China’s State-Owned Enterprises Hold Keys to Carbon Neutrality

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsESG in Action

China has pledged to reach carbon neutrality by 2060, and state-owned enterprises (SOEs) are responsible for half the country’s CO2 emissions. Yet SOEs are also major players in China’s renewable and other low-carbon energy industries. It’s important for investors to understand the ecosystem in which SOEs operate to gain insight on the macro and microeconomic challenges that will determine whether China’s long-term carbon-neutrality plans are successful.

China’s state-owned enterprises (SOEs) are huge CO2 emitters. But they’re also an essential component of efforts to reduce greenhouse gases in the world’s biggest emitter and second-largest economy. Investors must understand the role of SOEs in the economy and what drives these companies to gain insight into opportunities being created by China’s carbon-neutrality plans.

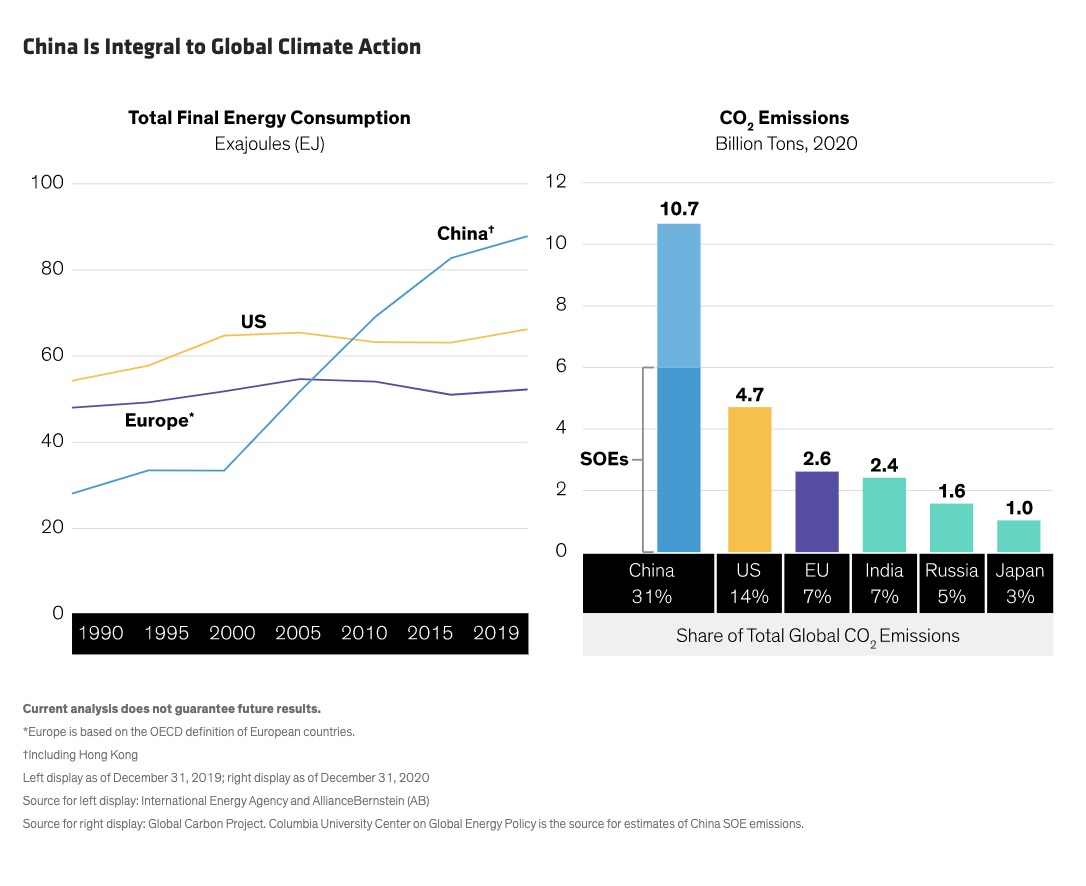

Global efforts to combat climate change won’t be successful without China. Throughout the 21st century, China’s rapid economic development has fueled a steady rise in energy consumption, in contrast to the US and European Union, where it has plateaued and even started to fall (Display). SOEs generated about six gigatons of CO2 per year, accounting for about half of China’s emissions—much more than all the emissions of the US or the EU.

Deciphering the Environmental Agenda

The good news is that China’s government has put environmental issues high on the national agenda. President Xi Jinping announced in 2020 plans to target peak CO2 emissions by 2030 and to transition toward carbon neutrality by 2060. But deciphering the details of environmental efforts in a vast, state-run economy isn’t easy. And since SOEs account for a significant share of China’s business activity and an even bigger share of its emissions, they are an integral part of its carbon-neutrality equation.

