Stock selection in a climate investing strategy takes more than just avoiding companies exposed to global warming risks. The process should intersect with an active search for diverse opportunities among companies helping to fight climate change, but with high-quality business models, too.

Concerns and action to stem global warming are decades in the making, although efforts have increased in recent years. The German city of Freiburg, for instance, pioneered the move to solar power in the 1980s and is quickly approaching its goal to nearly halve its greenhouse gas emissions by 2030. Freiburg’s early awareness is uncommon, however, and many economies and industries today are just waking up to climate-related risks.

Climate Risks Are High but There’s Still Time to Act

Europe experienced its second-hottest year on record in 2022; globally it was the fifth warmest. Against this backdrop, the UN’s environmental experts intensified demands to fast-track climate-fighting efforts by “every country and every sector on every timeframe.”

On a positive note, the same UN report underscored that it’s not too late. First, the widely adopted goal to limit annual rising temperatures to 1.5 degrees Celsius by 2030 is still within reach. And by mobilizing funds and sharing best practices, technology, and effective policy measures, any entity can better manage, even prevent, carbon output.

More top-down support via government initiatives is helping, too, and the incentive is clear; research shows that climate change can strain or benefit economic output to the tune of –8% to 15% annually, depending on how governments and industries respond.

At last year’s UN COP27 conference, for example, delegates agreed to establish a multinational financial backstop for loss and damage, ideally to help poorer countries recover from climate-related impact. The US Inflation Reduction Act and the pending European Green Deal include well-funded incentives to shepherd economies toward low-carbon mode. China, arguably a top greenhouse gas producer, is also on board. Its 2060 carbon-neutral framework, while addressing climate change, also reveals its vision for the country’s economic future in light of it.

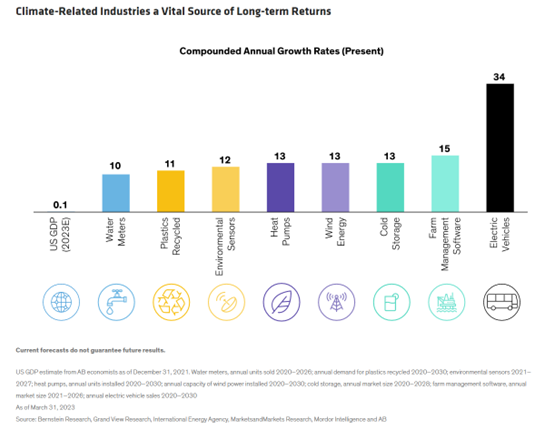

Many Industries Benefit From Climate-Related Economic Drivers

Combatting climate change goes deeper than macroeconomic policies. A growing number of industries, from electric vehicles to wind farms, are also on the front lines of a decarbonizing economy—and all are growing at a faster rate than the US economy (Display).

These are the innovative companies that will lead the way with climate-transition-specific business models, as well as products and services that enable the achievement of global decarbonization. And we expect they’ll enjoy multi-decade growth potential as a result.

Understandably, investors remain wary of today’s uncertain macro environment, mainly rising interest rates and high inflation. Clearly, these disruptors are factors in the investment selection process, too, but should be integrated right alongside climate risks—not in sequence—to find businesses likely to do well in the new economy.

Climate Solutions Are an Appealing Investment Factor

The growth potential among companies providing climate solutions is making a strong impression on investors. In 2022, for example, global investment in energy-transition products and services, such as renewable energy, electric vehicles, energy efficiency, and hydrogen, reached a record $1.1 trillion, a 31% increase from the prior year (Display). China is by far the largest contributor to the growth, accounting for about half of all investment. More importantly, the recent groundswell put energy-transition investment levels on an even keel with fossil fuels for the first time. By the end of this decade, we anticipate investment in decarbonization products will dwarf spending on fossil fuels by at least four-fold.

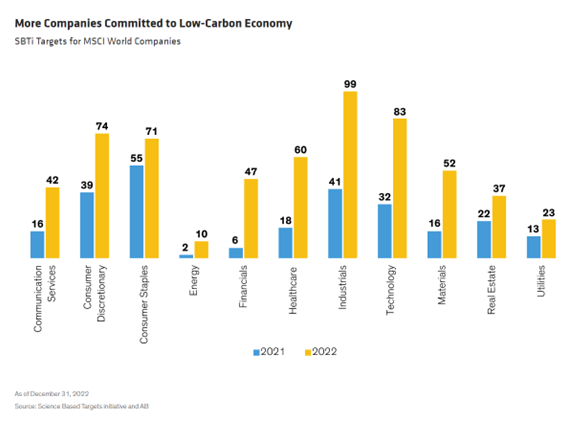

The growing commitment to global carbon-reduction goals extends well beyond climate-friendly industries. More companies than ever are signaling support for science-based greenhouse gas reduction targets, particularly in the consumer discretionary, information technology, and industrials sectors (Display).

This momentum is fostering a healthy competitiveness among innovative climate-resilient and climate-focused businesses, offering attractive growth opportunities. Companies such as AECOM, based in Dallas, Texas, offer to consult for carbon-intensive industries like transportation and construction that can help deliver aggressive emissions-reduction goals, up to 50% for most projects. Hexcel, based in Stamford, Connecticut, makes lightweight carbon fiber used in airplane construction that saves fuel and cuts airline annual greenhouse gas emissions by the tonnes. Norway-based recycling firm TOMRA continues to benefit from an expanding global commitment to reusable plastic in manufacturing, retail, and food packaging.

Climate Resilience Also Needs Strong Fundamentals

A company’s climate resiliency also stems from the quality of its business model, so investors should focus on both. Besides navigating the near-term impact of climate change, companies need to plan their long-term contribution, and profitability, in a low-carbon economy. In our view, strong balance sheets and effective governance are as important to active climate investing as other equity strategies. It’s not enough to mitigate the financial impact of climate change; companies must demonstrate solid bottom-up fundamentals and top-down vision to benefit from current and future opportunities in the transition to a decarbonized world.

The global population will swell to 10 billion by 2050, so our worldwide Freiburg moment is now. Innovation is more important than ever to improve the environment, ensure clean water and produce enough safe food. That’s why holistically integrating the risks and opportunities in today’s economy is the linchpin of an effective climate strategy. Companies that can find their niche in this massive effort will prosper, provided they can mitigate today’s risks while setting the groundwork for future profitability. Climate investment solutions should focus on both sides of that equation.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams, and are subject to revision over time.

References to specific securities are presented to illustrate the application of our investment philosophy only and are not to be considered recommendations by AB. The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for the portfolio, and it should not be assumed that investments in the securities identified were or will be profitable.

© AllianceBernstein

Read more commentaries by AllianceBernstein