The Federal Reserve raised interest rates by a half point (50 basis points) on Wednesday in line with forecasts. The new fed funds rate is 4.25-4.50%. While the increase was significant, it was the smallest increase of the past 5 meetings. The prior 4 meetings saw increases of 75 basis points each. They represented the largest individual rate hikes in over 25 years. The rate news followed Tuesday’s release of inflation numbers from the Bureau of Labor Statistics. The Consumer Price Index rose 7.1% year-over-year in November, less than the expected 7.3%.

Tuesday’s lower-than-expected inflation news was bullish for markets, with the March S&P 500 e-mini gaining over 100 points in the aftermath of the release. Wednesday’s fed funds release was in line with expectations, so one might expect the market to react in a muted way. This is especially true since the Fed statement was virtually identical to the statement released November 2 (two words were changed). However, the March e-mini dropped nearly 50 points in the 3 minutes following the Fed announcement. What could have caused the drop?

For that, we can look to the Summary of Economic Projections. The Summary is released at every other Fed announcement, 4 times a year. It contains the “dot plot” or officially “FOMC participants’ assessments of appropriate monetary policy.” The dot plot displays the anticipated target fed funds rate at the end of the next three calendar years. For the September release, the median number for 2023 was 4.6%, while December’s number was 5.1%. With this change, the fed is signaling higher rates over the longer term. The move can be taken with a grain of salt, given that the March release showed an anticipated 1.9% rate for the end of this year. Interestingly, he December release projected a lower terminal rate for the end of 2024 versus September, while the 2025 target and longer run numbers were about the same.

The Summary of Economic Projections is a useful tool in anticipating longer-term actions by the Fed and its projections for the overall economy. Current and past releases can be found at FederalReserve.gov in the Monetary Policy section.

Technicals

The March S&P 500 e-mini was down significantly at mid-day yesterday. The day’s move took the contract below its 9- and 20-day SMA, approaching the 50-day. It approached 3900, a low last seen in early November. The RSI dipped significantly after Tuesday’s rally and saw it approaching 40%. On a 1-month chart with 30-minute candles, the RSI was well into oversold territory at a reading of 8%.

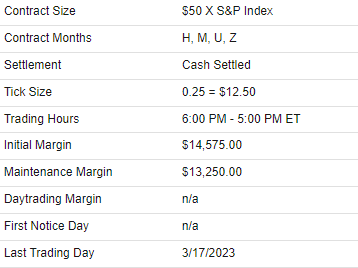

ESH23 3-Month Daily Chart