For the first time in a long time, muni investors may be able to earn attractive yields without having to take undue risk.

Like high-waisted bellbottoms and baggy overalls—fashions that were once out but are making a resurgence—2023 should be the year that municipal bonds come back in vogue, too. Although 2022 so far has been a brutal year for the muni market, we expect things to change in 2023. For the first time in a long time, investors can earn appealing income on their muni bond portfolio, which should begin to attract investors back and bode well for total returns.

Recovering from a tough year

So far, 2022 has been characterized by the Federal Reserve aggressively tightening monetary policy in an effort to quell decades-high inflation. Fed policymakers hiked short-term rates six times. However, the worst is likely behind us, as the Fed has indicated it will slow the pace of rate hikes and may be done in early 2023.

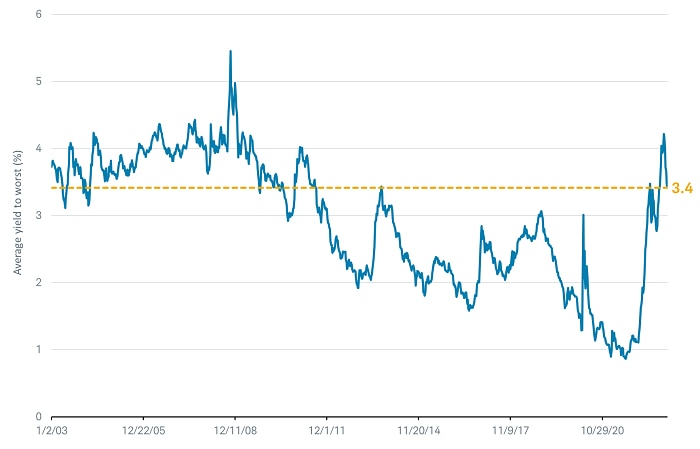

For the first time in a long time, yields are attractive. At the beginning of the year, the yield on the Bloomberg Municipal Bond Index was close to 1%, near the lowest level in the history of the index. That's no longer the case. The yield on the index has risen to roughly 3.4%. While this isn't as high as other fixed income options, municipal bonds are one of the few investment options that are often exempt from federal and potentially state income taxes if the issuer is located in your home state, so after adjusting for this, they are attractive relative to alternatives.

Muni yields are near the highest level in over a decade

Source: Bloomberg Municipal Bond Index, weekly data as of 12/8/2022.

Past performance is no guarantee of future results.

To put that into dollars and cents, at the beginning of 2021, an investor would have needed a muni portfolio of nearly $900,000 to generate $10,000 of interest income. Today, an investor would need a portfolio of roughly $290,000 to generate the same $10,000 of interest income—which, again, may be exempt from federal income taxes.

Themes for 2023

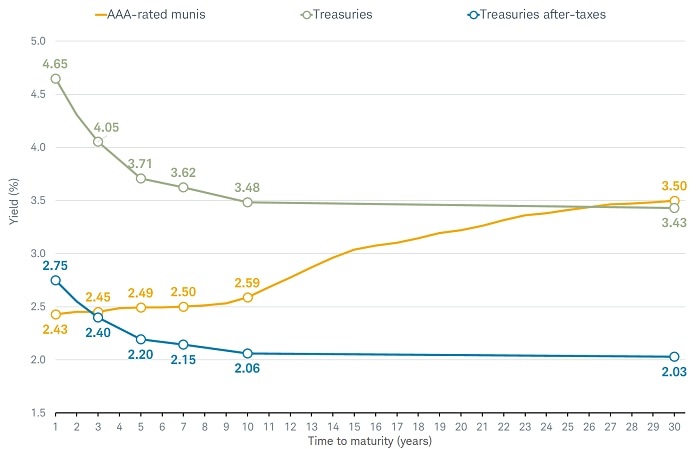

1. We like the intermediate part of the yield curve. We often hear from clients, "why should I invest in intermediate-term bonds if I can get the same or an even higher yield with shorter-term bonds?" While this is true for the Treasury market, it isn't true for the municipal bond market. Unlike the Treasury market, the slope of the muni yield curve is positive. meaning that investors are better compensated for extending out the yield curve rather than staying in short-term securities.

The muni yield is upward sloping, unlike the Treasury yield curve

Source: Bloomberg, as of 12/8/2022.

Municipal bonds are represented by the Bloomberg BVAL AAA Curve. Treasuries assume a 37% Federal and 3.8% ACA tax.

