Equity market volatility persisted in the third quarter as investors came to terms with a new reality of high inflation and rising interest rates. With macroeconomic concerns continuing to set the tone, a fundamental approach to companies can help investors chart a course through today’s uncertainty.

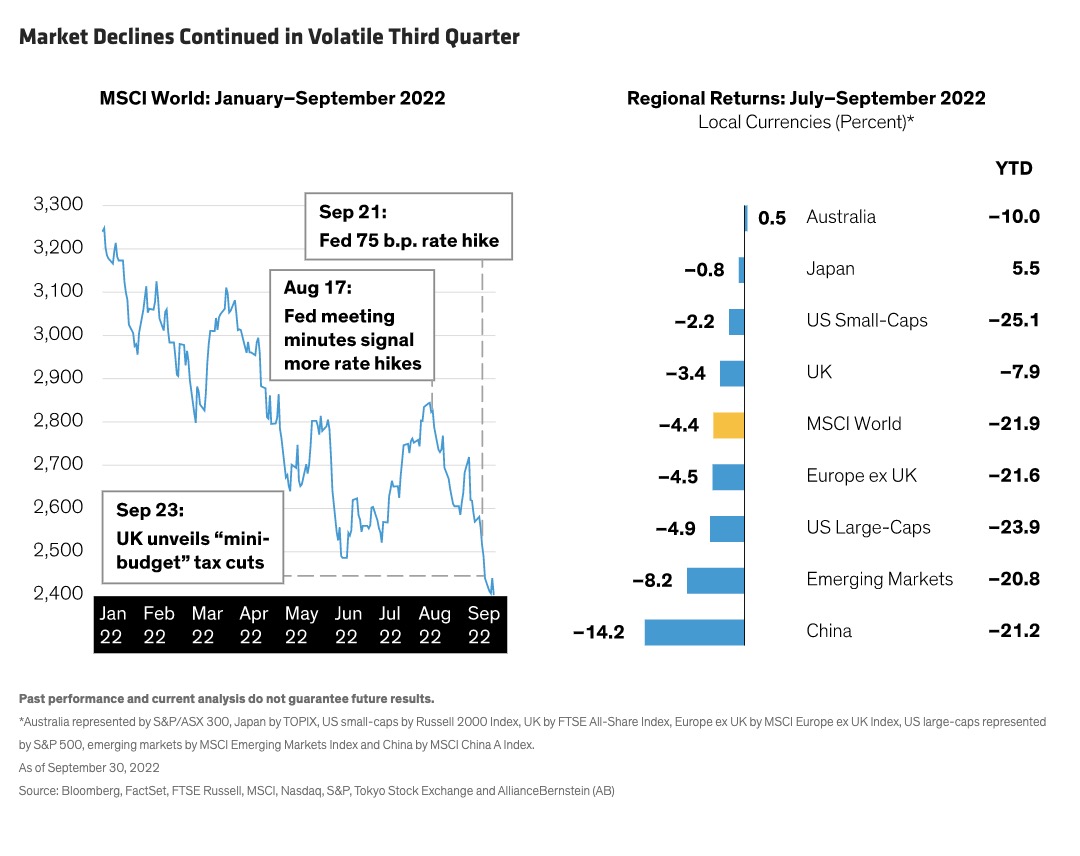

Despite modest advances during the quarter, stocks in most markets gave back their gains and have posted steep losses this year. The MSCI World Index fell by 4.4% in the third quarter in local currency terms (Display) and was down by 21.9% in the year to date. Stocks in Australia and Japan did relatively well. Emerging markets underperformed, weighed down by sharp declines in China.

