2022 has been a stormy year for bond investors, and the forecast calls for more of the same. Below, we address today’s biggest investment challenges—from persistent inflation to rising rates to a looming recession—the silver linings of higher yields and wider credit spreads, and strategies for navigating bad weather.

The Storm: Global Slowdown, Stubborn Inflation

Rising prices continue to confound expectations that slowing global growth will ease inflation pressures. While the US Federal Reserve and other central banks are aggressively hiking rates to combat inflation, most drivers of today’s high inflation are outside of central banks’ control. The war in Ukraine and the COVID pandemic continue to disrupt fuel, food and goods supply chains, feeding high inflation and throttling global economies.

Sticky inflation may compel central banks to tighten monetary policy still further, which increases the potential for a global recession. In turn, fear of recession is leading investors to take refuge in the US dollar, the world’s reserve currency. As their own currencies tumble, other countries feel the pain of both the strong dollar and higher interest rates. Emerging-market (EM) countries are especially vulnerable, since their sovereign debt is often issued in US dollars; when the dollar strengthens, their debt burden increases.

The upshot? Financial market turbulence may be here to stay for some time.

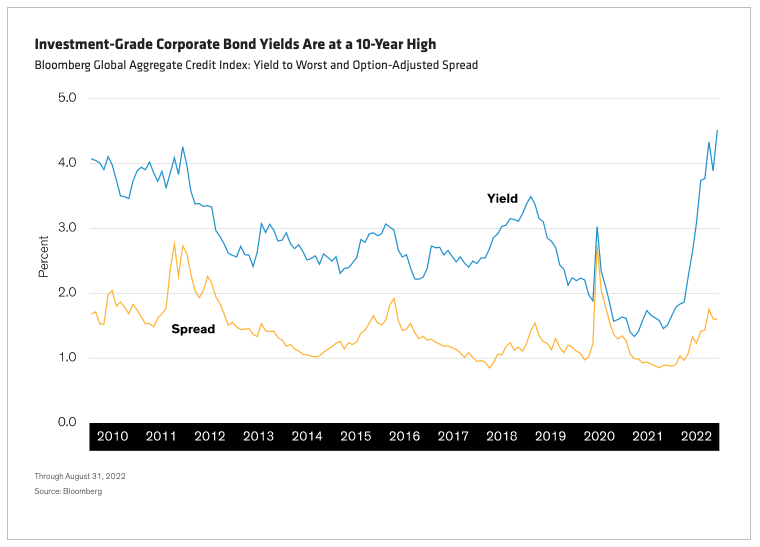

The Silver Lining: Higher Yields

The risk of recession is contributing to market volatility and episodic liquidity challenges, but it’s also creating opportunity. Investment-grade corporate yields and spreads are at multiyear highs (Display), and the yields on high-yield debt now average 9.5%.

The specter of a recession usually scares investors away from corporate debt. Credit fundamentals tend to have weakened prior to any slowdown, causing issuers to enter a downgrade and default cycle as growth and demand slow further. But today’s situation is different.

Today’s issuers are in better shape financially than issuers entering past recessions. The corporate market went through a default cycle just two years ago when the pandemic hit. The surviving companies were the strong ones—and they’ve managed their balance sheets and liquidity conservatively over the past two years, even as profitability recovered. Thus, we expect defaults and downgrades to rise only to average levels over the next year.

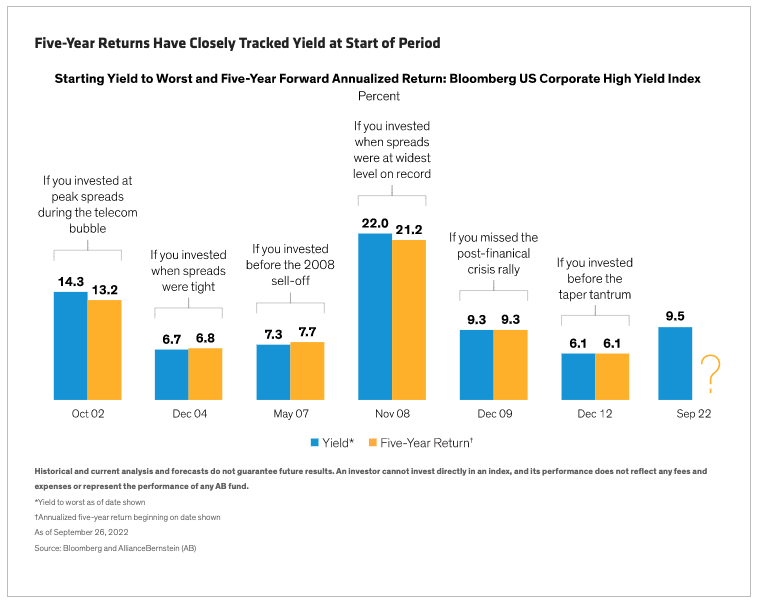

Meanwhile, today’s higher yields signal higher potential returns ahead. For example, the high-yield sector’s yield to worst has been a reliable indicator of high-yield return over the following five years (Display).

In fact, high-yield bonds performed predictably through the global financial crisis, one of the most stressful periods of economic and market turmoil on record. During that period, the relationship between starting yield and future five-year returns held steady, thanks largely to bonds’ consistent income stream.

Strategies for Surviving and Thriving

Here’s how active investors can rise to the challenge in today’s environment:

Be nimble. We expect heightened volatility and liquidity challenges to persist. Active managers should be ready to take advantage of quickly shifting valuations and fleeting windows of opportunity as other investors react to headlines.

Seek (inflation) protection. Because inflation is likely to remain elevated for some time before it falls back to target, explicit inflation protection, such as Treasury Inflation-Protected Securities and CPI swaps, can play a useful role in portfolios.

Lean into higher-yielding credit. Yields across risk assets are much higher today than they’ve been in years—an opportunity investors have been waiting a long time for. “Spread sectors” such as investment-grade corporates, high-yield corporates and securitized assets, including commercial mortgage-backed securities and credit risk–transfer securities, can also serve as a buffer against inflation by providing a bigger current income stream.

Choose a balanced approach. Global multi-sector approaches to investing are well suited to a quickly evolving landscape, as investors can closely monitor conditions and valuations and prepare to shift the portfolio mix as conditions warrant. Among the most effective active strategies are those that pair government bonds and other interest-rate-sensitive assets with growth-oriented credit assets in a single, dynamically managed portfolio.

This approach can help managers get a handle on the interplay between rate and credit risks and make better decisions about which way to lean at a given moment. The ability to rebalance negatively correlated assets helps generate income and potential return while limiting the scope of drawdowns when risk assets sell off.

For now, we encourage bond investors to fix their eyes on the horizon. By taking a longer view, investors can avoid overreacting to today’s headlines—even as they shift tactically to capture opportunities that arise when other investors overcorrect.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein