The drama characterizing the first half of 2023 may abate, with potentially milder returns for investors due to the effects of the Cardboard Box Recession.

Global stocks' double-digit gains may make it easy to forget the drama in the first half of 2023 that included spy balloons, failed banks, hiked interest rates, and a debt ceiling showdown. The second half may see less drama, but milder returns for investors as the Cardboard Box Recession broadens. We will sum up what we learned in the first half and what we believe the second half of the year may hold for investors.

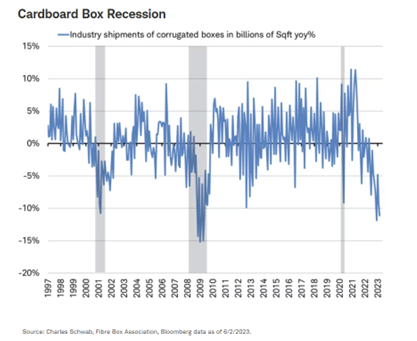

The Cardboard Box Recession

During the typical global recession, all areas of the economy (like manufacturing, services, retail, construction, and trade) tend to turn down around the same time. Yet, over much of the past year, only manufacturing and trade seem to be in a global recession, according to indicators such as industrial production, worldwide trade volumes, job growth by industry, surveys of purchasing managers at manufacturing companies, and many others.

We're referring to this phenomenon as a Cardboard Box Recession because items that are made (manufacturing) and shipped (trade) tend to go in a box. Demand for corrugated liner board, what most cardboard boxes are made from, has fallen similar to past recessions, as per data from the Fibre Box Association. The latest drop is reminiscent of the price behavior during those shaded periods on the chart below denoting global recessions. Note that while the drop in 2012 on the chart isn't matched with a global recession, both Europe and Japan did suffer recessions at that time, softening global demand for boxes.

In contrast, services industries, which make up the largest share of output among developed economies, have continued to grow. The global services Purchasing Managers' Index (PMI) remains well above 50–the threshold between contraction and growth. As consumers have turned to shop for experiences over goods, travel, and entertainment remain in high demand. As an example, the airline industry's main organization, the International Air Transport Association, said on June 5th that it is doubling its estimate for global net profit in 2023 on the surge in flying in North America and Europe.

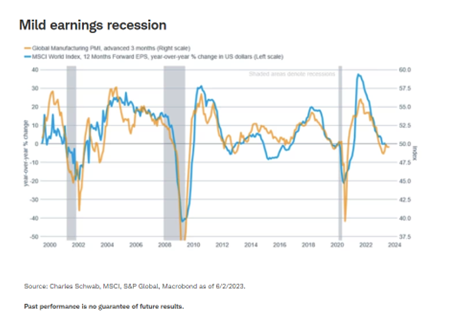

Earnings recession

Evidence of the Cardboard Box Recession suggests the mild recession in corporate earnings may continue. Historically, the global manufacturing PMI leads earnings growth for global companies by a quarter. It currently continues to point to low-to-mid single-digit year-over-year percentage declines for earnings per share. While falling earnings are never great news, the drop is barely noticeable when compared with prior recessions where they fell 20% or more.

Looking further ahead, the gap between earnings expectations for cardboard box-type industries and services industries is double-digit. Over the coming year, the FactSet-tracked consensus of analysts' earnings growth forecasts for companies in manufacturing industries is +3.8% versus +14.9% for services. While these forecasts by analysts often tend to be overly optimistic, the wide gap between them highlights how the economists and analysts are aligned on the nature of the current economic environment.

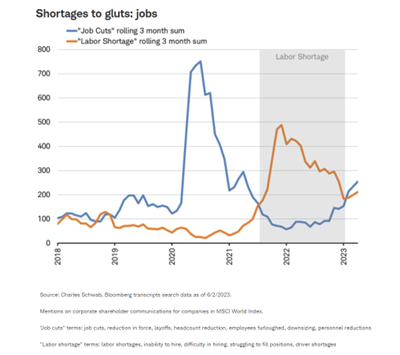

Shortages to gluts

The change from shortages to gluts in the global market for goods that took place in mid-2022 may now be shifting to the global labor market of 2023. Company communications on earnings calls and shareholder presentations reveal a rising trend of mentions of job cuts (including phrases like reduction in force, layoffs, headcount reduction, employees furloughed, downsizing, and personnel reductions) along with a falling trend in mentions of labor shortages (including phrases like labor shortages, inability to hire, difficulty in hiring, struggling to fill positions, driver shortages).

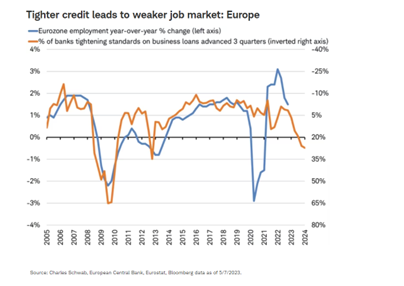

Lending conditions may also contribute to a weaker job outlook. There is a clear and intuitive leading relationship between banks' lending standards and job growth. The magnitude of the recent tightening in lending standards from banks in the U.S. and Europe points to a potential shift from job growth to job contraction in the coming quarters.

Job growth in cardboard box-type industries has been weak this year in comparison with services:

- U.S.: This past Friday's U.S. jobs report showed manufacturing jobs fell by -2,000 while overall non-farm jobs rose by +339,000.

- Canada: May data for Canada isn't available yet, but manufacturing jobs fell a total of -3,300 in March and April combined while service-producing jobs rose by +111,000.

- Germany: A breakdown of job growth by industry is only done on a quarterly basis in Europe, but in the first quarter Germany saw 13,000 net new manufacturing jobs compared with 155,000 net new jobs in the overall economy.

This weakness in manufacturing job growth could begin to spread into services industries in the second half of the year.

Inflation

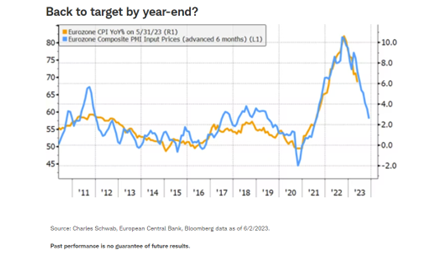

The Cardboard Box Recession may be good news for inflation. The output prices component of the manufacturing PMI, which signals the trend in prices charged by manufacturers, has consistently forecast six months beforehand both the direction and level of inflation in Europe, the United States, and the United Kingdom. Europe's latest PMI price index shows inflation may track from the current 6% to near 2% during the next six months. Inflation might just continue to recede as fast as it rose.

If inflation reaches its target of 2%, the European Central Bank may pause rate hikes this summer. This could mean a shift away from all the markets' attention revolving around central bank actions in the first half of the year.

Out-of-the-box ideas

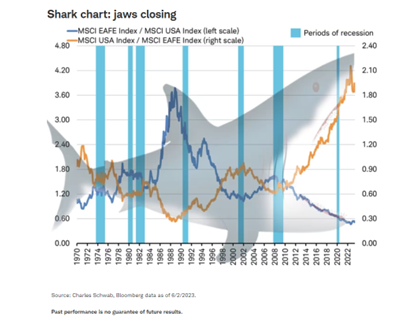

In our 2023 Outlook, we stated that international stocks were likely to outperform again in 2023, as the leaders of the last cycle tend to reverse and fall the most during the bear market while the recovery and next cycle tend to see new leaders. The chart below shows what stock market shark attacks look like using the relative performance of U.S. and international stock indexes. The lines are just the ratio of one index divided by the other. When the blue line is rising, international stocks are outperforming U.S. stocks. When the orange line is rising, U.S. stocks are outperforming international stocks. They are mirror images of each other.

There were numerous baby shark attacks around recessions in the 1970s and 2000s. But, in the late 1980s, the jaws were gaping wide after about a decade of international stock market outperformance. As U.S. stocks began to outperform, the enormous jaws began to close and took a big bite out of the portfolio of investors who hadn't rebalanced away from international stocks. Now, the shark's massive jaws may be closed once again, having been extending for more than 10 years. This time, markets appear to be prepared to take a bite out of the relative performance of the U.S. stock market as international stocks likely take their turn to outperform.

No one knows for sure if we have seen the peak of U.S. stock market outperformance relative to international stocks; the shark jaws could open still wider after appearing to begin to bite down with international stocks' outperformance. May's surge in a small group of U.S.-based artificial intelligence (A.I.) stocks helped the U.S. erode the international outperformance in the first half of the year. U.S. technology stocks outperformed the S&P 500 by the largest margin since November 2002 in the month of May. While recognizing that a bubble in A.I. stocks could further boost U.S. stocks on a relative basis, we still find international stocks attractive in the second half of 2023, bolstered by more attractive valuations and faster earnings growth.

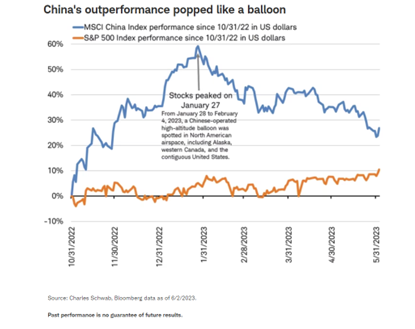

We are still neutral on the performance of emerging-market stocks this year, which seems to remain dependent upon U.S.-China tensions as much as China's continued economic recovery, as Chinese stocks are the largest weight in the MSCI EM Index, at over 30%. Geopolitical tensions seemed to have had a negligible impact on China's domestically driven economic growth, but they did appear to weigh on China's stocks. Despite the strong and better-than-expected economic performance, China's stock market fell after the spy balloon controversy erupted in early February. That slump disrupted a 60% three-month rebound from the end of October until this year's peak on January 27.

Leaders on both sides have signaled that U.S.-China relations may soon thaw as U.S. policymakers schedule meetings with their counterparts in China. In fact, the Financial Times reported that CIA Director Burns made a previously undisclosed trip to China last month, meeting with his counterparts and emphasizing "the importance of maintaining open lines of communication." But tensions have the potential to remain strained in the near term with a Biden administration executive order to restrict U.S. outbound investment into China possible in the coming weeks so the transition may not be smooth. The momentum in China's economy slowed after the initial post-zero-COVID rebound, but more aggressive stimulus may be forthcoming to reinvigorate the recovery.

Boxing it up

The second half of 2023 may hold the potential for fewer surprises, with a debt ceiling deal in place until early 2025, global central banks moving toward a pause on rates, bank stress stabilizing, and signs of potential U.S.-China tensions cooling. The pause in international stock market leadership in May could resume in the second half of the year. Yet, the global stock markets' double-digit returns in the first half may already reflect expectations of an end to the Cardboard Box Recession. Stocks may have trouble matching those gains in the second half if weakness spreads into services industries as both inflation and job growth ease.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Diversification and rebalancing strategies do not ensure a profit and cannot protect against losses in a declining market. Rebalancing may cause investors to incur transaction costs and, when a non-retirement account is rebalanced, taxable events may be created that may affect your tax liability.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this or other topics, please check out our most recent white papers.

© Charles Schwab

Read more commentaries by Charles Schwab