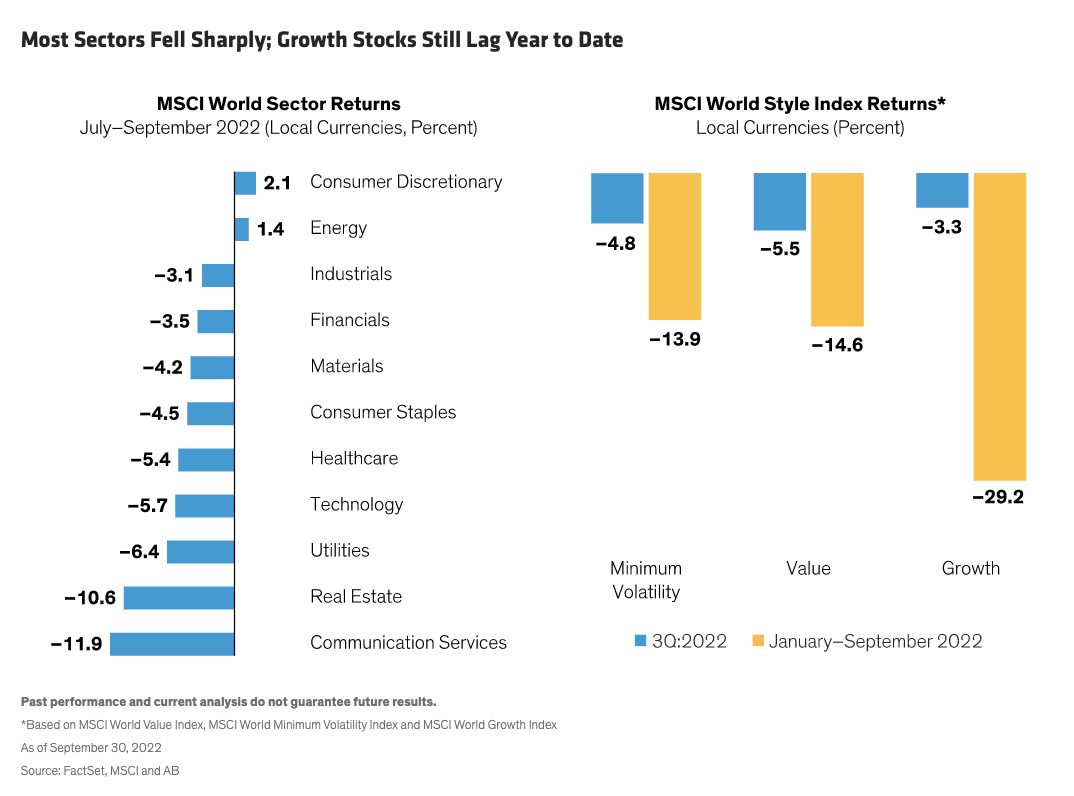

Most sectors declined during the quarter. Consumer discretionary stocks—previously a big casualty of growth fears—advanced. Energy companies continued to rise, fueled by high oil and gas prices. Healthcare, technology and communications underperformed. Growth stocks outperformed value stocks in the quarter yet have trailed by a wide margin so far this year (Display).

Inflation and Interest Rates Set the Mood

As the fourth quarter begins, the mood is gloomy. The US Federal Reserve has hiked interest rates sharply and is committed to an aggressive policy stance. There is no “painless way” to rein in high inflation, said Fed Chair Jerome Powell on September 21, as the Fed raised its benchmark policy rate by 0.75 percentage point, taking the federal funds rate target to between 3% and 3.25%. Powell’s statement was seen as an acknowledgement that the US economy is in for a hard landing—and possibly recession.

In Europe, the Bank of England and the ECB also face a tricky balancing act, complicated by an impending energy crunch. Soaring natural gas prices ahead of winter threaten potential fuel rationing because of the loss of supply from Russia, as the war in Ukraine grinds on. In the UK, the new chancellor of the Exchequer Kwasi Kwarteng unveiled a mini-budget including massive tax cuts and fiscal easing measures at a time when inflation exceeds 10%. The moves rattled investor confidence, prompted dramatic declines in the British pound and raise the risks of destabilizing the economy. Fears are rising that the eurozone may be on the brink of recession as well.

The dynamics are different in Asia. Japan may be one of the world’s only developed countries that would welcome higher inflation, and its central bank is keeping rates at very low levels. China is also on a different course, as policymakers are loosening conditions to support an economy weighed down by a COVID crackdown earlier this year and a faltering property market. Economic growth data still look weak.

Will the US or global economy slip into recession? When will inflation ease and where will it settle? How high will interest rates go—and for how long? What about escalating geopolitical risk, from the effects of the war in Ukraine to China-Taiwan tensions?

Nobody knows the answers. Yet for most of this year, equity markets have violently traded on this unholy trinity of rising inflation, rate hikes and growth fears. To be sure, inflation and growth impact company cash flows and earnings, and interest rates play a key role in determining equity valuations. But when macro trends are such a huge driver of market movements, it tends to cloud investors’ vision of company-specific developments that ultimately determine future equity returns.

How Can Investors Gain an Edge?

With so much uncertainty, it’s almost impossible to develop high conviction in a single economic scenario. Yet by studying company fundamentals—where our analysts have skill, knowledge and experience—we can gain a better understanding of how businesses will fare under a range of likely outcomes. This may not insulate holdings from volatility. But it can position portfolios for long-term success by pinpointing companies that are well positioned—or strategically adjusting—to evolving business conditions.

From a bird’s eye view, the earnings landscape looked eerily complacent at the start of the third quarter. Sell-side earnings estimates had generally not come down, suggesting that market participants were not yet fully anticipating the impact of the economic storm. We believe this is unsustainable.

There will certainly be more warnings to come as the third-quarter earnings season begins in October. Investors must comb through the company reports with a magnifying glass and step up engagement efforts with management to identify potential casualties—and surprising opportunities.

Asking the Right Questions: From Pricing Power to Margin Pressure

Pricing power will continue to be a key differentiator in an inflationary world. But identifying quality companies with pricing power requires deep business expertise. For example, one of our investment teams engaged with food producers that have US and UK brands. To assess their ability to increase prices, we study their brand power in each market and ask whether premium products are vulnerable in a tougher economy. Even if they can raise some prices, will it be enough to cover cost inflation and/or lead to a reduction in demand? Answering questions like these hundreds of times over—across industries, companies and countries—is key to determining whether a stock will succumb to current pressures or turn out to be a strong long-term investment.

It’s also important to pinpoint the source of pressure on a business—a tough task when companies are being pounded by multiple economic forces. Consider supply chain bottlenecks. In the auto industry, it’s unclear whether weak sales volumes reflect supply chain snags or deteriorating demand. Supply chain issues are more likely to be resolved sooner. Investors must investigate how industry dynamics are unfolding on a company-by-company basis.

