Although few nations have a debt ceiling similar to the U.S.', rising government debt levels are a widespread global risk that may lead to lower economic output and weaker growth.

A default or funding delay in the U.S. Treasury market, the deepest and most liquid market in the world and a central component of the global financial system would undoubtedly have global impacts. Although a last-minute debt ceiling increase may address the immediate issue in the U.S., the level of government debt is still a major concern globally. The U.S. debt ceiling showdown offers an opportunity to examine how the rest of the world is seeking to limit the amount of government debt.

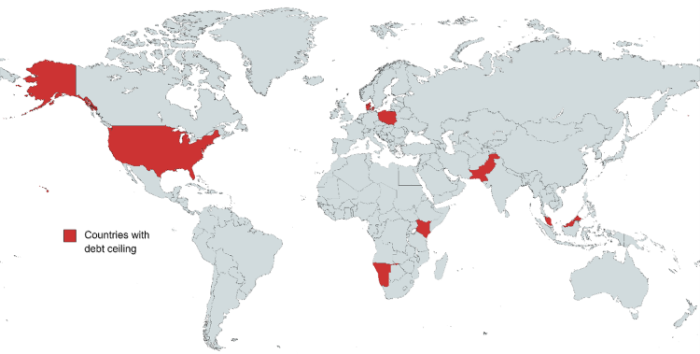

Debt ceilings are uncommon

Few nations have a debt ceiling similar to the United States, giving us no other countries to look to as a guide on the impacts of a debt-ceiling-driven crisis. After Australia abandoned its debt ceiling in 2013 after six years and four increases, only Denmark, Poland, Kenya, Malaysia, Namibia, and Pakistan currently limit the amount of government debt. Why so few? Perhaps because there is no evidence to suggest it limits spending.

Few nations have a debt ceiling

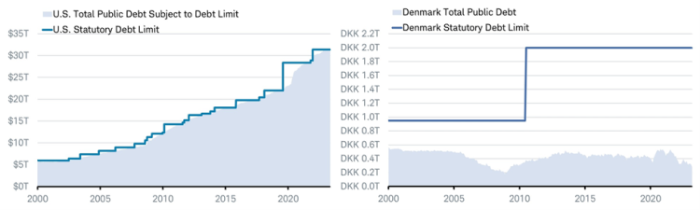

- Denmark, the only other developed country with a debt ceiling, has set its limit so much higher than the country's spending that it has not posed a constraint. Denmark's central government debt is currently only about 14% of the ceiling. Over the past 22 years, the U.S. has needed to increase the debt ceiling 22 times, while Denmark did so once but didn't need to. Denmark doubled its debt ceiling in 2010, well ahead of any risk of hitting it.

Source: Charles Schwab, created with mapchart.net as of 5/12/2023.

Low versus high debt ceilings

Source: Charles Schwab, Macrobond, Danmarks Nationalbank data as of 5/18/2023.

- Poland's constitution does not directly limit borrowing but effectively does so by capping spending at 60% of GDP. Nevertheless, in 2021, Poland's state auditor found that the government used "unprecedented mechanisms" to spend more than rules allow.

- Kenya is in the process of making the debt limit a percentage of GDP (55%) rather than a static number, according to President William Ruto's office. Last summer, Parliament increased the limit from nine trillion Kenyan shillings to 10 trillion with little political opposition.

- Malaysia's debt limit of 60% of GDP is voluntarily imposed by the Ministry of Finance and not governed by law, nor is the approval of Parliament required to raise it. The government can simply revise the limit when needed, as they have in each of the past three years.

- Namibia's debt ceiling is set at 35% of GDP by the Sovereign Debt Management Strategy of 2005 but has been above that level for years with no required actions to lower it. It climbed to 72% of GDP in 2021, the latest year data is available.

- Pakistan's Fiscal Responsibility and Debt Limitation Act of 2005 limits government debt to 60% of GDP but does not stipulate any actions for breaching that limit. Pakistan's debt has continually been over the limit with debt-to-GDP currently at 75%.

Australian policymakers repealed their debt ceiling in 2013. That was only six years after the Act was passed that created it. During those six years, they were forced to increase it four times from A$75 billion to A$500 billion.

Europe's debt plan

Like the U.S.'s debt ceiling deliberations, the European Union's new proposal to limit debt will likely be subject to heated debate, but unlike the U.S., is not a high-stakes battle at risk of prompting a default.

After the austerity in the form of tight debt and budget controls in the aftermath of the European Debt Crisis a decade ago, Europe's former debt and budget rules were suspended during the pandemic and war in Ukraine to allow nations to increase public spending to address the risks. On April 26, the European Commission unveiled a new proposal to limit the government debt and fiscal budget deficit limits for member nations. EU governments are now debating the new rules with the goal of reaching an agreement to impose a flexible debt ceiling by the end of 2023.

- Debt ceiling: If a government's debt is in excess of 60% of GDP, it must present a plan to lower it over four years (that could extend to seven years if it's implementing reforms that increase fiscal sustainability and encourage growth, invests in green and digital transitions or in security and defense). This contrasts with the rigid former rule where governments must cut debt by 1/20th of the excess above 60% of GDP every year.

- Deficit limit: If a government's budget deficit exceeds 3% of GDP, it will have to cut its deficit by 0.5% of GDP every year until it is below the limit (that could extend to seven years for the same reasons as apply to the debt limit). This offers much more flexibility than the former rule which mandated that government budget deficits must not exceed 3% of GDP.

Like the U.S. debt ceiling deliberations, the EU's proposal will likely be subject to heated debate which could delay the implementation of the new rules. Germany and the Netherlands have expressed skepticism that the proposed rules are too lenient and subject to politicization with a shift from universal rules to customized debt-reduction plans with a subjective approval process. In contrast, France and Italy see the proposals as an improvement on the bloc's current one-size-fits-all approach to limits. France, Italy, Spain, and Belgium will likely exceed the limits, per data from Eurostat.

The conflict between reining in overall spending while ramping it up in strategic areas vital to the security and sustainability of the EU (defense and energy), means a flexible set of rules are likely. This would avoid anything like the high-stakes risks seen with the U.S. debt ceiling showdown. The resulting lack of strict budget cuts and the greater flexibility on fiscal adjustments also means the new rules are not likely to lead to the austerity of the 2010s when forced budget surpluses acted as a major drag on Europe's economic and earnings growth. It is possible that greater fiscal integration may also result from the negotiations, increasing the use of collective EU debt to fund EU-wide projects such as green energy transitions, industrial subsidies, and joint defense procurements.

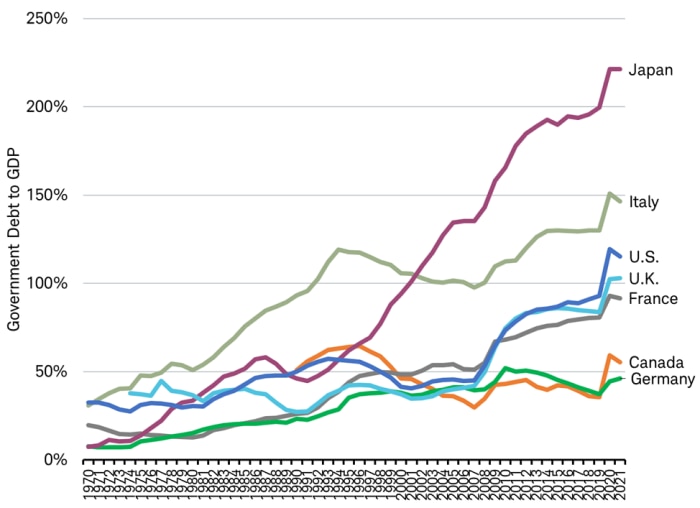

Japan has no limit

While debt ceilings may have been proven ineffective at capping debt growth, there are also risks to not having any limits on debt growth, as Japan has demonstrated. As of December 2022, Japan's government debt is 263% of GDP, double that of the U.S. (123%), and the highest of any developed nation.

Rising debt to GDP surged further in response to the pandemic

Source: Charles Schwab, IMF data as of 5/15/2023

To help finance this debt, the Bank of Japan (BOJ) has bought half (52%) of all Japanese government bonds, known as JGBs, more than double the share of U.S. government debt owned by the U.S. Federal Reserve (20%).

The unlimited growth in debt financed with low-interest rates has weighed on the value of Japan's currency. The yen has fallen nearly 25% against the dollar since the end of 2020 when the Bank's self-imposed ceiling on purchases JGBs was lifted in response to the pandemic. This effect on its currency may eventually act as a market-imposed debt limit on Japan, but since Japan has a high savings rate and can finance its debt without relying on foreign investment, it illustrates how high government debt can go when financed domestically.

Borrowing from the future

The efforts to contain the growth of debt are important to investors. Fundamentally, debt borrows future resources by spending tomorrow's income today. Debt can be a positive for future growth when it is used to invest in areas that may drive better productivity, but when borrowing more to fund current consumption, it can be a drag on future growth.

Global government debt levels were already at record highs before the pandemic and then surged further. Economists at the International Monetary Fund looked at debt surges in 190 countries between 1970 and 2020 and showed that debt surges tend to be followed by weaker economic growth and persistently lower output. The risk posed by high levels of debt isn't wiped away by the passing of yet another debt ceiling increase in the U.S., despite the near-term relief it may bring.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Investing involves risk including loss of principal. International investments are subject to additional risks such as currency fluctuation, geopolitical risk, and the potential for illiquid markets. Investing in emerging markets may accentuate this risk.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Past performance is no guarantee of future results.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab