Investing for High Inflation and Slow Growth

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsInflation and slowing economic growth are a real devil's brew. In isolation, each is bad enough. Together, they are truly toxic.

They would seem to contradict each other. Normally, inflation is a byproduct of too much economic activity—a case of surplus cash chasing around an insufficient supply of goods. In theory, that should mean slowing growth leads to slowing price gains. That hasn't been our experience, though, as annual inflation rates have stayed high—thanks to a mix of strong job growth, rapidly shifting COVID-era spending patterns, and supply chain problems—even as the economy has struggled this year.

That has been a problem for anyone trying to protect the pot that holds their life savings—no easy task when slowing growth is killing investment returns, and every dollar of savings seems worth a smaller portion of goods.

Some commentators have even started warning of the risks of "stagflation," a portmanteau coined in the late '60s combining (economic) stagnation and inflation. However, that may be a worry too far. Although inflation is high and the economy showing signs of faltering, the strength of the job market puts our current travails in a different category than the "classic" stagflation of the '70s.

It's still tough going, though, and investors may be wondering what they can do to make it through. Here, we'll look at a few possibilities.

Any good options?

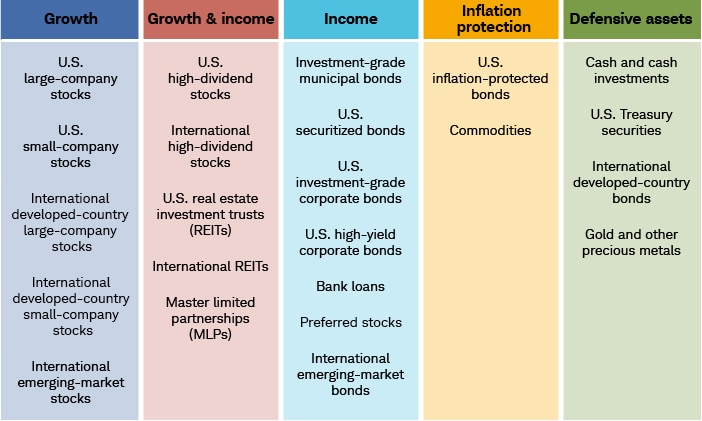

Economic growth and inflation rates are always changing, and different asset classes can prove their worth under different conditions. Some offer returns or income when the economy is growing. Others work best when inflation is rising or the economy is slowing. That's one reason to hold a bit of each—having a mix can generally help you prepare for any environment.

Source: Schwab Center for Financial Research.

For illustrative purposes only.

Of course, the current conditions are proving a particular challenge, as anyone watching the markets is aware. For example, stocks have historically delivered enough returns to help keep portfolios growing faster than inflation over the long term—but they usually need economic growth to do it. Bonds are generally perceived a safe haven when the economy falters, but the Federal Reserve's campaign of anti-inflationary interest rate increases has slammed bond prices, even as it has boosted yields.

That's not to say you're bound to lose in these conditions and should move entirely to cash—that could mean locking in paper losses and potentially missing the start of a recovery. But it probably isn't the time for aggressive risk-taking in a quest for returns. Panic isn't a strategy. Neither is greed.

Our view is that investors should stay in the market, focus as much as possible on the quality of their holdings, and remain disciplined. Of course, quality can be a subjective concept, even in the world of investing. Here's how we think about it.

For your stock allocation

When you're assessing stocks, consider paying attention to these measures:

- Strong profit margins: This is a measure of how much profit a company makes after accounting for its costs.

- High free-cash-flow yield: This measures how much cash a company has available for things like dividends after accounting for its costs and debt service. It is calculated by dividing its cash flow from its market capitalization. A higher yield is generally a sign of financial health.

- Low volatility. This is fairly self-explanatory, but even in today's wildly swinging markets some stocks are simply less volatile than others.

- Positive forward earnings revisions. This captures what companies are reporting in terms of their earnings expectations for the coming months. Granted, the share of S&P 500 companies reporting positive three-month earnings revisions has shrunk significantly this year, from nearly 70% of the index's stocks around the start of the year to about 30% of the stocks as of mid-September.

Consider dividend payers

Dividends, when reinvested, can significantly boost total returns over time, making dividend-paying stocks an attractive option for older and younger investors alike. For example, if you invested $1,000 in a hypothetical investment that tracked the S&P 500® Index on January 1, 1990, but didn't reinvest the dividends, your investment would have been worth $11,687 as of September 2022. If you had reinvested the dividends, you would have ended up with just over $20,000—nearly double.1

Consider a "sector-neutral" approach

Sector rotations can be volatile, with one sector outperforming one month and struggling the next. That's why we recommend keeping your exposure to the various industrial sectors roughly in line with their weight on the S&P 500. (As of the end of September, that means: Consumer Discretionary 11.7%, Consumer Staples 6.9%, Energy 4.5%, Financials 11%, Health Care 15.1%, Industrials 7.9%, Materials 2.5%, Real Estate 2.8%, Info Tech 26.4%, Communication Services 8.1%, Utilities 3.1%).

For your bond allocation

For bond investors, focusing on quality means Treasuries backed by the full faith and credit of the U.S. government, certificates of deposit (CDs), and investment-grade municipal and corporate bonds. Of course, the Fed's interest-rate moves do make things slightly more difficult, as rate changes can play havoc with bond prices. (That's not necessarily a problem, though: Although you might see bond prices dip when rates go up, barring default you're still locked into interest rate and the return of your principal at maturity.)

As things stand now, the Fed looks set to take its benchmark lending rate to as high as 5% by May—but markets expect the Fed to start cutting that rate back again later next year or in early 2024. In a typical rate-hiking cycle, investors might be tempted to pile into short-term bonds—which are more sensitive to interest rate changes—that they can keep rolling forward at maturity in exchange for higher rates. The potential for a reversal makes such a strategy risky, as opportunities for reinvestment could be less appealing if rates start dropping again. That's why it can make sense to have a mix of maturities.

Longer-term bonds, like the 10-year Treasury, are less influenced by the federal funds rate and more closely tied to prospects for inflation and economic growth. As a practical matter, owning some allows you to lock in a yield and shield you from reinvestment risk if the Fed suddenly changes gears.

So, what are some strategies for spreading your risk across maturities?

Consider a bond barbell

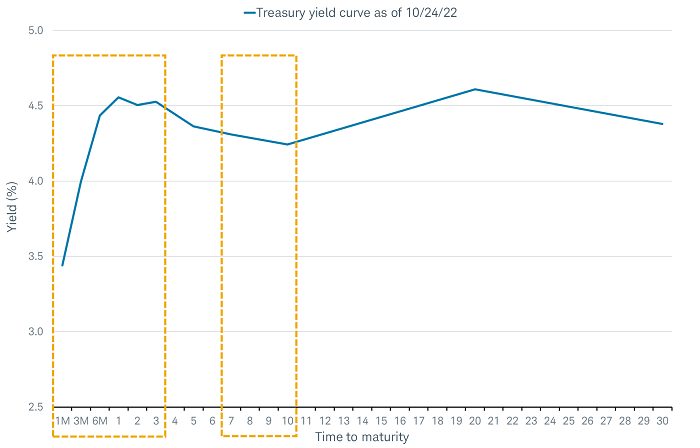

A bond barbell is a tactical strategy that focuses on bonds with two different types of maturities—short-term and longer-term. Today, we prefer maturities of three years or less for the short-term holdings, paired with maturities in the seven- to 10-year area. By concentrating on a combination of short- and intermediate- or long-term bonds—while avoiding what's known as the "belly" of the yield curve, i.e., maturities in the three- to seven-year range—the maturity allocation can somewhat resemble a barbell. A bond barbell can be a good compromise for investors hesitant to move out of short-term investments and into longer-term bonds, as it holds a little of both. The chart below highlights our preferred barbell maturities.

Source: Bloomberg as of 10/24/2022. For illustrative purposes only.

For illustration purposes only.

One thing to keep in mind is that although rates for longer-term bonds are tied to the outlook for growth and inflation, the prices of such bonds tend to be more sensitive to interest rate changes than those of shorter-term bonds. So, if rates rise, the prices of your longer-term bonds could suffer. However, if rates fall as projected, you might see some price gains.

Consider a bond ladder

A bond ladder is a portfolio of individual bonds with staggered, or "laddered," maturities. While a bond barbell is more of a tactical strategy that may depend on the shape of the yield curve and future Fed policies, a bond ladder is a type of "all-weather" strategy that is meant to help provide predictable income with the flexibility to reinvest bonds as they mature.

Picture a ladder with several rungs and spacing between the rungs. The individual bonds are the rungs and the time between maturities is the spacing between the rungs. By staggering maturity dates, you avoid getting locked into a single interest rate. The bonds will mature on a regular schedule—potentially every year, quarter, or month, depending on the number of rungs and spacing of the ladder. At maturity, you could reinvest that principal in a new longer-term bond at the end of a ladder. If bond yields have risen, you'll benefit from a new, higher interest rate and keep the ladder going. If rates have fallen, you'll still have higher-yielding bonds in the ladder. A ladder strategy doesn't mitigate all interest rates, however. If rates rise, prices will likely fall, especially bonds with longer-term maturities.

Consider Treasury Inflation Protected Securities

TIPS are a type of Treasury security whose principal value is indexed to inflation. When inflation rises, the TIPS' principal value is adjusted higher. (If there's deflation, then the principal value is adjusted lower.) The coupon payments are a percentage of the adjusted principal, so your income payments should increase as the principal value rises with inflation. For example, if inflation averages 3% for the next five years, that 3% would be added to the roughly 1.8% "real" yield that five-year TIPS offer today, resulting in a nominal return of 4.8% annually. The higher (or lower) inflation comes in, the higher (or lower) that nominal total return would be.

At maturity, you receive either the adjusted higher principal or the original principal value. In other words, TIPS never pay back less than the initial principal value at maturity.

Market watchers may object here, as TIPS prices have actually fallen sharply this year despite the crazy inflation we've seen. While this isn't normal, it's not impossible for prices to fall more than the principal grows over short periods with high inflation. TIPS can help protect you against inflation over the longer term and aren't a hedge for short-term inflation shocks.

It's also useful to compare TIPS yields to Treasuries using the "breakeven rate," which is what inflation would need to average over the life of the TIPS for it to outperform the nominal Treasury.

The five-year TIPS breakeven rate is now about 2.5%. If inflation were to average more than 2.5% over the next five years, the five-year TIPS would outperform a five-year nominal Treasury. (Likewise, if inflation averaged less than 2.5%, the nominal Treasury would outperform.)

Considering that the CPI rose by 8.2% during the 12 months ending September 2022, a 2.5% breakeven rate seems relatively low.

General portfolio maintenance

If you're finding it tough to identify safe haven investments in this environment, you can also focus on keeping your portfolio positioned to participate in any future recoveries, in line with your long-term financial goals and investing strategy. Here are some moves to consider:

- Rebalance as needed. As the markets rise and fall, the investments in your portfolio will grow and shrink in value—so much so that, over time, your portfolio could become either less or more aggressive than you'd intended. After a long bull run, equities could account for a much larger chunk of your overall portfolio than you'd planned—leaving you exposed to unwanted risk. This is what makes rebalancing so important. By regularly selling positions that have become overweight in relation to the rest of your portfolio and moving the proceeds to positions that have become underweight, you can bring your portfolio back to its original target allocation. It's a good idea to do this at least once a year, and more frequently if markets are making big moves.

- Harvest some investment losses to lower your tax liability. Selling for a loss is never easy, but you can use those losses to offset gains you may have realized in your taxable accounts over the course of the year—a strategy known as tax-loss harvesting—and then reinvest in holdings similar, but not identical to, the ones you sold. (Just beware of wash sales.) If you don't have investment gains to offset, or if you realize more losses than gains, you can use up to $3,000 in losses to reduce your ordinary income this year—and every year thereafter—until the entire loss is accounted for.

- If your plan calls for it, continue making regular investments. Finding the perfect time to invest is nearly impossible. Time in the market is what matters. While staying the course and continuing to invest even when markets dip may be hard on your nerves, it can be healthier for your portfolio and can result in greater accumulated wealth over time.

- Retirees should maintain a reserve. No matter the market conditions, we recommend holding the equivalent of a least a year's worth of anticipated withdrawals in cash investments—such as checking or savings accounts, money market funds, or CDs—with another two to four years' worth in relatively liquid, conservative investments such as short-term Treasuries and other high-quality bonds or short-term bond funds. If you don't have that kind of reserve, you may need to consider other options.

Take the long view

If there's any consolation to be had, it's that historically recoveries tend to follow rough periods. Getting too caught up in the short-term fluctuations of the headline indexes might tempt you to take your eye off how your portfolio is doing. Or worse, to start dumping temporarily depressed assets that might deserve a long-term place in your savings.

If you're young, you probably have enough time for your assets to recover some of what they've lost. If you're older, you may find fresh value in maintaining enough of cash reserve to see you through these periodic drops. In the course of an investing career, they are inevitable.

1Source: Charles Schwab. Monthly data from 01/01/1990 through 9/01/2022. Calculations assume a starting portfolio value of $1,000. Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All