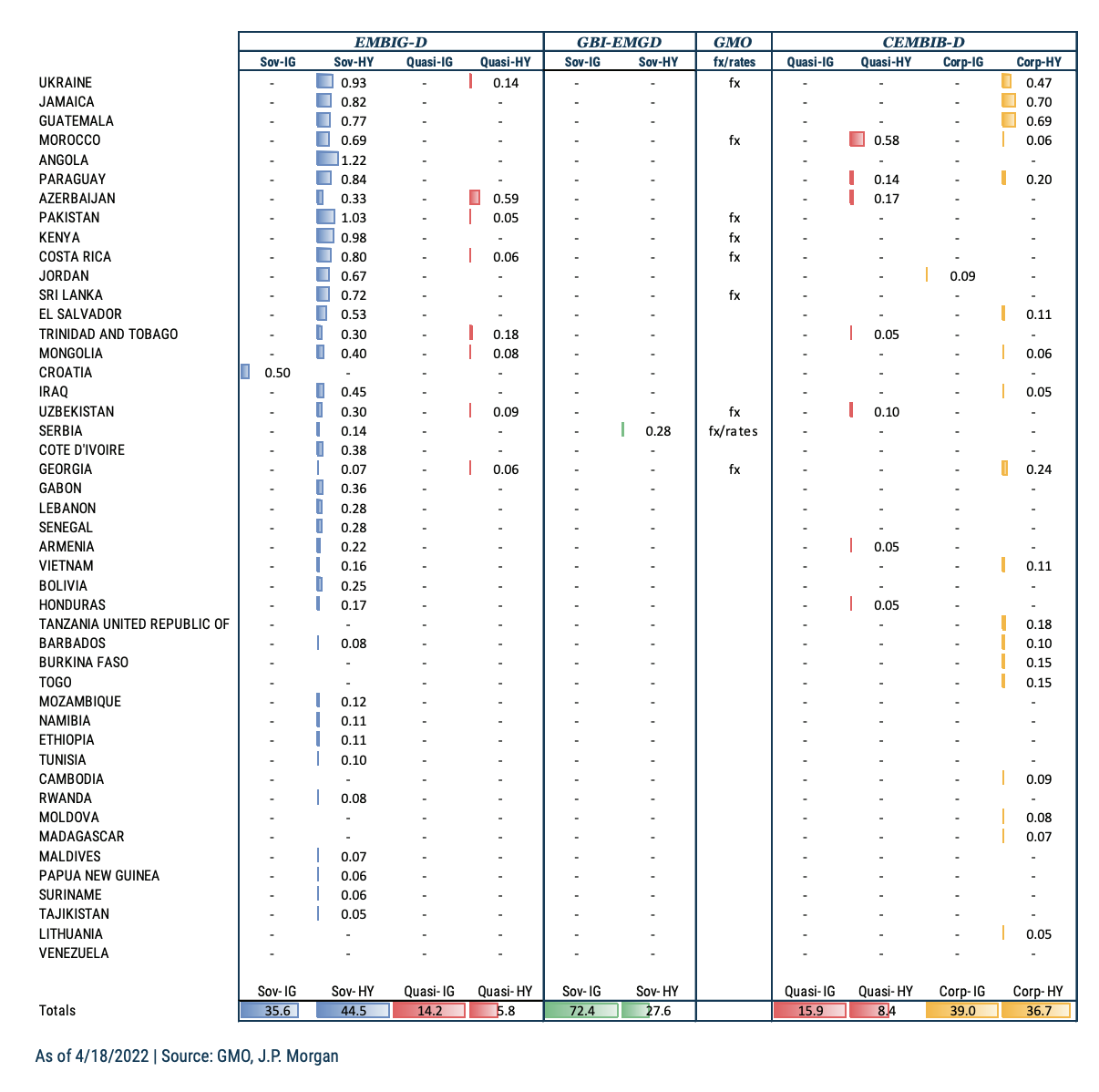

A Note on Appendices A and B

The Appendices A and B show the investment universe in more detail. Appendix A shows the underlying benchmarks and is organized in descending order of country weight using the Equal Weight blend. Within each index (EMBIG-D, GBI-EMGD, and CEMBIB-D), we show the contribution to weight coming from the major credit types: hard currency and local currency sovereigns, quasi-sovereigns, and corporates. Each of these is then broken into investment grade and sub investment grade (i.e., high yield) to give a sense of what’s contributing to the yields and durations.

In the main text we referenced the fact that the top countries overlap across the three major benchmarks and that EMBIG-D and CEMBIB-D each has a “tail” of non-overlapping exposures.

In credit: for EMBIG-D, the tail is mostly smaller, sub investment grade countries. For CEMBIB-D, the tail is mostly Taiwan (too high income for EMBIG-D/GBI-EMGD) plus a variety of high yield corporates. GBI-EMGD essentially has no credit tail given that it has no unique countries.

In rates & FX: While GBI-EMGD doesn’t contribute to country diversity, it does contribute to rates and duration diversity. That said, GMO’s rates and investment universe extends well beyond these 20 markets to include high-quality markets as well as an extensive list of frontier markets.

© GMO

Read more commentaries by GMO