The COVID-19 pandemic upended the way we live and work by creating secular changes and accelerating trends that were already afoot. For investors in commercial real estate, the results have been mixed.

The pandemic hurt small retailers by hastening the transition to digital commerce and emptied office buildings by turning living rooms into workspace. But it also fueled a warehouse building boom and unleashed a torrent of pent-up travel-and-leisure spending when economies reopened, underscoring the diversity of commercial real estate.

Recent turmoil in the banking industry has renewed concerns that the crosswinds buffeting commercial real estate could turn into headwinds. Of particular concern are midsized and regional banks, which purchase commercial mortgage-backed securities (CMBS) and are active commercial real estate lenders. A pullback in lending by regional banks could create a credit crunch that would have a negative impact on real estate valuations.

There’s no doubting the many challenges facing commercial real estate, but we believe the issues afflicting banks are largely idiosyncratic, rather than systemic. Moreover, the commercial mortgage market is too diverse to be painted with the same brush—fundamentals vary widely by property type, location and quality. For investors, conducting thoughtful due diligence and picking the right spots has never been more important.

With Credit Tightening, Quality Matters

Mortgage-backed securities are an important component of commercial real estate lending, comprising more than 13% of commercial and multifamily mortgage debt outstanding. CMBS are made up of mortgages that finance the purchase of hotels, office buildings, apartment buildings and other commercial property.

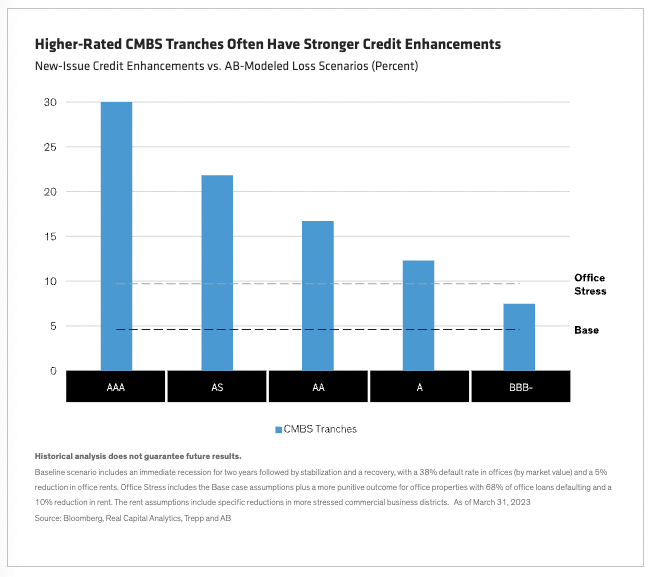

To create CMBS, individual mortgage loans are pooled and securitized into rated securities and then divided into tranches according to credit quality. At the high end are securities rated AAA with relatively low credit risk. These upper tranches often feature credit enhancements that cushion investors from potential losses, while saddling investors farther down the credit spectrum with the lion’s share of credit risk in exchange for higher yields (Display).

A second kind of CMBS is created from a single loan, collateralized by a single property or cross-collateralized by multiple properties in a single-asset single-borrower (SASB) deal—its risk is similarly divided into rated traches.

In the current environment, we believe investors should focus on higher-quality tranches to protect against downside scenarios, although we also see select opportunities to purchase lower-rated securities with favorable risk/return profiles.

Here, some historical context is in order: Even during the worst of the global financial crisis, which saw a crisis of confidence in mortgage-backed securities, AAA-rated CMBS with at least 20% credit enhancements didn’t take losses, and the credit enhancements have increased since then.

Know Your Vintage: Newer Isn’t Always Better

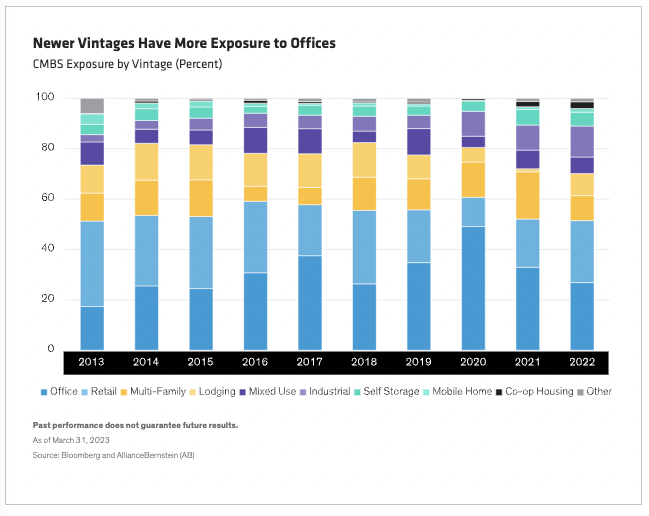

It’s also important for investors to consider when the securities were issued. More seasoned CMBS vintages—particularly those issued between 2014–2018—have benefited from property price appreciation and higher current credit enhancements.

By contrast, the loans underlying newer-vintage bonds have more exposure to struggling office properties (Display). They’re also more difficult to refinance and have seen little to no price appreciation in underlying properties. For these reasons, it’s important for investors in newer-dated CMBS to stick with the highest-quality tranches.

Assessing Different Property Types

Although it’s tempting to lump commercial real estate together, the commercial real estate market is complex, and some property types are better positioned than others.

-

Office: The office segment remains our highest concern as the demand for office space has fallen, particularly within the technology sector. Although recent-vintage CMBS have more exposure to offices, this risk is partially mitigated by longer-term leases, which provide more leeway to re-tenant space. This sets the stage for what we believe will be a gradual increase in delinquencies as tenant re-leasing needs change once leases expire. Older-vintage CMBS, on the other hand, have benefited from deleveraging and less exposure to offices.

-

Retail, Regional Malls: Malls with lower sales per square foot—particularly those in tertiary markets—remain a concern. Many owners are reluctant to invest in property improvements unless they see a commensurate return on their capital. Given credit constraints, we are wary of legacy CMBS loans backed by lower-quality malls and anticipate further loan extensions and some defaults. By contrast, better-quality properties—particularly those in growing markets that have been creative in catering to evolving consumer tastes—have the potential to thrive.

-

Retail, Non-malls: Non-mall retail has proven to be surprisingly resilient, benefiting from strong consumer spending and nondiscretionary outlays. Many retailers have also been able to refinance their brick-and-mortar assets to keep financing costs in check.

-

Lodging: Corporate cost cutting and reduced business travel have put the squeeze on full-service hotels that cater primarily to business travelers. Limited-service hotels, on the other hand, have benefited from increased domestic and leisure travel. Limited-service hotels also have lower break-even costs, which provide additional financial cushion.

-

Multi-family: A housing supply shortage, high single-family home prices and relatively high mortgage rates have been catalysts for multi-family housing. Increased labor, material and financing costs could slow construction in the coming years, which further supports solid demand for existing housing stock. As a result, we expect slow but steady growth in rents to support loan performance.

-

Industrial: Warehouses and data centers have been among the biggest winners thanks to the growth of online retailing and cloud computing. Although rents have risen steadily, we expect growth in this segment to slow if the economy weakens and larger tenants pull back on new leases.

Choppiness Likely, but High-Quality Credits Should Fare Better

We expect commercial real estate to face continued challenges as cap rates (a function of net operating income and property values) rise and interest rates stay elevated. As a result, we expect to see a gradual uptick in delinquencies over the course of the year. However, we expect most credit impairments will be contained to lower-rated CMBS tranches and more troubled segments like office buildings.

For the CMBS market to function smoothly, lending activity must remain robust. Although we anticipate a more restrictive lending environment, we expect lenders to work closely with high-quality borrowers to extend loans and avoid foreclosure. Look for institutional CMBS conduit and SASB borrowers to extract the most favorable terms from lenders.

The Federal Reserve may also consider changes that would allow banks to avoid reclassifying loans or taking reserves against potential losses if there’s a reasonable expectation of full recovery. Similar measures were successfully employed during the global financial crisis.

Investors may also benefit from positive technical factors resulting from low CMBS issuance. Reduced supply should prevent a widening in spreads, providing some measure of price support. In time, renewed confidence in mid-sized and regional banks should support the CMBS market and provide a more normalized operating market. Until then, investors should expect elevated volatility—particularly in the office segment—making the focus on credit quality all the more important.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein