China’s domestically driven economic growth has not yet translated to Emerging Market stock performance, which has tended to have been weighed down by international political tensions.

Although we maintain a positive view on developed international stock market performance this year, emerging market (EM) stocks continue to be a tougher call given their heavy exposure to China. Yet, EM stock market performance could improve later in the year if U.S.-China tensions begin to cool.

Back to BRIC era

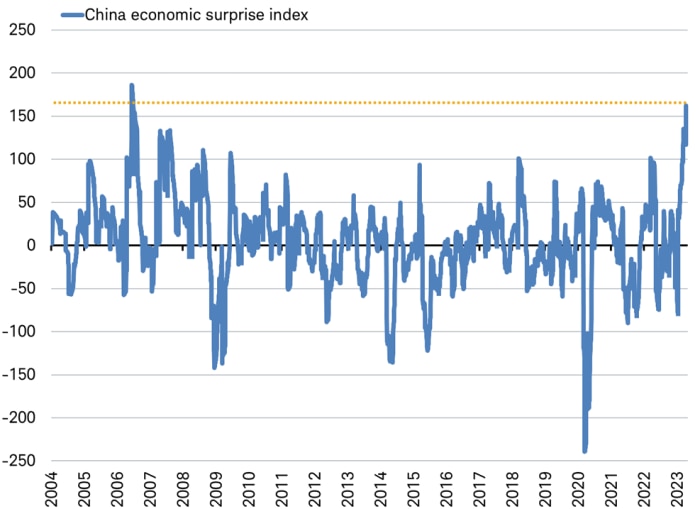

China’s economic data once again exceeded expectations last week. To put it in perspective, the data has been so much stronger than economist forecasts that the positive surprises are the highest since 2006, a year that marked the end of the BRIC (Brazil, Russia, India and China) era of booming growth.

Not since the end of the BRIC era has China’s data come in so far ahead of forecasts

Source: Charles Schwab, Bloomberg data as of 4/22/2023.

According to the National Bureau of Statistics of China:

- China’s GDP growth picked up from a pace of just 0.6% in the fourth quarter to 2.2% in the first quarter. If it were reported like U.S. GDP, that is nearly 9% at an annualized rate.

- March data showed retail sales were up 10.6% following a 3.5% rise in the January-February period. Notably, auto sales increased 11.5%, swinging from a -9.4% drop in January-February.

- Property sales swung to a 0.1% gain in March from a 3.6% decline.

- A rebound in the services helped push down the urban unemployment rate to 5.3% in March from 5.6% in February.

Also, the General Administration of Customs of China reported export growth delivered a major upside surprise in March, probably due to backlogs of orders finally getting cleared out.

It isn’t just the official data that points to a powerful rebound in China. Our alternative measures are also showing a surge in growth: EPA air pollution tests by U.S. consulates in China (an indicator of manufacturing activity and road travel), air travel to and from China reported by international carriers, China’s crude oil imports, and earnings reports on sales in China from global companies like LVMH and Hermes.

More to come

Leading indicators point to China’s economic recovery continuing to gather strength over the coming months. Private-sector credit growth accelerated further in March. Real growth in nationwide per-capita income accelerated to 3.8% in the first quarter from 2.3% in the fourth quarter. A tighter job market may continue to lift wages and drive further improvement in household income growth.

Consumer sentiment has improved but remains below pre-COVID levels, indicating opportunity for further thawing. The next phase of recovery is likely a gradual return to underlying growth as consumers get more distance from the zero-COVID days, jobs and income prospects improve and confidence recovers. We will be watching China’s national Golden Week holiday, which takes place in early May, for a potential boost in both travel and spending.

Tensions hit stocks

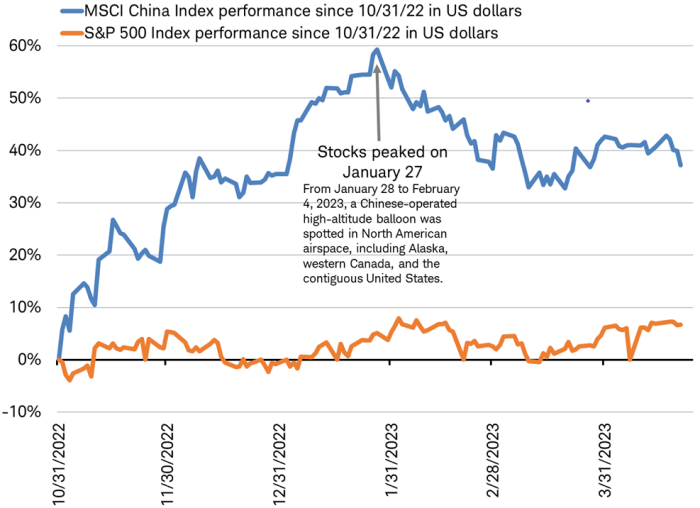

Geopolitical tensions seemed to have had little impact on China’s domestically driven economic growth. But they did appear to weigh on China’s stocks. Despite the strong and better-than-expected economic performance, China’s stock market fell 14% after the spy balloon controversy erupted in early February. That slump disrupted a 60% three month rebound from the end of October until this year’s peak on January 27.

China’s stock market momentum burst by a balloon

Source: Charles Schwab, Bloomberg data as of 4/22/2023.

Indexes are unmanaged, do not incur management fees, costs and expenses (or "transaction fees or other related expenses"), and cannot be invested in directly. Past performance is no guarantee of future results.

Next flare up

The next potential flare up in U.S.-China tensions could come within a month. The Biden administration may announce its executive order tracking and restricting outbound investments in China in critical technologies (in areas of semiconductors, quantum computing and artificial intelligence) as it seeks endorsement from members at the May 19 G7 Summit (though no members are expected to join in the restrictions). Given their narrow focus, these restrictions are expected to have limited effects on most U.S. businesses, but they could likely further impede China's progress in developing next-generation technologies. Although, tech stocks in the U.S. and other countries could be impacted should China seek to retaliate in the targeted industries.

- On March 31, the Cybersecurity Administration of China announced a review of U.S. memory-chip maker Micron. The CAC, a Communist Party-controlled organization, has never investigated a foreign company before, but may be motivated by Micron’s lobby activities in Washington for semiconductor export controls. This activity could encourage Micron’s Chinese customers to shift business to Korean rivals like Samsung and SK Hynix.

- China has asserted its regulatory authority to approve some cross-border mergers on the grounds that market concentration inside China could be affected. For example, U.S. semiconductor firms with M&A deals in front of Chinese regulators include Intel’s plan to take over Israel’s Tower Semiconductor and MaxLinear’s acquisition of Taiwan’s Silicon Motion. Both deals may see retaliatory delays in China.

- Another potential risk is any restriction placed on exports of rare-earth processing and magnet technologies, where China has a dominant global position. If put in place, these restrictions could hurt Japanese rare-earth magnet makers and their U.S. customers using them to make advanced commercial and military technology including electric vehicles and submarines.

It is important to distinguish between any potential retaliation by China directed at the tech industries targeted by the Biden Administration’s forthcoming executive order and China’s open door to U.S. firms in other sectors. For example, in the last few months several U.S. asset managers received final approval from regulators in China to start selling mutual funds and begin directly managing money for individual Chinese investors. And Tesla is expanding operations in China with a large battery plant.

There is also the potential for a Chinese consumer boycott of American-branded products, such as cars, due to further escalation of U.S.-China tensions. It’s happened several times before. U.S. auto sales in China tumbled 28% over a nine-month period after President Trump announced tariffs on Chinese goods in 2018. And a year earlier, Chinese consumers shunned Korea’s Hyundai and Kia vehicles in a political spat over the installation of U.S.-made defense missiles in South Korea, sending sales plunging by a third. Any escalation of tensions could see GM lose market share to Toyota, or Tesla to increase exports from its Shanghai plant to reduce inventory from slower domestic demand. According to company filings, China contributes just under 40% of GM’s total vehicle sales (2.3M units in China compared with 2.27M in the U.S. for 2022) and over 20% of Tesla’s revenue (18.1B USD in China compared to total revenue of 81.5B for 2022), there is a potentially large impact to any change in Chinese consumer tastes.

Tensions may cool later

While China’s economic growth is likely to remain strong, U.S.-China tensions are unlikely to significantly lower in the near-term. But looking out past the potential flare up in May, tensions could begin to cool, lifting the heavy weight on Chinese and EM stocks.

We are closely watching for signs that the U.S and China are ready to resume high-level interaction with a call between Presidents Biden and Xi and a delayed trip to China by Secretary of State Blinken, Treasury Secretary Yellen, and Commerce Secretary Raimondo. U.S. officials want to forge relationships with a largely new economic team in China after the turnover at the Two Sessions meeting earlier this year. Some positive signs include Biden administration working to limit the fallout from President Tsai’s recent visit to the U.S. and Treasury Secretary Yellen’s speech on China last week defending the Biden administration’s efforts to “de-risk” critical supply chains from China and to boost strategic competition but advocating for the need for continued bilateral engagement with China.

The potential for cooling of tensions later in the year as diplomacy begins to work may help stocks to begin to reflect the impact of the growing economy on profits for Chinese companies, which could benefit EM stocks.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

© Charles Schwab

Read more commentaries by Charles Schwab