The central bank likely won't have enough reason to hike rates again this cycle. In fact, we wouldn't be surprised to see one or two rate cuts later this year.

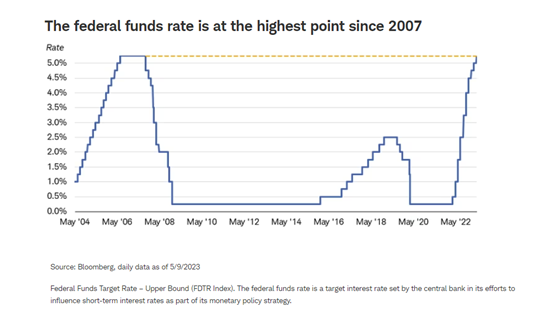

As expected, the Federal Reserve raised short-term interest rates by 25 basis points at its May 2-3 meeting. With the rate hike, the upper bound of the federal funds rate target is now 5.25%, the same level as the peak of the last cycle in 2006-2007.

In the statement released after the meeting, the Fed hinted that its aggressive rate-hiking cycle is on hold as it assesses the outlook for growth and inflation, but left the door open to further tightening, citing ongoing high inflation as its primary concern. While the Fed may not be certain about its next move, the market is pricing in the likelihood of two rate cuts of 25 basis points1 each later in the year.

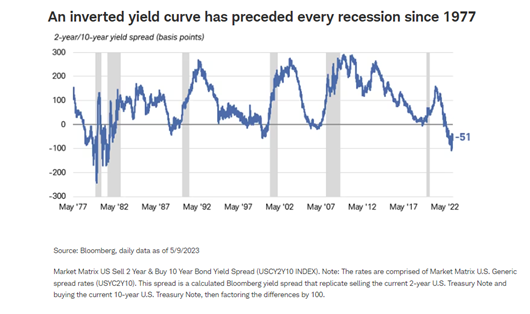

Notably, this divergence between the Fed's forecasts and the market's expectations has persisted even as the rate hikes have continued over the past few months. Consequently, the yield curve has been steeply inverted for the past nine months—a sign that investors expect lower interest rates in the future—which historically has been a fairly reliable indicator of a coming recession.

Enough already

In our view, the evidence suggests that the Fed's tightening has gone far enough to bring inflation down in the longer term. The next move will likely be a cut in rates rather than a hike. The timing is unclear, with the Fed indicating it is likely to hold rates at the current level this year, but it all depends on inflation. We would not rule out a rate cut as early as the third of fourth quarter of the year. Here are the three major reasons:

1. Lagged impact of rate hikes is starting to show softening growth and inflation. Central bankers often remark that monetary policy works with a lag, and it takes time for tighter monetary policy to bring down inflation. Recent economic indicators indicate that the effects are beginning to show up. In fact, the Fed's research staff is forecasting a "mild recession starting later this year, with a recovery over the subsequent two years." 2

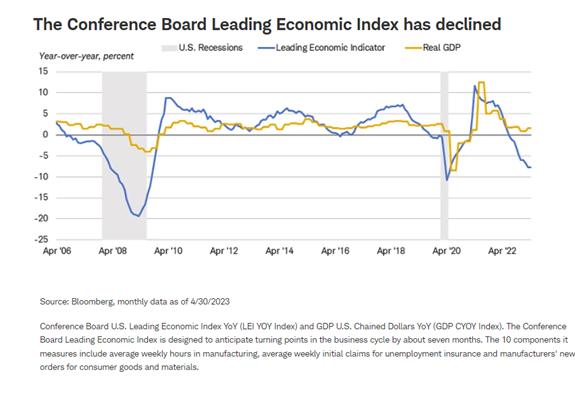

Leading indicators suggest the same. They have been falling for over a year. While the Fed has been focusing on coincident or lagging indicators, such as the unemployment rate, in setting policy, the market is looking forward. Now it looks as if the Fed is catching up.

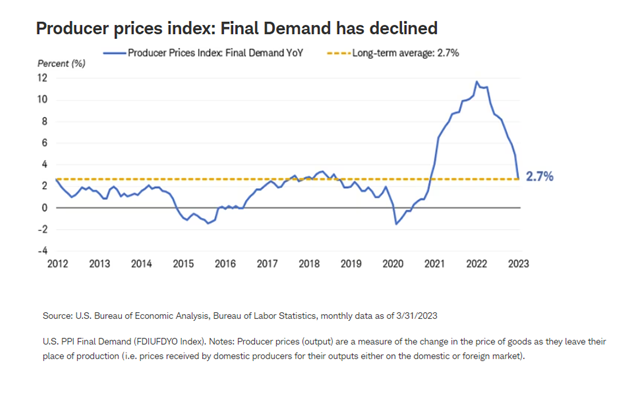

Inflation has been easing as well, especially at the wholesale level. The producer price index (PPI) has been falling sharply as the supply of goods has caught up with demand. After spiking during the pandemic, producer prices are now growing at only 2.7%, consistent with the long-term average.