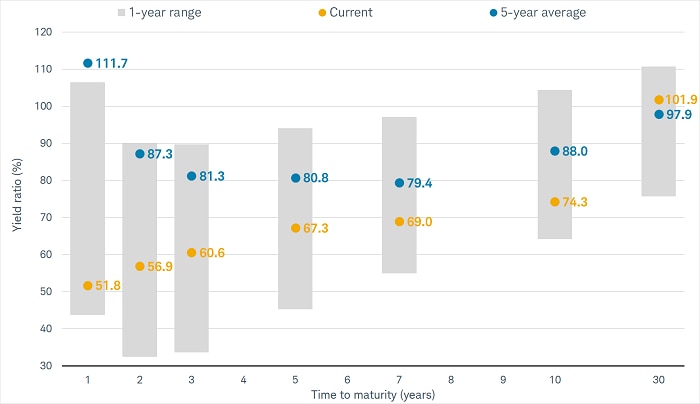

One metric we often use to analyze the relative attractiveness of the muni market is the muni-to-Treasury ratio. It compares the yield on a generic AAA-rated muni bond to that of a Treasury of equal maturity before adjusting for taxes. As illustrated in the chart below, that ratio is below its five-year average for most maturities on the curve. It's especially below its longer-term average for short-term bonds. Tactically, this can be translated to mean that intermediate-term bonds offer more attractive relative yields than shorter-term bonds. This isn't to say that we don't suggest holding some short-term bonds, but we think investors should consider extending duration in 2023 to take advantage of the move up in longer-term yields.

The muni-to-Treasury ratio is below its five-year average for all maturities

Source: Bloomberg, as of 12/8/2022.

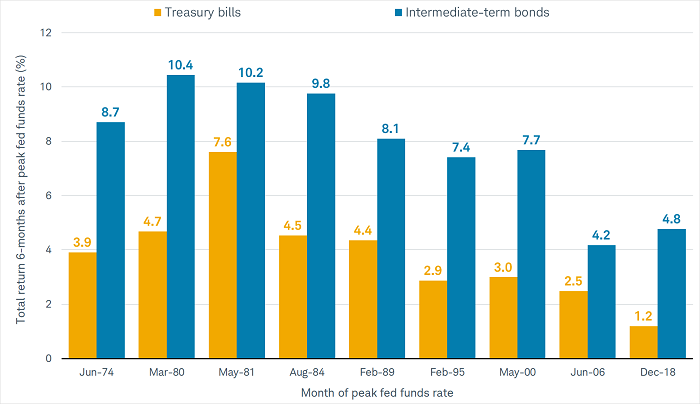

In addition, intermediate-term bonds have historically outperformed short-term bonds in the months after the Fed has completed its hiking cycles. For example, in the most recent cycle—when the Fed stopped hiking rates in December 2018—intermediate-term bonds outperformed short-term bonds by more than 3.5 percentage points, returning 4.8% compared to 1.2% over the six months after the Fed finished hiking rates.

Historically, intermediate-term munis outperform short-term munis after the Fed finishes hiking rates

Source: Ibbotson and Bloomberg, using monthly data as of 11/31/2022.

The Ibbotson U.S. Intermediate-Term Government Bond Index (Intermediate-term bonds) Ibbotson 3-Month Treasury Bill Index (Treasury bills) Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. Includes the reinvestment of interest and/or dividends. Does not include the impact of taxes. For illustrative purposes only. Past performance is no guarantee of future results.

2. We suggest staying up in credit quality in 2023. One of our themes for the broader fixed income market in 2023 is to target higher-rated issuers rather than lower-rated issuers. For example, we think investment-grade corporate bonds appear more attractive than high-yield corporate bonds. In the municipal bond market, this translates to focusing more on higher-rated investment-grade issuers like those in the AA/Aa category or above. We think investors with a greater comfort with risk could also consider some bonds in the A/A category, but would suggest caution with BBB/Baa rated issuers. We believe they should account for only a small portion of your overall muni portfolio, if you have the risk tolerance for it.

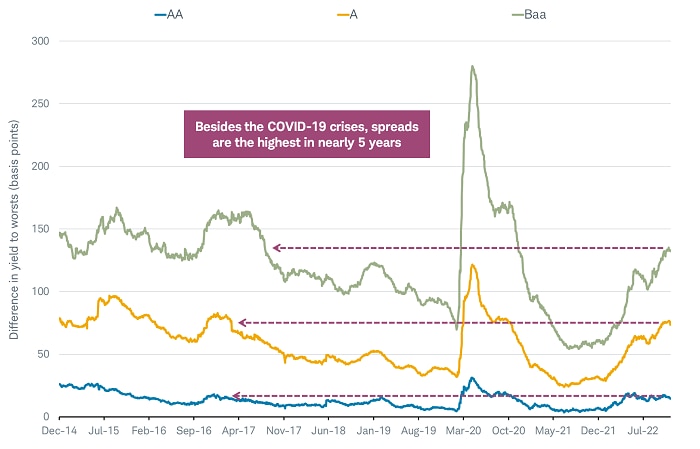

One reason why we suggest staying up in credit quality is because spreads (the additional yield for taking on credit risk) have increased, so investors don't need to target the lowest rungs of investment grade to get higher yields. In other words, at the beginning of the year, the average BBB-rated bond only yielded roughly 1.5%, which was only 61 basis points more than the average AAA-rated muni. Today, the average A-rated muni yields roughly 3.8%, which is roughly 75 basis points more than the average AAA rated-muni. One basis point is equal to one one-hundredth of a percentage point, or 0.01%. In other words, investors are now being better compensated for taking on less credit risk than they were at the beginning of the year.

The chart shows the difference in yields between the AA, A, and Baa components of the Bloomberg Municipal Bond Index relative to the AAA portion of the index. The spread for the A index, for example, has risen to 75 basis points which—aside from the COVID crises— is the highest since early 2007.

Spreads for lower-rated munis have risen

Source: Components of the Bloomberg Barclays Municipal Bond Index, as of 12/8/2022.

Spreads may be due to other factors such as differences in maturities, coupons, or durations.

The other reason we suggest staying up in credit quality in 2023 is that we believe economic growth may slow, which would more negatively impact the finances of lower-rated issuers compared to higher-rated issuers. This could result in less financial flexibility for lower-rated issuers and potentially downgrades if revenues slow too much. We're less concerned with higher-rated issuers, as they generally have revenues that are less economically sensitive than lower-rated issuers.

3. Demand should improve. We expect demand for munis to rise in 2023, which bodes well for total returns. Given attractive yields and our opinion that rates don't have much more upside in 2023, we would expect demand for munis to increase, which should be supportive of total returns for the year.

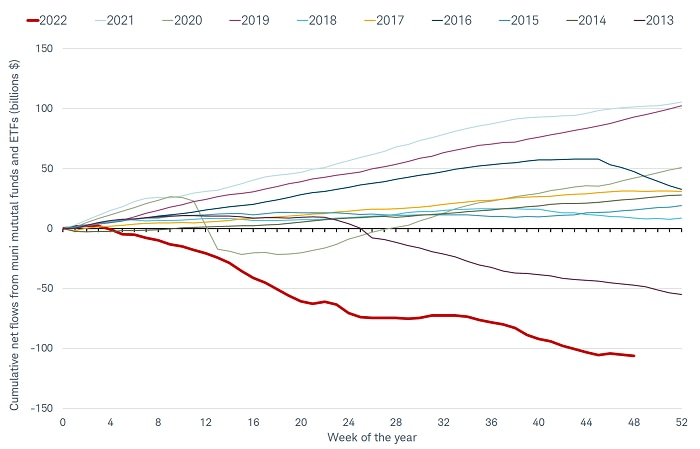

So far, 2022 has been characterized by substantial outflows from muni mutual funds and exchange-traded funds (ETFs), which could have been a headwind to performance—but muni issuance is down slightly less than 18% from the same time last year, so the outflows had less of an impact on total returns. We found that flows from mutual funds and ETFs tend to follow total returns. In other words, when rates rise it results in negative total returns for many funds. Investors experience these negative returns and choose to sell their funds. These outflows can be an impediment to total returns if issuance is elevated.

Muni investors pulled money from muni funds in 2022

Source: Bloomberg, as of 11/30/2022.

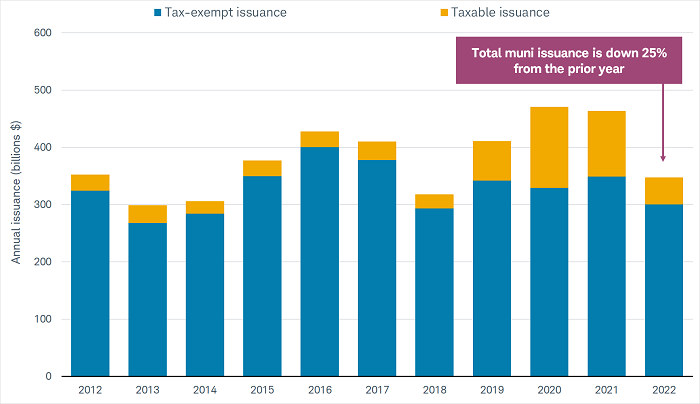

Issuance should continue to remain lower than average, assuming that interest rates don't fall substantially. Historically, higher interest rates have resulted in lower issuance, as illustrated in the chart below. Moreover, state and local government coffers are at record levels, which lessens the need to borrow. Lower issuance combined with increased demand should help support muni returns in 2023.

Bond issuance declined in 2021 and YTD 2022

Source: Bloomberg, as of 12/8/2022. 2022 is year to date (YTD).

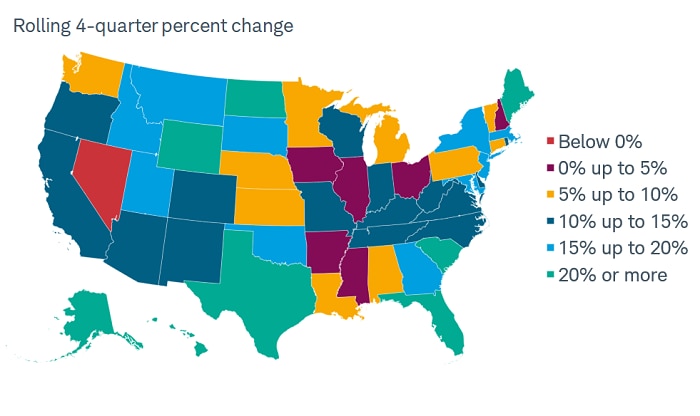

4. A positive credit outlook should also bode well for demand in 2023. State and local government credit quality continued to improve in 2022, and we expect it to remain strong in 2023. State tax revenues have surged to record levels and state rainy-day funds are at record levels, as well. A rainy-day fund is akin to a savings account that a state can tap under certain circumstances if there's a slowdown in revenues. Rainy-day funds can help alleviate the negative impact of revenue slowdowns if the economy falters.

Tax revenues have surged to record levels

Source: Bureau of Labor and Statistics, as of Q2 2022, which was the most recent data available.

The improved financial conditions for state and local governments have translated into ratings upgrades. For example, there have been more ratings upgrades relative to downgrades over the past six quarters, according to Moody's Investors Service, and upgrades outpaced downgrades by a 2.5-to-1 margin in the most recent quarter. The only industries that haven't experienced more upgrades relative to downgrades are health care and housing—two areas in which we suggested caution at the beginning of 2022. A bond usually increases in price if it is upgraded.

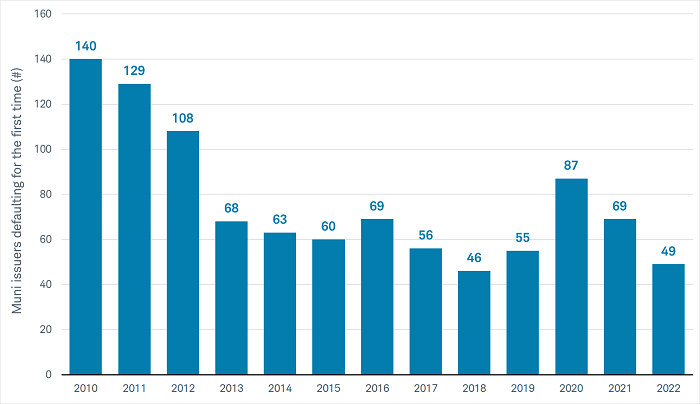

Additionally, defaults remain low, and we don't anticipate they will substantially increase in 2023. Since 2013, there have been an average of 60 first-time defaults per year. We're on pace for around 50 in 2023, which represents roughly one-tenth of one percent of all municipal bond issuers. A default can occur when an issuer misses a scheduled interest or principal payment. Moreover, most defaults are among lower or non-rated issuers.

Defaults remain low and are unlikely to substantially increase in 2023

Source: Municipal Market Analytics, as of 12/8/2022.

Although credit quality is high, we believe that we are at the peak in the economic cycle and if the economy continues to run below-trend growth, the pace of growth for state and local government tax revenues should slow, too. This likely won't lead to an increase in defaults or downgrades, but the pace of upgrades should slow. We're more cautious on issuers that are lower-rated and have revenue streams closely tied to economic growth.

What to do now

After a long and difficult 2022 year to date, the municipal bond market should fare better in 2023. We think that rates will be volatile due to Fed policy and concerns about economic growth. However, for the first time in a long time, investors can finally earn attractive yields without having to take on undue risk.

Schwab clients can log in to research individual municipal bonds, view pre-screened municipal bond exchange-traded funds (ETFs) on Schwab's ETF Select List® or municipal bond mutual funds on Schwab's Mutual Fund OneSource Select List®. For additional help in selecting an appropriate solution for your needs, a Schwab Financial Consultant or Fixed Income Specialist can help.

Investors should consider carefully information contained in the prospectus or, if available, the summary prospectus, including investment objectives, risks, charges, and expenses. Please read it carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

ast performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

1222-21BX

© Charles Schwab

Read more commentaries by Charles Schwab