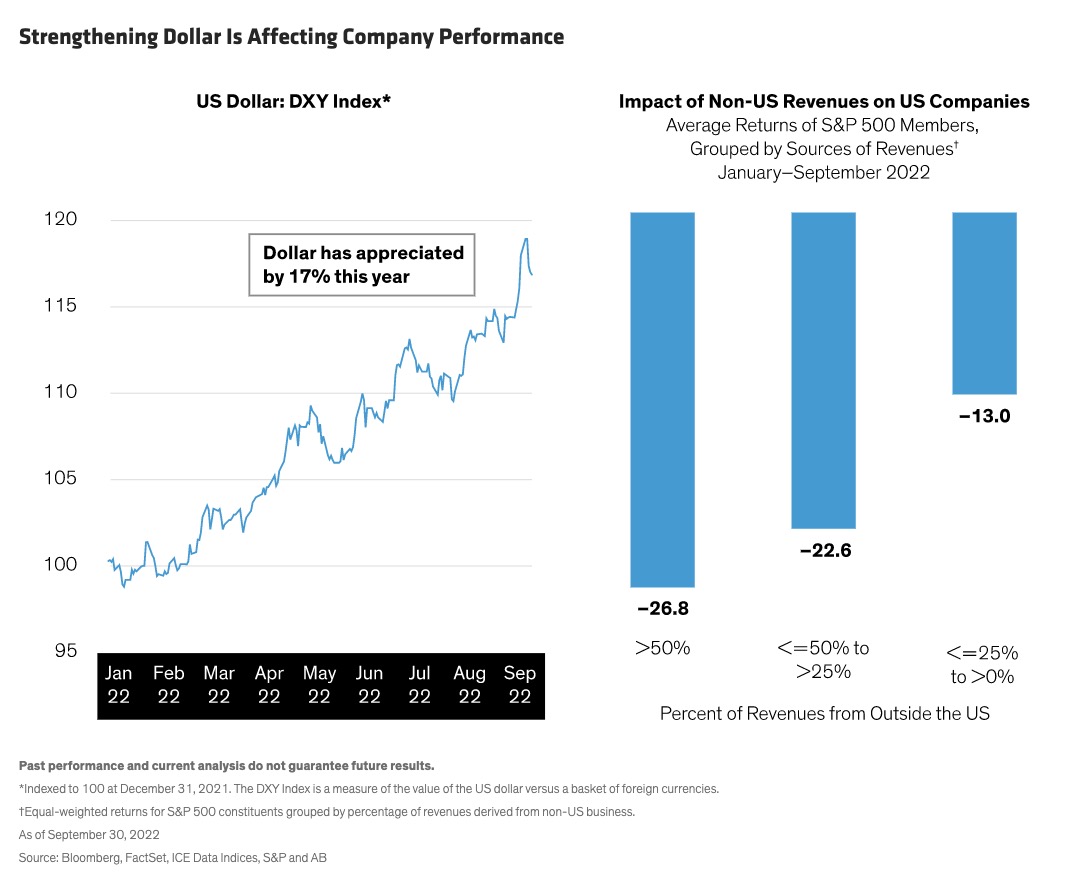

Issues like these will determine whether companies can maintain profit margins to support earnings growth. This warrants a closer look at myriad inputs from commodity costs to currency moves, as the sharp appreciation of the US dollar this year will have diverse effects on companies (Display). Projecting earnings and cash flows is very challenging in such an uncertain environment. But as valuations fall sharply in parts of the market, we can begin to develop conviction by asking whether a range of earnings outcomes are priced into the stock or not.

Rediscovering Opportunities: From Technology to Decarbonization

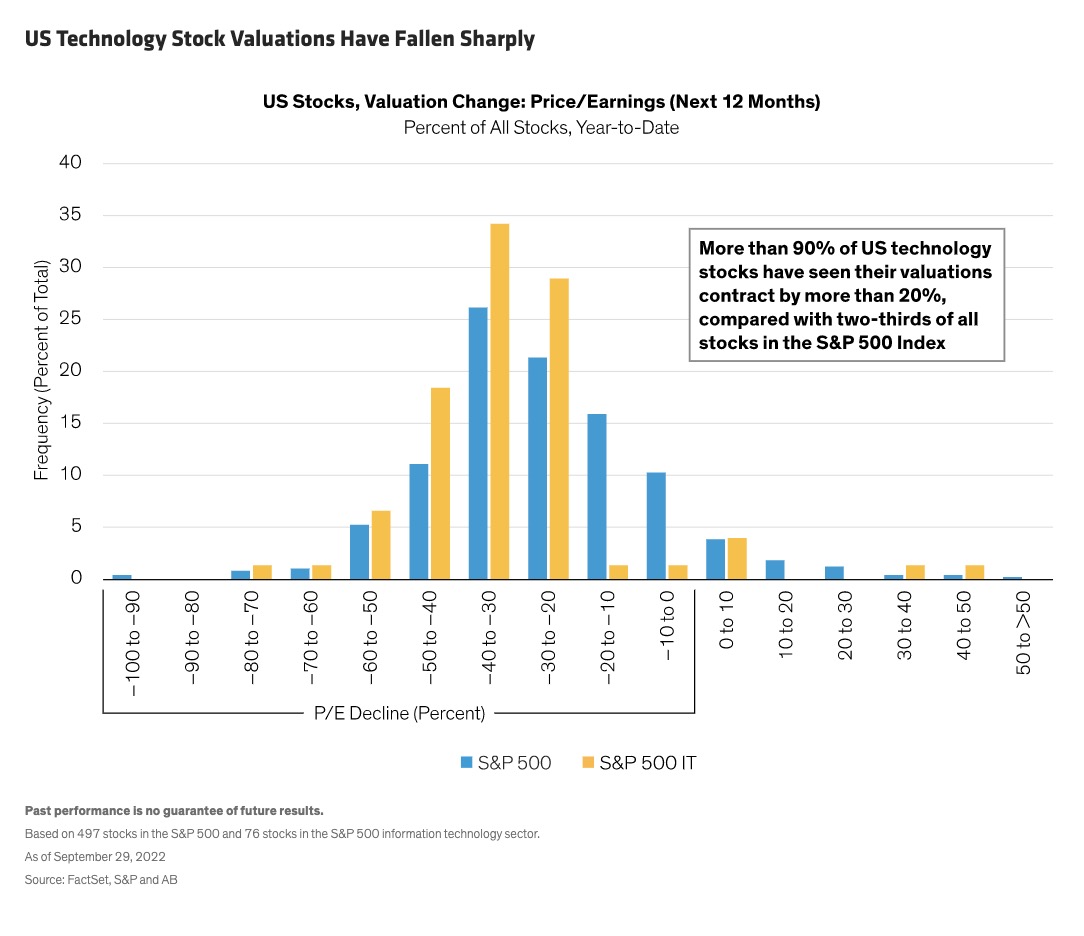

Growth stocks are a case in point. The Goldman Sachs Non-Profitable Technology Index has tumbled by nearly 70% from its peak last year. Some lossmaking technology companies had questionable business models even in better times. But US technology stock valuations have contracted across the sector (Display). Here, and in the broader growth market, select stocks with solid business models are trading at valuations we haven’t seen in years. This allows growth portfolio managers to identify attractive entry points in companies with relatively solid profitability and earnings prospects that might not have been accessible previously. In other words, we can upgrade the earnings quality of a portfolio at very attractive prices.

In the technology sector, the severe underperformance is overshadowing opportunities that probably won’t be derailed by current uncertainty. While consumer technology growth is starting to slow as some of the tech giants mature, we believe a new phase of innovation is beginning—the transformation of tech-enabled infrastructure, offering solutions to global problems from shortages of labor and resources to inflation and environmental issues. No matter what happens to the economy, we think this revolution will fuel demand for cloud-based services, robotics and alternative energy generation.

Indeed, reducing carbon dioxide emissions is a massive, multi-year global effort—and sustainability challenges are not going away. The new US Inflation Reduction Act includes an unprecedented US$369 billion commitment to mitigate climate change. Meanwhile, in Europe, the push to reduce reliance on Russian gas is accelerating regional decarbonization efforts. This will translate into more investment in climate solutions than previously expected, creating investment opportunities in areas ranging from alternative energy to biofuels to electric vehicles—even in a slowing economy.

Staying Diversified in Challenging Markets

Volatility is unlikely to subside soon. But we believe the market has already incorporated the macro challenges to some degree. For example, global flows to equities have fallen to extremely low levels, reflecting investor concerns about the future. We believe these are good conditions for active managers to find opportunities in companies that can weather the storm.

Finding quality companies with resilient characteristics will be the key to constructing robust portfolios during this unsettled period. Since the range of outcomes is very wide—for economies and companies alike—we believe investors should maintain diversified allocations spanning growth, value and core equities, and across different regions. For investors who are concerned about future volatility, low-volatility equity strategies can help cushion the downside in increasingly turbulent conditions.

It’s impossible to predict when equity markets will turn. But history suggests that recoveries can happen very quickly, and investors who miss the strongest days of a rebound will sacrifice significant returns. And markets tend to bottom before the economy troughs.

We are most likely heading into a new economic world order, with higher inflation and interest rates than we’ve seen in many years. Yet as the world rapidly changes, we believe investors will still find they need equity return potential to meet their goals. By remaining laser-focused on company fundamentals, investors can chart a course through today’s uncertainty, which is creating a diverse set of opportunities that offer superior long-term return potential.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

© AllianceBernstein

Read more commentaries by AllianceBernstein