Past performance and current analysis do not guarantee future results.

*All burger prices include tax. Display excludes 13 EM countries for which historical data for 2011 is not available. June 2011 is cited as a historical reference because this is the earliest available date for which GDP-adjusted data are available.

†EM stocks represented by MSCI Emerging Markets Index, EM bonds represented by JPM EMBI Global Diversified Index and US stocks represented by S&P 500 Index

As of December 31, 2022

Source: The Economist, Eurostat, J.P. Morgan, McDonald’s, MSCI, Refinitiv, S&P and AllianceBernstein (AB)

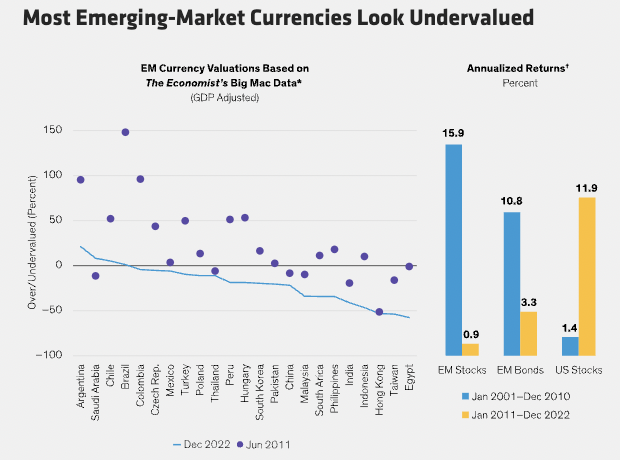

Investors in emerging markets (EM) have endured a decade of poor performance. But things may be changing. Based on The Economist magazine’s data comparing hamburger prices across countries, many EM currencies look cheap today—as they did 20 years ago before an extended rally of EM stocks and bonds.

Since 1986, The Economist has collected data comparing currency values based on the price of a McDonald’s Big Mac in different countries. It is a self-described “lighthearted guide to whether currencies are at their correct level,” based on the concept of purchasing power parity (PPP). The “burgernomics” data are adjusted for GDP per capita to account for differences in wage levels between richer and poorer countries.

A simple observation of The Economist’s data shows that most EM currencies are relatively cheap today (Display, blue line). The South Korean won and Indian rupee are undervalued by 19.6% and 41.2%, respectively. Buying a burger in South Africa or the Philippines is about 34% cheaper than you would expect. The Indonesian rupiah and Taiwan dollar are cheaper still.

There are some exceptions, such as the relatively expensive Argentine peso. But this currency isn’t free floating.

Comparing Currencies with Stock and Bond Performance

How do currency valuations align with market performance? In June 2011, most EM currencies were overvalued, as the purple dots show (Display). That’s because the previous decade’s commodity supercycle fueled currency appreciation in countries such as Brazil, Colombia and South Africa. For many commodity exporters, overvalued currencies ultimately triggered a broader macroeconomic deterioration, and EM stocks and bonds underperformed dramatically from 2011 to 2022.

Rewind to 2001, and most EM currencies were undervalued. Over the following 10 years, EM stocks and bonds surged, driven by huge demand for commodities from China, which was pursuing aggressive growth targets of 10% per year. This led to large foreign direct investment and portfolio flows toward EM stocks, bonds and currencies.

A Good Starting Point

Expectations for EM are low and today’s global economic circumstances are very different from 20 years ago. Inflation is high, China’s growth has slowed and another commodity supercycle isn’t likely.

But we believe attractively valued currencies create favorable conditions for EM countries and companies to overcome the challenges amid a shifting balance of risks. After a lost decade, today’s currency levels also provide investors with a good starting point to get reacquainted with carefully curated portfolios of EM stocks and bonds that capture attractive recovery potential.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

© AllianceBernstein

Read more commentaries by AllianceBernstein