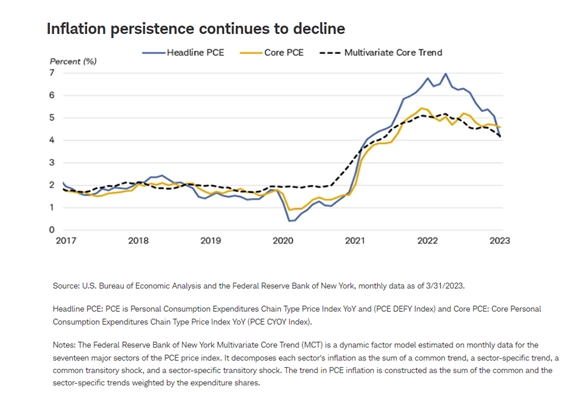

While inflation in the service sector has been slower to fall than at the wholesale level, it is receding. The New York Fed model shown below indicates that core inflation (excluding food and energy prices, which tend to swing up and down) is trending steadily lower and is lower than the more widely known core personal consumption expenditures (PCE) index.

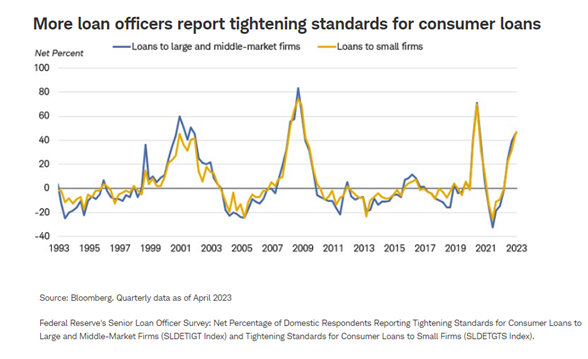

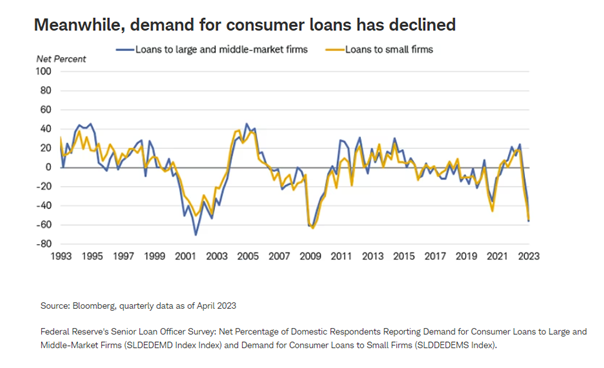

2. Credit conditions are tightening. Since monetary policy is transmitted through the financial system, the recent turmoil in the banking sector suggests that credit conditions will likely tighten further. In fact, the recent turmoil in the banking system may be a signal that policy is already too tight.

The Fed's quarterly Senior Loan Officer Opinion Survey indicates that banks were pulling back on lending even before the recent failure of several banks. Given worries about potential outflows of deposits, lenders are likely to become even more cautious. Regional banks are the major lenders to small- and medium-sized businesses as well as to the commercial real estate sector.

Credit tightening has been less evident in the corporate bond market, where yield spreads versus Treasuries are holding near long-term averages. However, in the private credit markets, there are reports of significant tightening in the availability of capital. These loans are often short-term with floating rates, resulting in sharply higher refinancing costs.

3. Debt ceiling debate. Finally, the standoff between Congress and the White House over raising the debt ceiling is likely to increase volatility in financial markets and may result in slower economic growth. While our base case is not for a default on the U.S. debt, even the threat of it is elevating volatility in the financial markets.

Yields for short-term Treasuries maturing in the next few months are elevated compared to those maturing in the third quarter, as investors shy away from the risk that the interest on T-bills could be deferred. The standoff has heightened the uncertainty about the economy. A default would risk sending short-term yields higher, while risk assets and the dollar would likely fall. This is the scenario that played out in the 2011 debt ceiling fight, which resulted in the U.S. federal government credit rating being downgraded by several rating agencies, including Standard & Poor's, to below AAA for the first time ever.

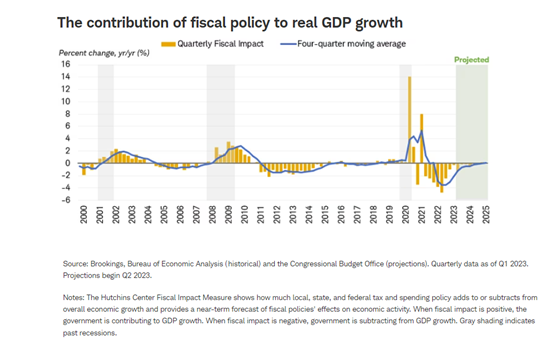

Even assuming that there is a deal that raises the debt ceiling in the near term, it looks likely that there will be wrangling over fiscal policy in the fall budget season. Fiscal policy has already moved from stimulative to restrictive. The Hutchins Center Fiscal Impact Measure estimates that fiscal tightening subtracted about 0.2% from gross domestic product (GDP) growth in Q1 2023, as transfer payments from state and local governments to households declined. Further fiscal tightening, coming on the heels of tighter monetary policy, could exacerbate a downturn.

Implications for interest rates

The combination of tightening monetary to date, the waning impact of fiscal stimulus, combined with the risks around the debt ceiling debate point to the likelihood that the Fed won't have much reason or scope to hike interest rates further in this cycle. Moreover, we wouldn't be surprised by one or two rate cuts later this year.

Given that outlook, we continue to look for intermediate- to long-term Treasury yields to remain low. They have already fallen sharply from the peak levels of late last year, but there is some scope for further decline. Consequently, we continue to suggest that investors add some duration to portfolios.

1 A basis point is one-hundredth of 1 percentage point, or 0.01%, so 25 basis points would be equal to 0.25%.

2 Source: Federal Reserve, "Minutes of the Federal Open Market Committee, March 21–22, 2023," page 6.

To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab