Like the proverbial middle child, mid-cap stocks often go unnoticed between their large-cap and small-cap siblings. But investors seeking exposure to value equities should take a closer look; mid-caps offer a less-travelled route to stronger return potential with relatively moderate risk.

During a difficult first half for equity investors, value stocks outperformed. The Russell 1000 Value Index of large-cap stocks fell by 12.9%, outperforming the S&P 500 by 7.1%. After several challenging years for value equities, the relatively resilient performance drew attention from investors who have been underweight value stocks—or lacked exposure entirely.

Why Have Value Stocks Outperformed?

And with good reason. Value stocks typically do relatively well when interest rates rise, which increases the discount rate used to value the future cash flows of stocks. While this tends to compress valuation multiples of all stocks, growth stocks are particularly vulnerable and value stocks are generally more resilient.

But value stocks are also widely perceived as being riskier. So, some investors might have qualms about dipping a toe into the value waters at a time when equity markets have been very volatile and companies are facing uncertainty on many fronts. Value companies trade at low price/earnings valuations, often because of a controversy that has raised doubts about the sustainability of their business or earnings potential.

In this environment, large-cap value stocks might be appealing to some because they tend to be higher-profile companies with perceived lower risk. Small-cap value stocks offer stronger return potential but may be more vulnerable to volatility. Indeed, small-cap stocks sold off sharply versus their larger-cap peers over the past four years as investor anxiety about the global economy intensified. Both large- and small-caps have pros and cons, with the suitability depending on an investor’s risk appetite and broader allocation profile.

Bridging the Risk-Return Gap

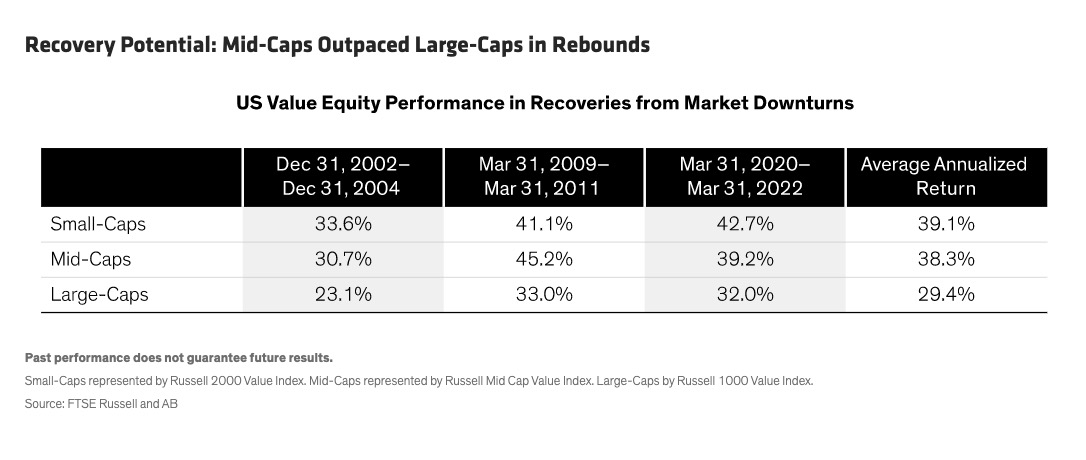

Mid-cap stocks can provide a good bridge between the two. During prior market recoveries, smaller-cap value stocks have outpaced larger-cap peers in the two years after a market bottom (Display). Mid-cap stocks have enjoyed similar recovery rates as small-caps.

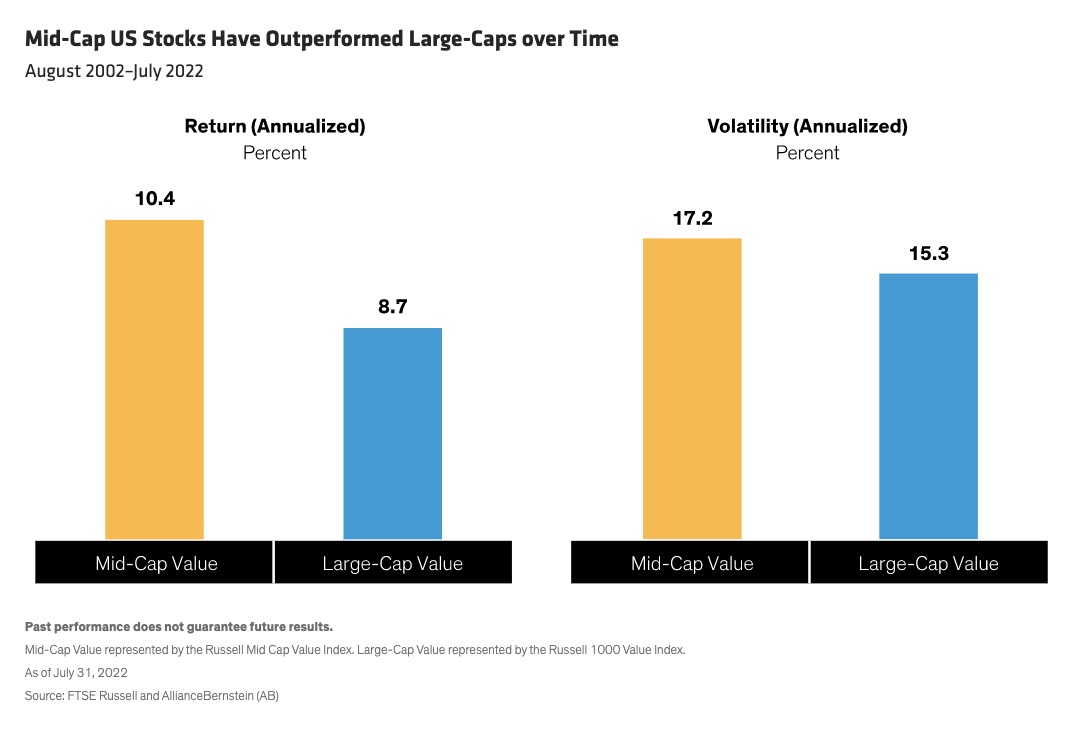

Over longer periods, these strong recoveries and have given mid-cap value stocks superior returns to larger-caps but with only a modest increase in risk (Display).

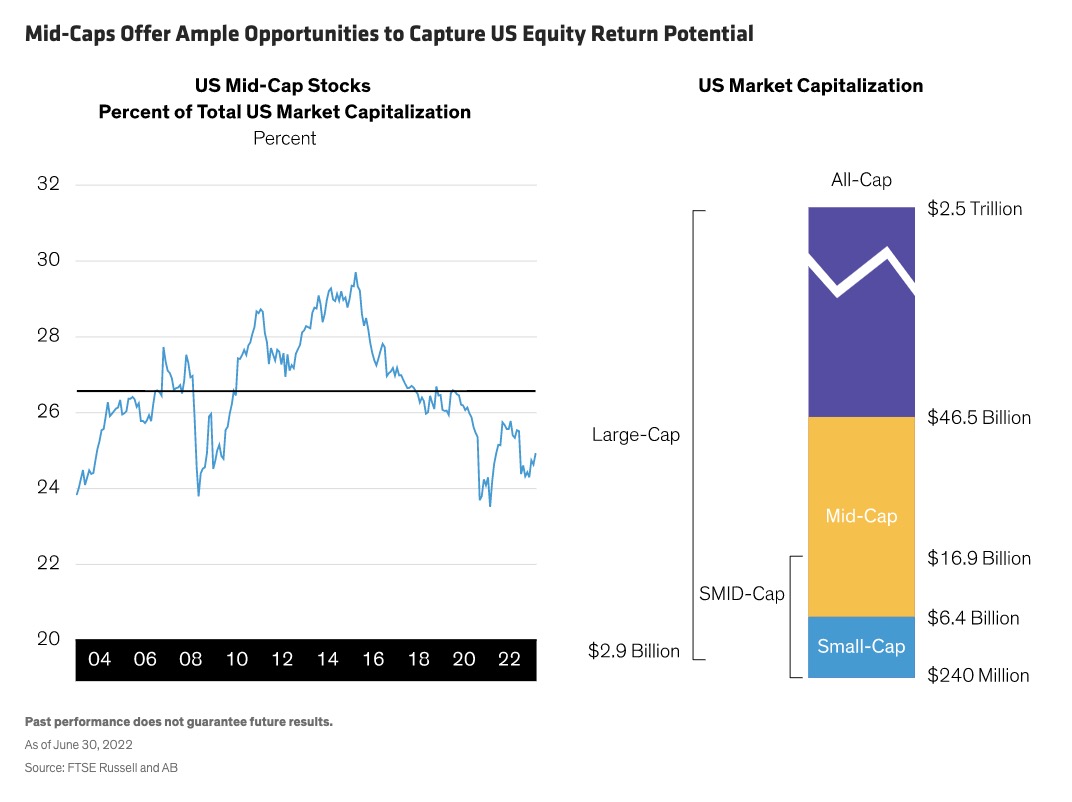

To capture that return potential, an active approach can be particularly effective, in our view. Mid-caps account for about a quarter of total US market capitalization (Display). Yet mid-cap stocks have relatively low weights in US large-cap indices, so they tend to get relatively less attention from large-cap portfolio managers. And within the $6 billion to $40 billion market cap segment that mid-caps generally call home, there are more than 500 companies to choose from, providing ample breadth to discover hidden opportunities and diversify by sector and industry.

Identifying mid-cap value opportunities requires the same disciplined approach that is applicable to larger- and smaller-cap stocks. Value investors seek stocks that are facing uncertainty about the sustainability and value of a company’s cash flows. The challenge is to correctly identify which have been unfairly punished and can eventually show strong and sustainable cash flows, and then determine when to get in position.

Compelling Catalysts for a Company’s Revival

Companies with a combination of strong fundamentals and compelling catalysts spell opportunity. Attractive valuations are only part of the value story—it’s just as important to understand a company’s competitive landscape, business environment and management capabilities. Then, investors should identify a catalyst such as a management change, stock buyback or other improvements that can drive a reassessment of the company’s valuation to push the stock up.

Examples today can be found across sectors and industries. For example, ON Semiconductor, based in Phoenix, is taking steps to improve profitability. The technology company is acquiring an underutilized semiconductor fabrication facility in the US while changing the types of products it makes and the end markets it serves. This allows ON Semiconductor to shift away from more commoditized products toward more profitable and higher value-added industrial and automotive applications. New agreements to produce silicon carbide semiconductors, a critical component in electric vehicles, provide access to a fast-growing market.

In financials, First Citizens Bancshares is a North Carolina mid-cap bank that recently completed an acquisition of CIT, a bank and equipment finance company. The deal unlocks significant potential synergies as First Citizens can use its stable and low-cost deposit base to improve the funding cost for the CIT portfolio. Cost savings are also expected through the elimination of redundant support functions and generate strong revenue growth through cross marketing.

The healthcare sector also offers mid-cap opportunities. Centene, based in St. Louis, is a managed care organization that recently underwent a leadership change after the company’s founder passed away. The new management team includes experienced professionals who can help consolidate the company’s positions as a leader in the fast-growing Medicaid and Health Exchanges insurance markets. Efforts are also underway to increase margins through cost cutting while improving Centene’s quality metrics, which can help push up payment rates.

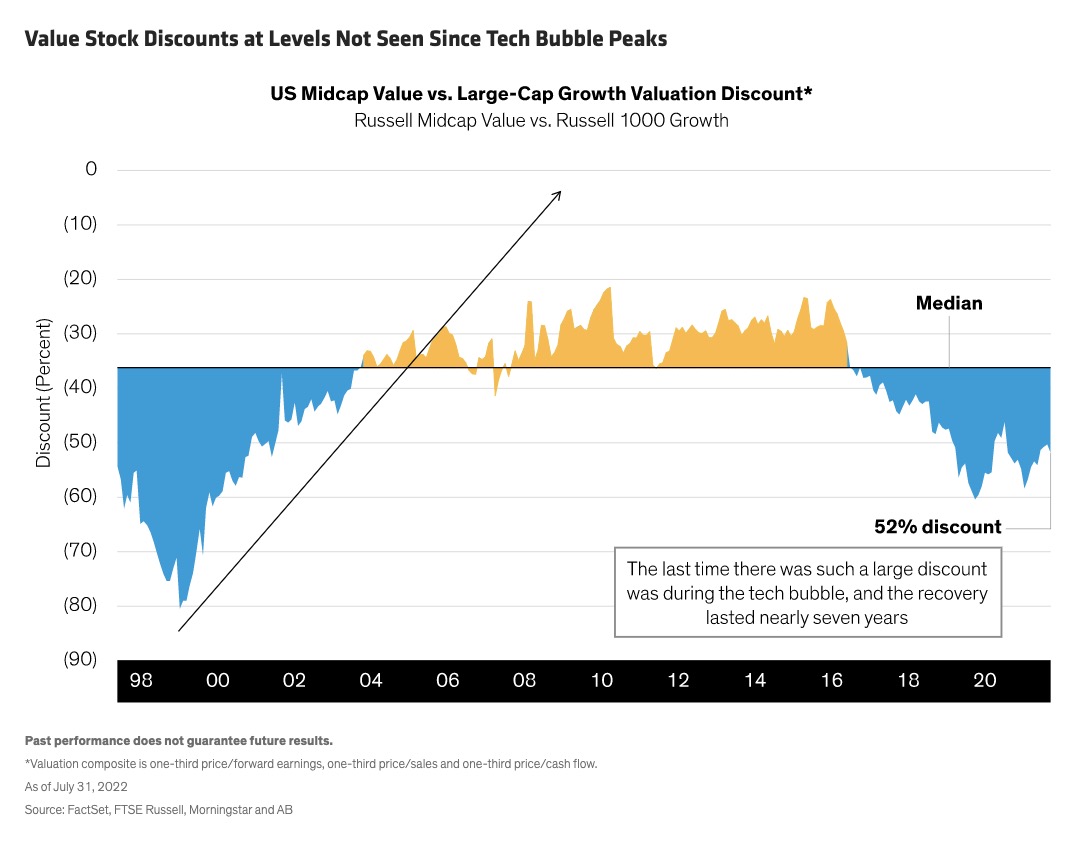

Mid-Caps Trade at Deep Discounts

Valuations are especially attractive in today’s uncertain market. Mid-cap value stocks traded at a 52% discount to large-cap growth stocks at the end of July (Display). The last time there was such a large discount was during the dotcom bubble in 2000, and the subsequent value recovery ran for nearly seven years.

Nobody can say with certainty whether the next few years will see a similar recovery. To be sure, today’s market environment is fraught with risks that are quite different than those seen 20 years ago. Investors today are acutely focused on understanding how company profits will be affected by supply chain snags, geopolitical tensions, inflation and macroeconomic uncertainty.

That’s why it’s important to make sure that value stocks are backed by quality businesses with strong fundamentals and sturdy balance sheets. At the attractive valuations we’re seeing today, we believe the less-known and underappreciated companies in the mid-cap universe can help bolster investors’ confidence to make value stocks part of a diverse equity allocation.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

References to specific securities are presented to illustrate the application of our investment philosophy only and are not to be considered recommendations by AB. The specific securities identified and described do not represent all of the securities purchased, sold or recommended for the portfolio, and it should not be assumed that investments in the securities identified were or will be profitable.

© AllianceBernstein

Read more commentaries by AllianceBernstein