To gain insight into China’s decarbonization efforts, AllianceBernstein (AB) has partnered with the Columbia Climate School at Columbia University in a workshop program entitled The Making of a Green Giant: Decarbonization with Chinese Characteristics. The webinar series aims to help investors explore the intersection of technology, investment opportunities and the energy transition in China. Experts from Columbia and AB tackle topics such as energy policy, solar and wind energy, electric vehicles and industrial manufacturing. The workshop began in June as part of AB’s ongoing collaboration with the Columbia Climate School, where AB is the founding member of the school’s Corporate Affiliate Program. The collaboration aims to help investors learn about the science of climate change, which promises to affect companies around the world.

For China, decarbonization considerations are tightly tethered to economic development and continued growth. China is a “hybrid superpower,” meaning it has many attributes of both an advanced economy and a developing economy.1 This combination of attributes, and notably its developing country characteristics, matter for energy consumption and policy, as projections by specialized energy agencies consistently point to further increases in energy demand for China, in stark contrast to advanced economies.

SOEs Are Everywhere

SOEs are at the heart of China’s green reform story. Wherever you look in China’s carbon-driven economy, you will find SOEs, from coal-fired utilities to oil suppliers, heavy industrial players, transportation groups and financial firms.

Yet SOEs are also dominant in China’s renewables and other clean energy industries. The rapid proliferation of solar, wind and hydroelectric power in China couldn’t happen without them.

Critics might say that SOEs are inefficient and poorly managed. But that reputation misses the point: SOEs are key players in China’s effort to decarbonize its economies and, like private companies, aren’t created equal and should be judged on their merits. What’s more, SOEs account for about a third of listed Chinese shares, so they can’t really be avoided by investors seeking to allocate to China’s equity markets.

When it comes to green reforms, the ecosystem in which SOEs operate is a web of interlinked entities that underpin the implementation of government policy. Mechanisms of interaction between the government, regulators, shareholders and company management will shape the environmental shift.

In economies dominated by private companies, incentivizing reform is relatively straightforward. Private shareholders want to maximize profits, so policies such as emissions-trading systems and carbon taxes can be very effective. Businesses that don’t proactively adjust will pay a price—and earnings will suffer.

Government shareholders have much broader objectives. Despite its rapid development, China still faces the huge challenges of a developing economy, including major income disparities between regions and the lack of access to clean cooking for 400 million people. The government’s policy goals include economic development, social development and access to energy, which must be considered along with efforts to reduce CO2 emissions. As a result, we believe market-based policies are too one-dimensional for the Chinese system and won’t necessarily achieve the desired objectives.

Case Study: Stranded Assets and the Economics of a Chinese Power Plant

These differences can be more sharply examined by analyzing the economics of a Chinese power plant and stranded-assets risk.

Stranded assets are a common theme in investment analysis of the global energy transition. It refers to the possibility that investors may overinvest in fossil fuels and not be able to recoup investments at a reasonable rate if green regulation curtails operations of dirty plants. Yet concern about stranded assets manifests itself very differently for private sector investors in publicly traded companies than for government holdings in SOEs. These differences help explain why China continues to build coal-fired power plants alongside increasing its decarbonization efforts.

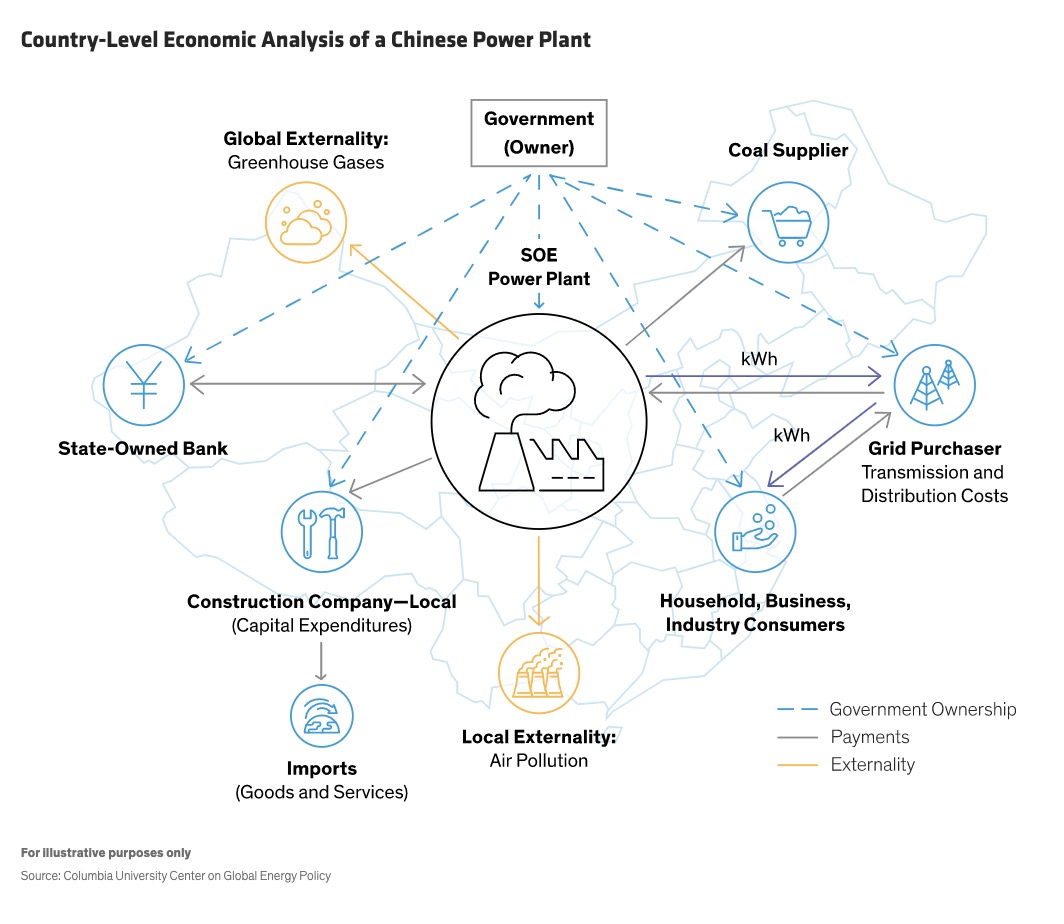

In China, building a state-owned coal-fired power plant involves many SOEs (Display). These include a bank, local construction company, coal supplier and grid purchaser. Their relationships must be factored into the government’s financial analysis of the power plant.

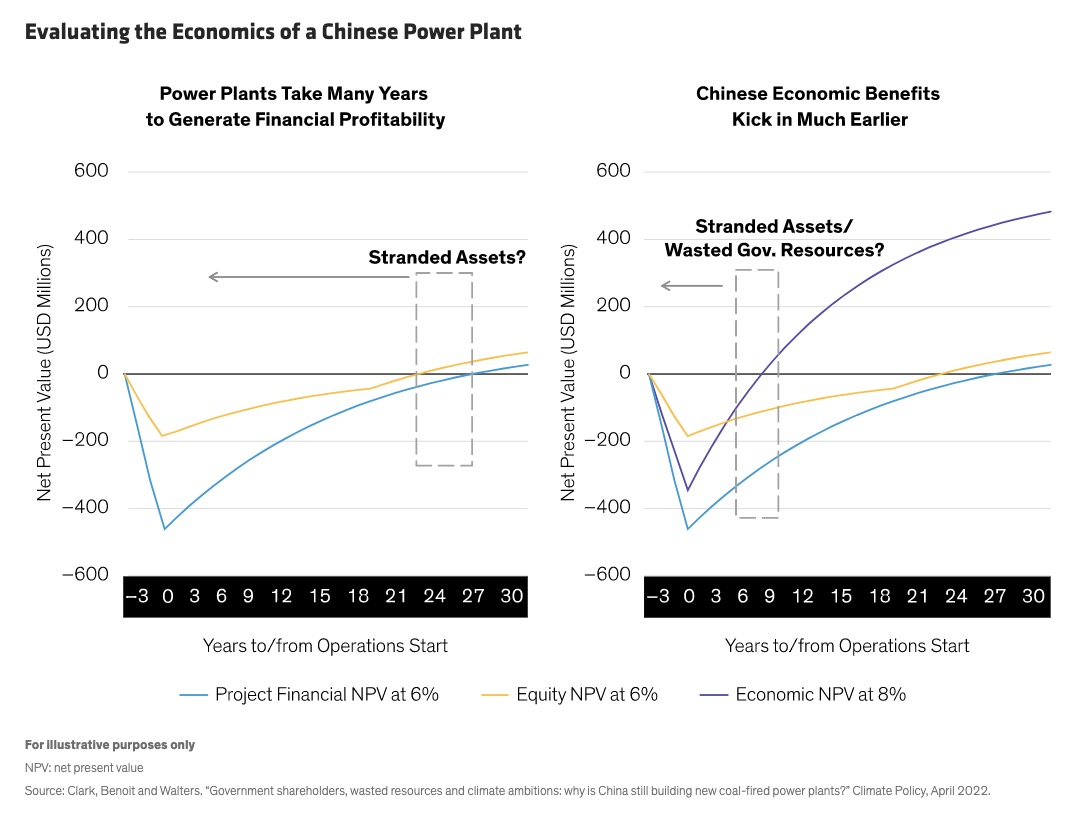

For our example, Columbia University’s Center on Global Energy Policy has modeled the cost of electricity and capital costs by assuming an 80% debt/20% equity leverage ratio and capital and operating costs consistent with the Chinese market.2 To evaluate stranded-assets risk, the key question is: How long does it take to generate an overall positive return to the company?

For a private plant, it could take more than 20 years. So if a coal-fired plant is forced to shut down 12 or 15 years after it was built, investors would get stuck with stranded assets and a negative return on their investment (Display). This is a real risk in the rapidly evolving regulatory environment.

The Chinese context is completely different. That’s because the shareholder of the power company is the government, which also owns multiple entities tied to the plant—and didn’t build the plant only to generate profits for the utility. The broader goal is to supply cost-effective electricity to households, businesses and consumers.

Seen through this lens, the Chinese SOE plant generates a much higher return than a privately owned plant. It turns an economic profit for the government shareholder by year seven in the modeled (albeit simplified) illustration above. As a result, assets would be stranded only if the plant shuts down in year eight or thereafter—a highly unlikely scenario. This helps explain why even though some Western analysts say many Chinese plants are unprofitable, the Chinese government is not losing money on those facilities.

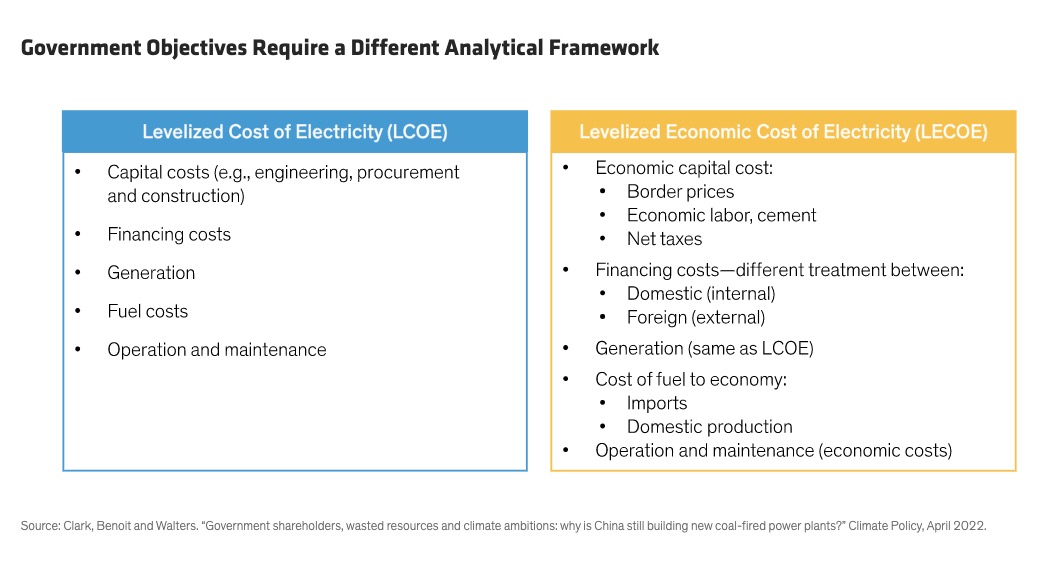

Based on this simulation, in a recent article published by Climate Policy, researchers Alex Clark, Philippe Benoit and Jonathan Walters argued that the standard metric for analyzing the cost of electricity production is too narrow for the Chinese reality. The levelized cost of electricity (LCOE) is a well-known measure to determine whether it is economically sensible to invest in coal, solar or wind power through a standardized comparative analysis. But for China, the study proposed a levelized economic cost of electricity (LECOE) as a complementary and in some ways more appropriate way to gauge the government’s broader cost-benefit analysis. The LECOE incorporates key inputs (such as domestic versus foreign financing costs, import fuel prices versus domestic production costs, and taxes) in the evaluation using country-level economic methodologies, rather than traditional financial tools (Display).

Integrating ESG Issues in China’s Top-Down Economy

Why does this distinction matter for investors? Because once we acknowledge the systemic difference between a Chinese government-owned power plant and a private plant, we can ask the right questions about how companies fit into China’s carbon-neutrality plans. Beyond the example above, the SOE framework is found in many other areas and industries that will participate in China’s green reforms.

Investors must realize that much of the impetus for environmental efforts in China comes from a top-down approach that starts with its political leadership. As a result, analyzing the green credentials of Chinese companies requires a different ESG approach than investors typically apply to Western companies.

For example, consider corporate governance. Standard ESG ratings tend to give Chinese SOE companies low scores on governance. Most boards aren’t composed of 50% independent directors. Compensation isn’t usually disclosed. Related-party transactions—because of the SOE ecosystem—are commonplace.

Government control of companies also means that top-down policy changes on environmental issues can have a profound effect on business decisions. We believe that China is serious about the long-term need to address climate change because its own economy and population will benefit. Listening closely to the policy noises in China can provide important clues about how companies will behave.

Investors can discover how this is playing out by engaging with company management teams. AB’s China Equities team has found that SOEs are often more comfortable talking about climate goals than private companies are. Private companies in China are also subject to a degree of government influence (a relationship that has fluctuated over time), yet they are driven by profit motives similar to those of their Western peers. Some have not yet embraced the idea that going green is good for shareholders.

Engaging with Management: SOEs Are Listening

As active managers, AB’s China Equity team routinely engages with company management. These efforts help us gain insight on a company’s ESG commitment, behavior and impact on the business. In part, given the weight of the government shareholder, it’s harder to influence the managements of Chinese SOEs than publicly traded Western peers’. However, private investors (both equity and debt) do have a role to play.

First, Chinese SOEs—and their government shareholders—are generally keen to attract foreign investment and increase their share prices; they want to hear what shareholders have to say. Second, in the Chinese corporate and finance system, SOEs are meant to be responsive to capital markets where possible; this includes considering international private capital as a prospective source of funding. Third, engaging with management can help investors learn which companies are more conscious of ESG issues in their operations and how to distinguish between good and bad ESG actors.

Through these engagements, AB has discovered that responsible companies don’t neatly align with the SOE or non-SOE labels, or with the preconception that SOEs might be laggards on ESG issues. For example, we recently engaged with one very large, privately held technology company and found that it was far behind the curve, devoting few resources to ESG.

In contrast, China Yangtze Power, a large SOE, is quite proactive on sustainability issues. The company is best-known for its Three Gorges Dam, the world’s largest hydroelectric power–generating facility. In our conversations with management, we discovered that even though the company is a hydroelectric generator, it produces CO2 emissions and is working on plans to improve transparency and disclosures on environmental issues. The company has also taken significant biodiversity initiatives, including the establishment of an institute to help protect Chinese river sturgeons. Though China Yangtze is an SOE, it is attuned to investors’ ESG concerns and, of course, reputational issues for itself and its shareholder, the government.

Companies like these are vital to China’s decarbonization efforts. They also offer investors a window into how the government will navigate decarbonization challenges over time. While the government has pledged to combat climate change, it’s balancing a precarious macroeconomic agenda and the need to foster domestic GDP growth, so there will be ebbs and tides in policy implementation.

Can the Climate Agenda Succeed?

Success, in particular within the broader international capital market context, will depend on several factors. First, investors and energy policymakers must acknowledge that China’s economic structure warrants a different approach. Free-market incentives such as emissions-trading systems and carbon taxes are less effective at delivering results in China, in our view.

Second, China needs a climate policy toolkit that is appropriate for its reality. Shadow carbon pricing, for example, which incorporates environmental costs into the analysis of energy and industrial projects, is well suited to SOEs that need to navigate the broad economic goals of their government shareholder with their own corporate-level financial objectives and could help persuade decision-makers to opt for green projects.

Third, more research is needed in areas such as the impact of growing affluence on energy and emissions and, by extension, on SOEs that have remained critical strategic actors in the government’s economic growth strategy. This in turn has implications on how SOEs can finance their low-carbon transition. Gauging the true costs of power and stranded-assets risk can also support sound green decision-making by government owners.

With the right policy guidance and financing, we believe that SOEs can help China make progress on the road to carbon neutrality. Investors who apply an ESG mindset and independent research to China’s unique circumstances will be able to identify companies driving change that stand to benefit as efforts to combat climate change gather momentum.

1Philippe Benoit and Kevin Tu, Is China Still a Developing Country? And Why It Matters for Energy and Climate, Columbia University Center on Global Energy Policy, 2020.

2Alex Clark, Philippe Benoit and Jonathan Walters, “Government shareholders, wasted resources and climate ambitions: why is China still building new coal-fired power plants?” Climate Policy, April 2022.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All