Stock and bond markets were shaken by the recent banking crisis in the US and Europe. Although both US and European authorities took prompt action to prevent damage to the financial system and dampen market volatility, these episodes highlight the importance of risk management and the worth of proven investment strategies that can both mitigate risk and generate worthwhile returns.

Historically, higher-rated short-duration high-yield bonds have provided strong returns with defensive characteristics. Now, with yield curves inverted across North America, Europe and parts of Asia, investors no longer need to increase interest-rate risk (duration) to earn extra income.

Shorter Bonds Make for Lower Risk

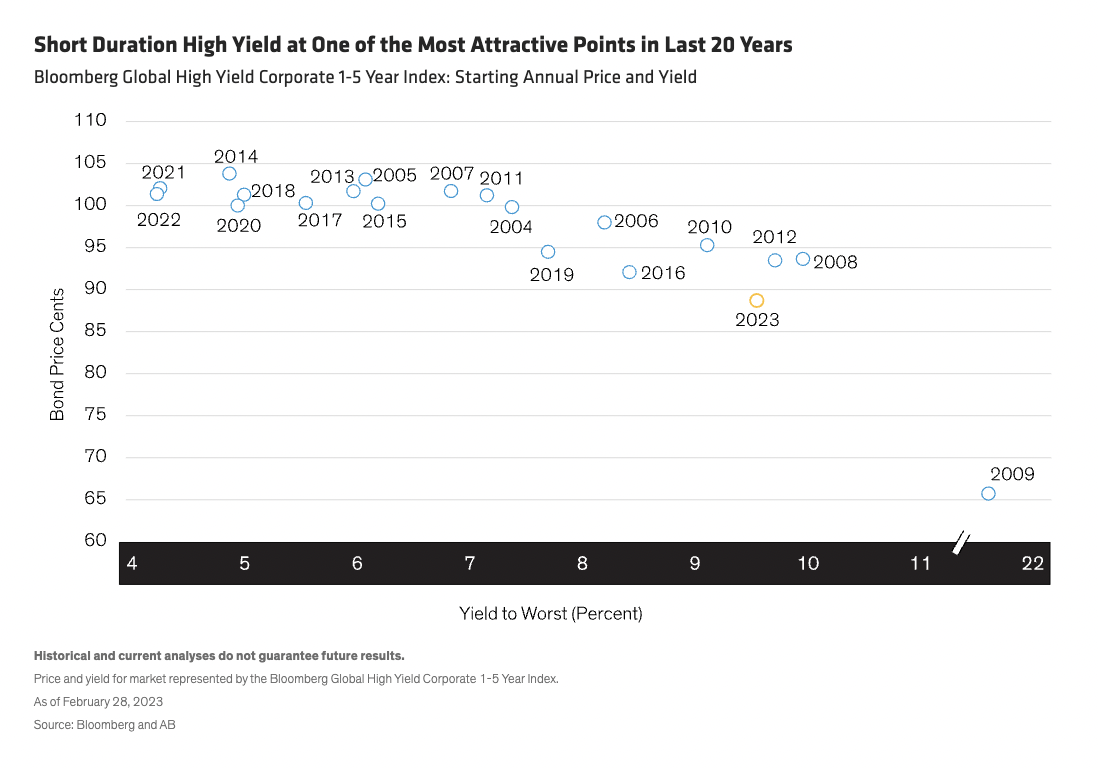

Short-dated high-yield bonds are intrinsically less risky than longer-dated counterparts, as their shorter maturities leave them less exposed to both default- and interest-rate risk. Further, as these bonds currently trade below par (Display), their prices will likely rise as they approach maturity, generating capital gains.

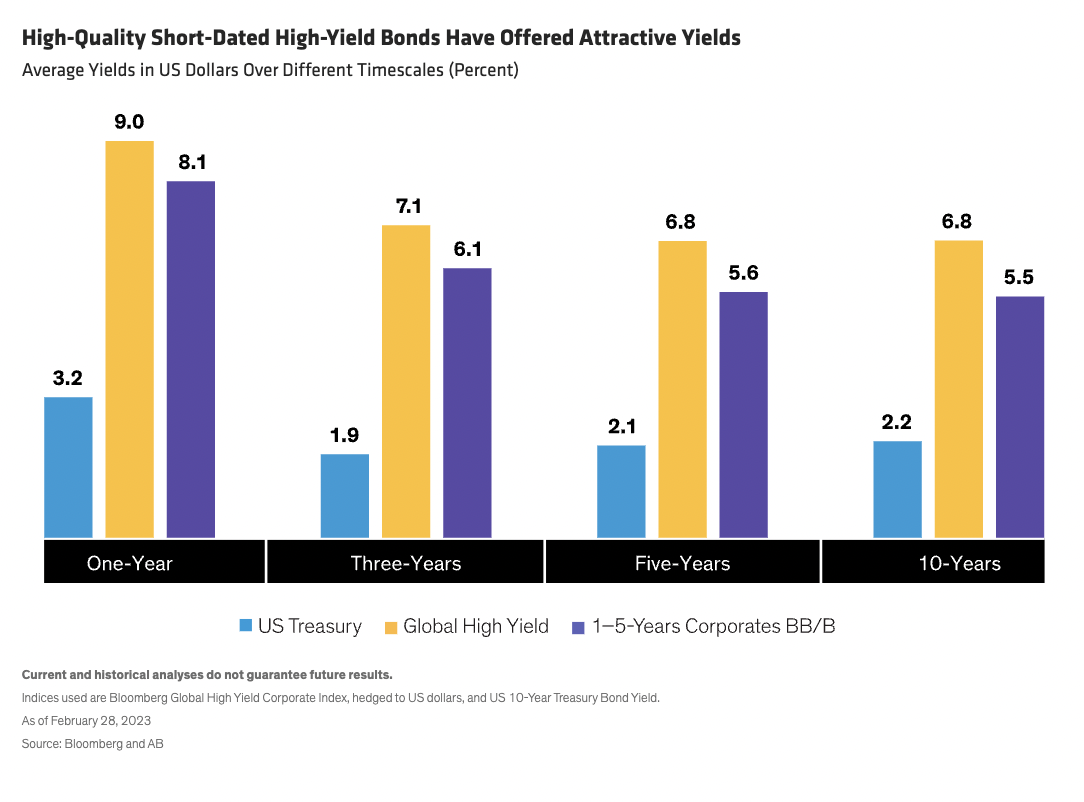

What’s more, by concentrating on the higher-quality segment of short-dated high yield, investors can create more defensive portfolios for a relatively small reduction in yield (Display).

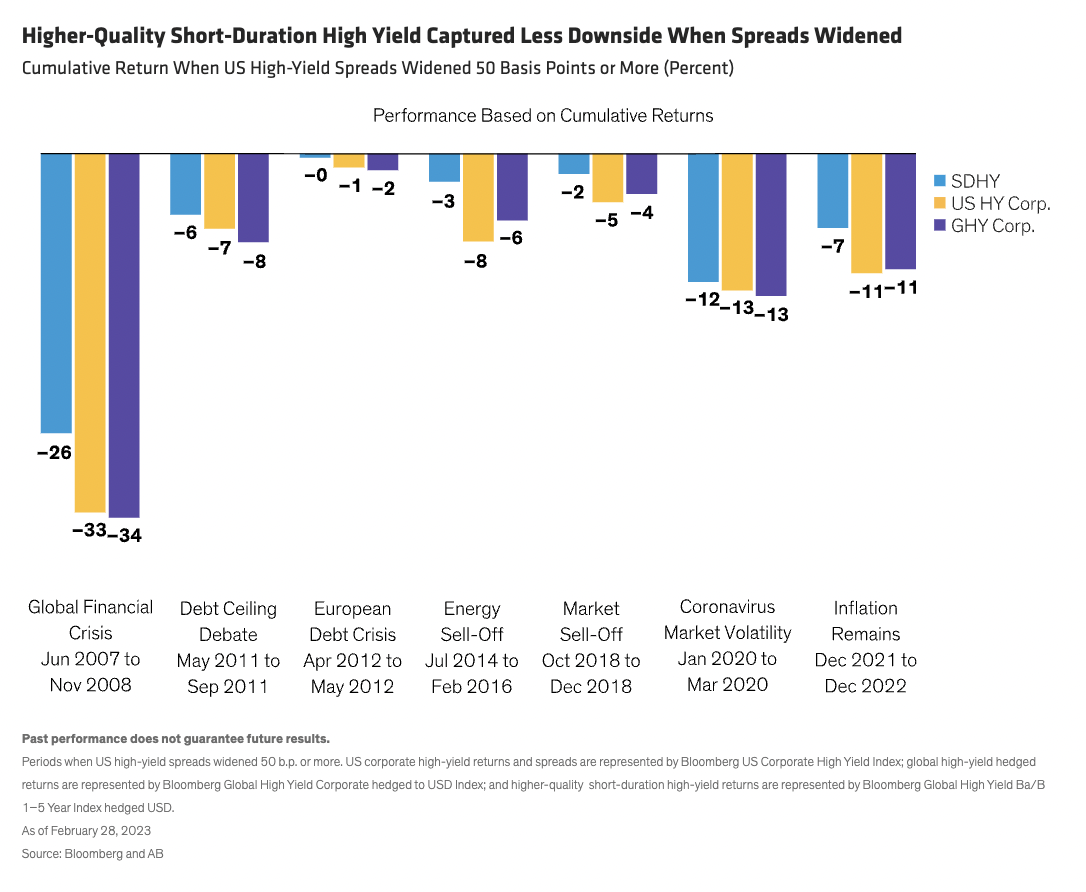

Over the 20 years ending September 30, 2022, BB- and B-rated high-yield bonds between one and five years to maturity captured more than 80% of the broader high-yield market return, while experiencing approximately 50% of the average monthly drawdown. Consequently, they have provided better risk-adjusted returns than their longer-dated (five- to ten-year) high-yield counterparts. But they have really come into their own during periods of extreme market stress. At these times, higher-quality, short-duration high yield has exhibited much lower downside capture than both the global and US high-yield markets (Display).

In our analysis, dynamically managed short-duration high-yield strategies that can allocate tactically to higher-rated assets, including investment-grade bonds, may achieve even more consistent performance. By varying the allocations to return-seeking and more defensive bonds as market conditions change, investors may have the opportunity both to capture higher returns in risk-on periods and to guard against downside risks in choppier markets.

Inverted Yield Curve Favors Shorter Bonds

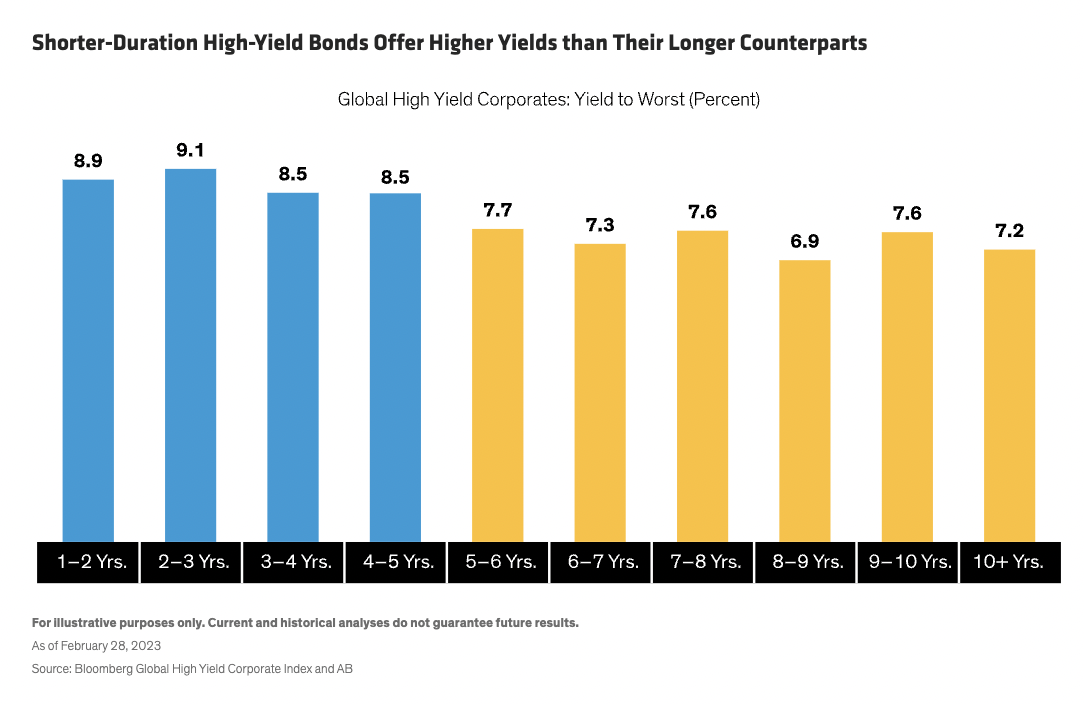

Currently, owing to inverted yield curves, investors have a potentially highly attractive entry point for investing in short-duration high-yield bonds, as high-yield bonds with five or fewer years to maturity offer significantly higher yields than longer-dated counterparts (Display).

In an uncertain world, we think shorter-dated, higher-rated, high-yield strategies could be particularly well-suited to delivering attractive risk-adjusted returns.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein