Global equities were volatile in the first quarter, as turmoil in the banking sector jolted markets. While swift regulatory action helped stem contagion, the crisis dented investor confidence in a fragile market environment and has sharpened awareness of risks created by a new interest-rate regime.

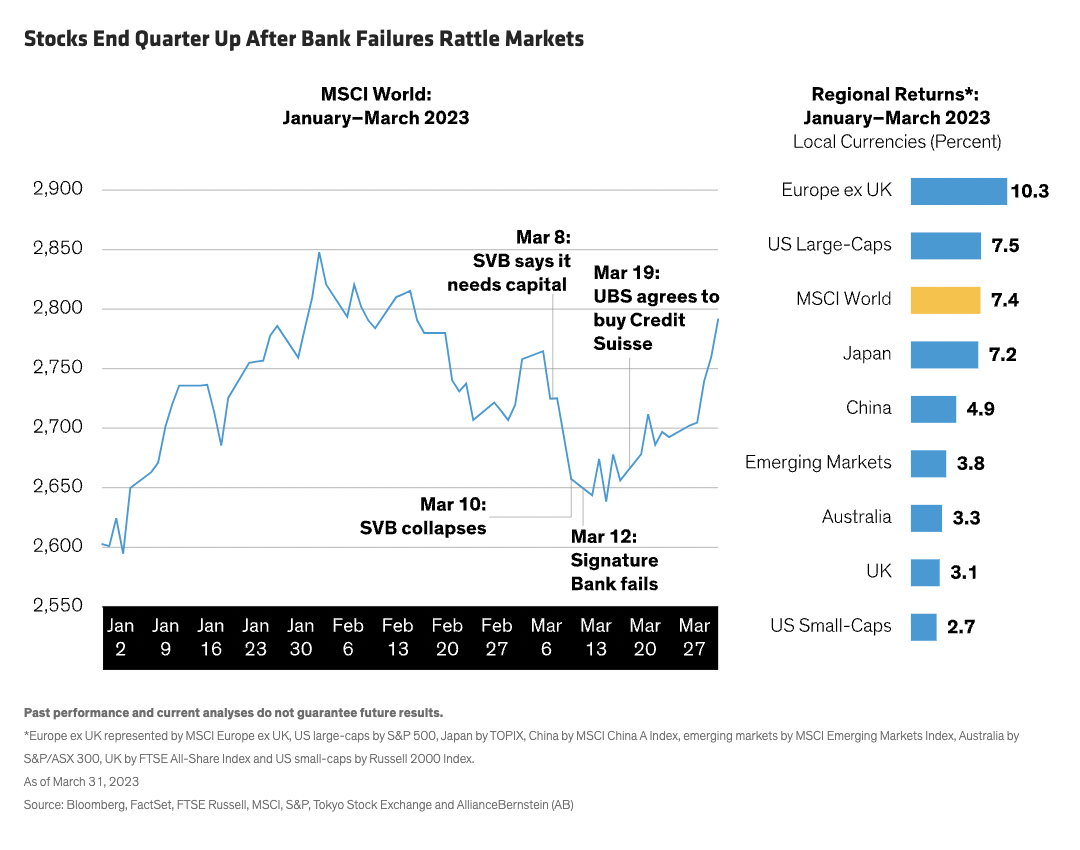

When 2023 began, many investors saw a half-full economic glass. Perhaps inflation and interest rates would fall faster than expected, without tipping the world economy into recession—a scenario which could revive stocks that were badly bruised in 2022. But in March, the failures of Silicon Valley Bank (SVB) and Signature Bank, followed by an emergency rescue of Credit Suisse, delivered a clear message to companies and investors: the US Federal Reserve’s dramatic rate-hiking cycle was making an impact on balance sheets that threatened to pile pressure on businesses and stocks, warranting heightened vigilance.

While stocks ended the quarter strong, return patterns reflected the uncertainty. Stocks rebounded in January but fell in February and the first half of March. After recovering toward quarter end, the MSCI World Index had advanced by 7.4% in local-currency terms during the first three months of the year (Display).

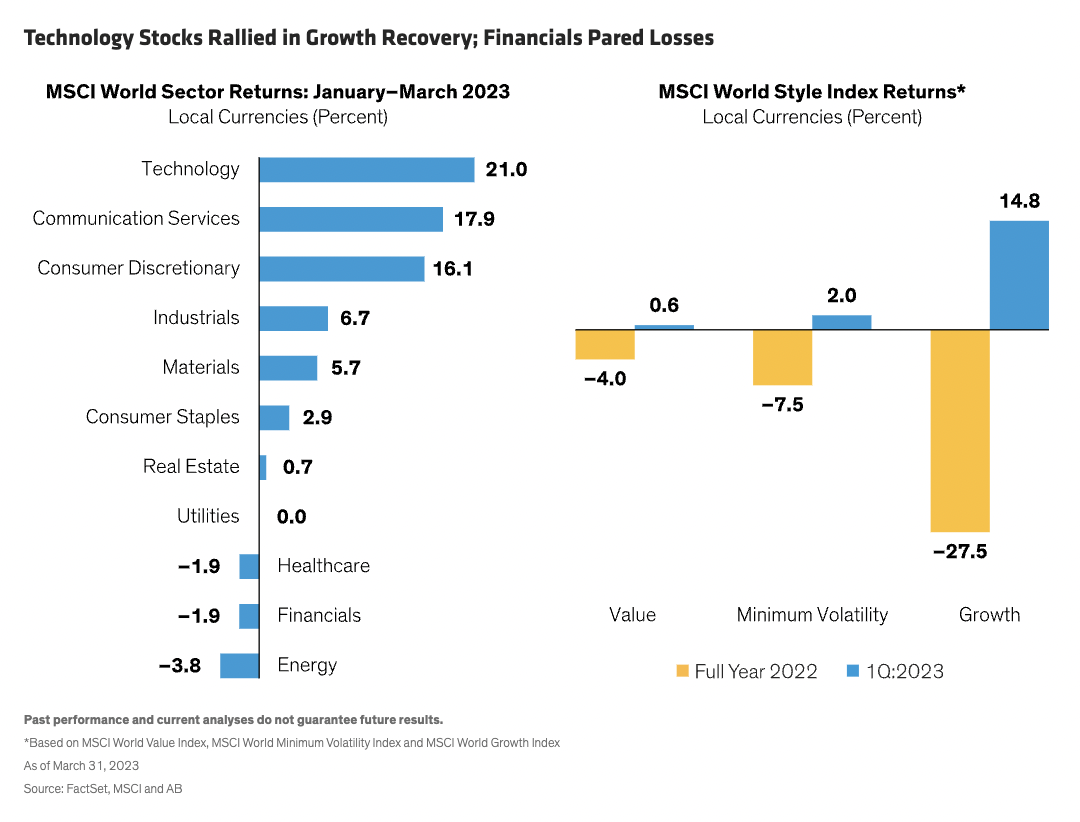

Financials were weak amid the turmoil in the banking sector while energy shares declined on falling oil prices (Display). Yet technology, communications and consumer-discretionary stocks rallied. Growth stocks outperformed value stocks in a reversal of last year’s performance patterns. Beyond equities, cryptocurrencies rebounded after a deep downturn last year.

Banking Instability Raises New Questions

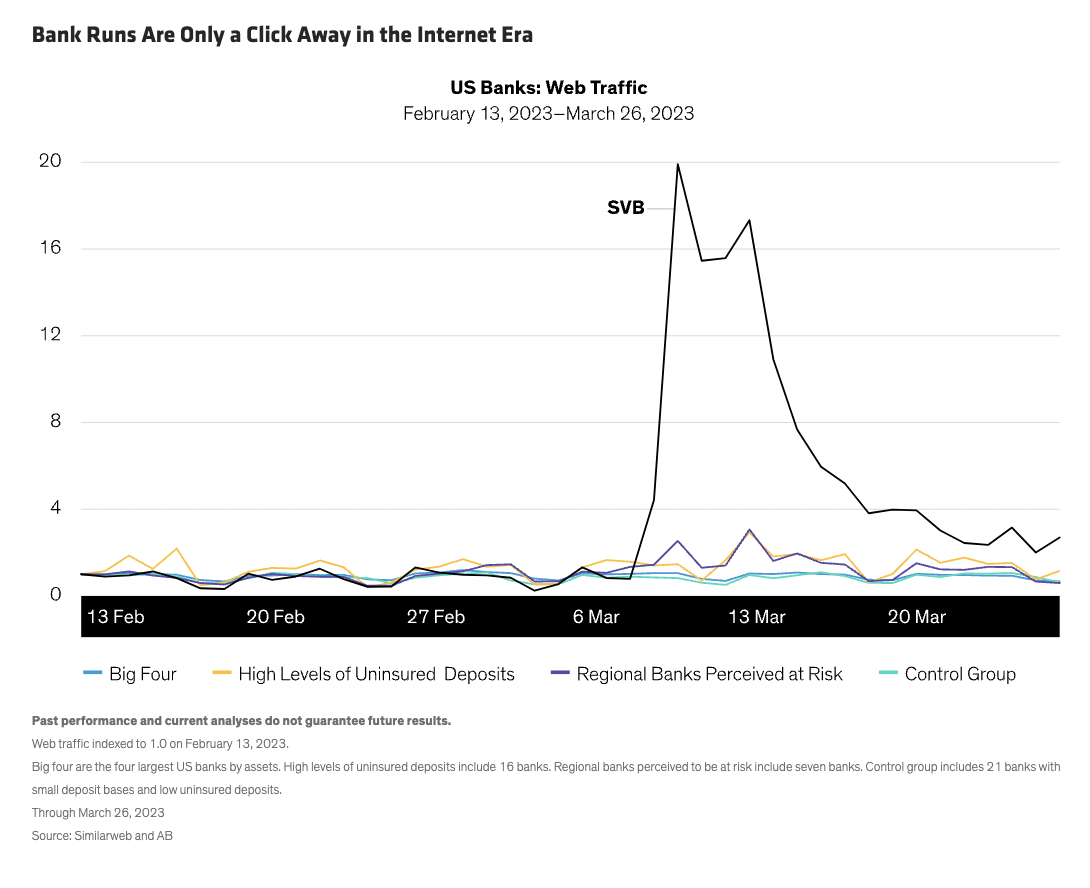

Though new challenges from rising rates were to be expected, the speed of the banking turmoil was jolting. On March 10, SVB succumbed to a run on the bank after the value of its large book of Treasury bonds shrunk because of higher rates. Panic spread to Signature Bank, a lender specializing in cryptocurrency firms, which buckled two days later. The crisis of confidence spread to Europe when Credit Suisse clients began pulling deposits after its leading investor confirmed no further capital support was forthcoming, prompting Swiss regulators to engineer a takeover by UBS on March 19. A key lesson of this past month is that in the internet era, bank runs can happen extremely quickly, as highlighted by the spike in SVB’s web traffic when withdrawals snowballed. Our research shows that despite elevated web traffic for some US banks that were perceived as relatively risky, traffic didn’t increase dramatically across the system during March (Display).

By quarter end, a financial system meltdown appears to have been averted—for now—by rapid regulatory action, including implicit deposit guarantees and bank securities lending programs to ensure adequate liquidity. The Fed remained comfortable raising rates by 25 basis points at its March meeting, anticipating tighter credit conditions but reaffirming that the banking system remained “sound and resilient, with strong capital and liquidity.” Equity markets stabilized.

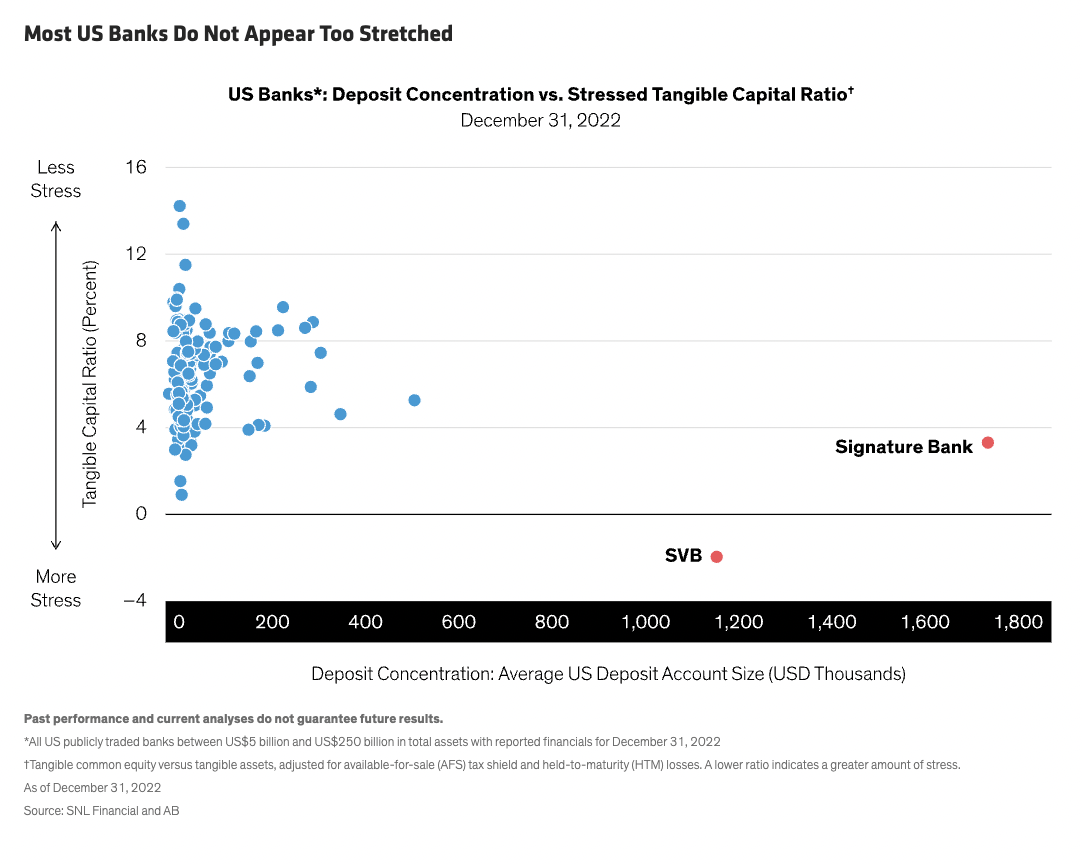

US banking fundamentals are encouraging, even as confidence remains fragile. Our research suggests most publicly traded US banks with between $5 billion and $250 billion in assets have relatively healthy capital ratios and much lower deposit concentration than SVB or Signature Bank (Display).

Still, sentiment remains uneasy. After two of the biggest bank failures in US history unfolded at lightning speed, many questions remain unanswered. What will be the knock-on effects of events in the banking sector? How will the growth or decline of deposits, potentially tighter regulation and the financial system’s ability to extend credit affect the real economy? Can private credit markets help fill the void if bank lending tightens? What other parts of the market are vulnerable to higher rates?

These questions should be at the top of any investor’s agenda in the coming months. The banking stress didn’t happen in a vacuum; like the UK liability-driven investing crisis last September, it reminded us that the ripple effects of a new interest-rate regime are still unfolding. Active investors must search for hidden linkages between companies and interest-rate exposures to surface evolving risks.

New Banking Regulation Could Hurt Profitability

Banks deserve special attention. Following recent events, banking watchdogs are expected to tighten regulation and capital requirements, which could make banks safer, but also likely less profitable. Stronger lenders that are furthest from the epicenter of the crisis should be best positioned to navigate ongoing volatility. Some may benefit from a flight to quality, as depositors move funds from smaller, regional lenders to systemically important giants with resilient businesses that are considered “too big to fail.”

Dynamics within the banking sector will determine credit availability—a key issue for the economy. In the US, regional banks are the largest credit providers to smaller businesses and commercial real estate, so as deposits shift toward larger banks and money-market funds, capital may become scarce. This could slow the wider economy, challenging industries already struggling with higher rates and post-pandemic changes, like commercial real estate, where occupancy rates remain low.

Evaluating Rate Pressures Across Sectors

While banks are systemically important to economic activity, financial stocks only comprise about 13% of the S&P 500 and 15% of the MSCI World. The moral of the recent episodes is not simply that banks were undercapitalized. Rather, any business that relies on financing and faces mark-to-market risk could be vulnerable to pressures lurking beneath the surface.

Balance-sheet and financing stress is always a potential hazard for any company. Yet in a world where interest rates have quickly risen to levels not seen in years, these risks have become more acute. For many companies, current liabilities were taken on in a dramatically different interest-rate regime, so their financial structures could suddenly become unsound.

As a result, investors must closely examine every company’s exposure to the financing ecosystem—and determine whether a balance sheet is vulnerable to the risk of higher rates. Exposure through association is another focus; we need to know whether a company is in an industry that is likely to experience significant defaults, and how this could affect the business.

Higher funding costs will make life more difficult for companies that rely on debt financing as part of their business model. Companies with too much short-term debt on their balance sheets could be especially jeopardized by higher rates. Investors must evaluate the dynamic of rising financing costs and tougher business conditions in a slowdown or recession on a company-by-company basis. We believe this will be the most critical component to identifying susceptible businesses or, in contrast, developing conviction in long-term investment opportunities.

Alongside company-specific issues, investors must also keep an eye on broader market implications of recent events. For example, investors who have been spooked by the banking failures may want more liquidity in their allocations. And in recent years, some investors have increased their holdings in private assets. But if they struggle to sell the private assets, they may have to sell public equities instead, which could create downward pressure on stocks.

Three Broad Lessons for Investors

As the new quarter begins, we think equity investors should internalize and apply three broad lessons from the banking stress to portfolios and allocations.

First, prepare for tighter lending conditions and higher costs of capital by making sure that your portfolios are focused on quality, cash-generating companies that aren’t overly reliant on refinancing. Second, be wary of private markets, which may simply mask underlying and unrecognized losses; public equities offer transparency and liquidity that should be prized in this environment. Finally, don’t panic when volatility strikes—remember that after a very bumpy ride, markets ended the first quarter up. Equity strategies with a long-term focus and a disciplined approach to valuations can tackle evolving risks with conviction—and give investors the confidence to stay the course, come what may.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

© AllianceBernstein

Read more commentaries by AllianceBernstein