Schwab Market Perspective: Different Speeds

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSometimes it feels like the economy and markets are on different tracks. Although leading economic indicators have been flashing recessionary signals, the S&P 500® index has plowed higher. Manufacturing activity is weak while services is resilient. The Federal Reserve declined to raise short-term rates at its June meeting for the first time in more than a year—but made it clear the door is still open to future rate hikes. Meanwhile, Europe is in a recession and a bull market at the same time.

As we enter the second half of the year, clarity remains elusive. We see positive signs ahead, but also potential risks.

U.S. stocks and economy: Bifurcations

Approaching the end of the first half of the year hasn't yielded much economic clarity. There remains a relatively strong bifurcation between certain segments of the economy—be it manufacturing (weaker) and services (resilient), or leading economic indicators (weaker) and their coincident peers (resilient), which has mostly been reflected in the stock market.

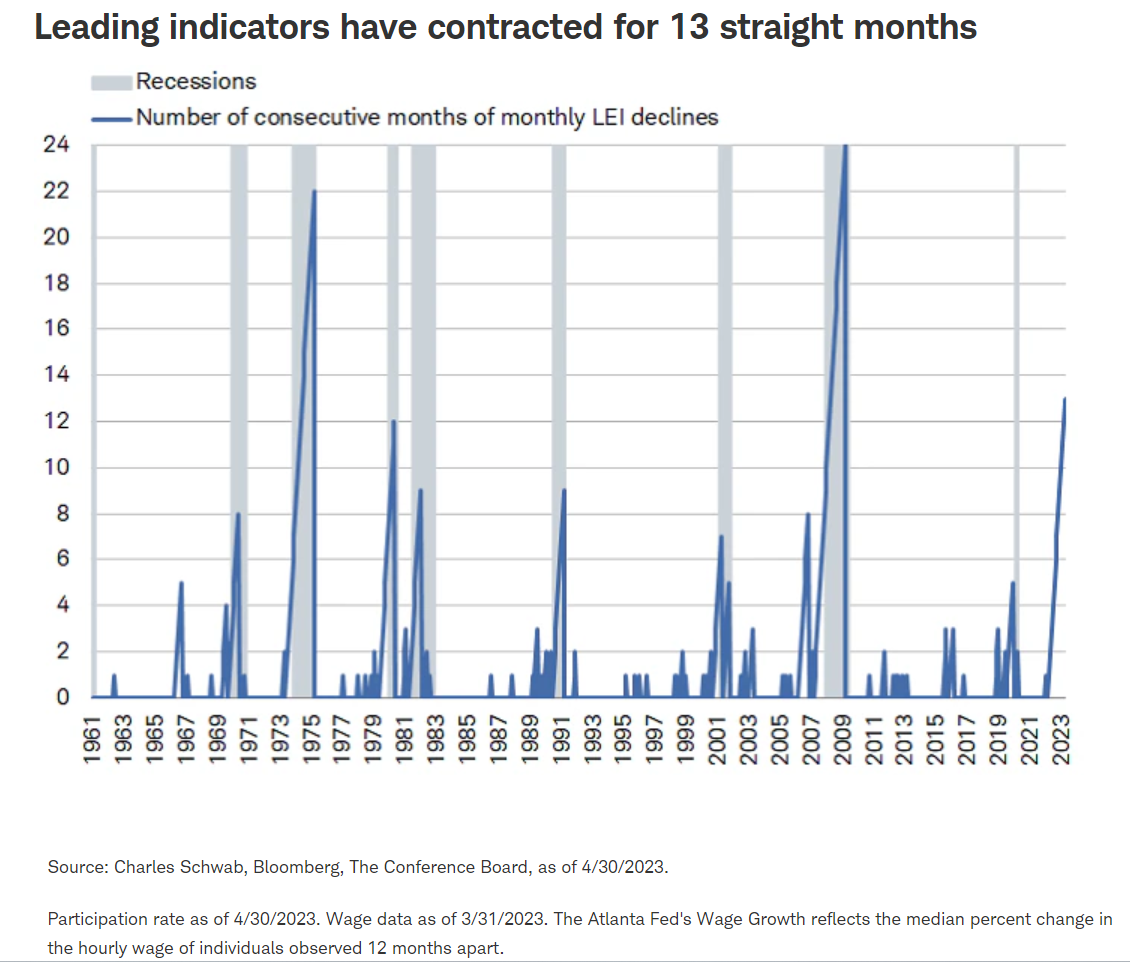

The split between leading and coincident data has garnered a lot of attention due to the significant deterioration in leading economic indicators over the past year. As shown in the chart below, The Conference Board's Leading Economic Index (LEI) has contracted for 13 consecutive months. Only twice in history have we seen longer streaks: the recessions that started in 1973 and 2007.

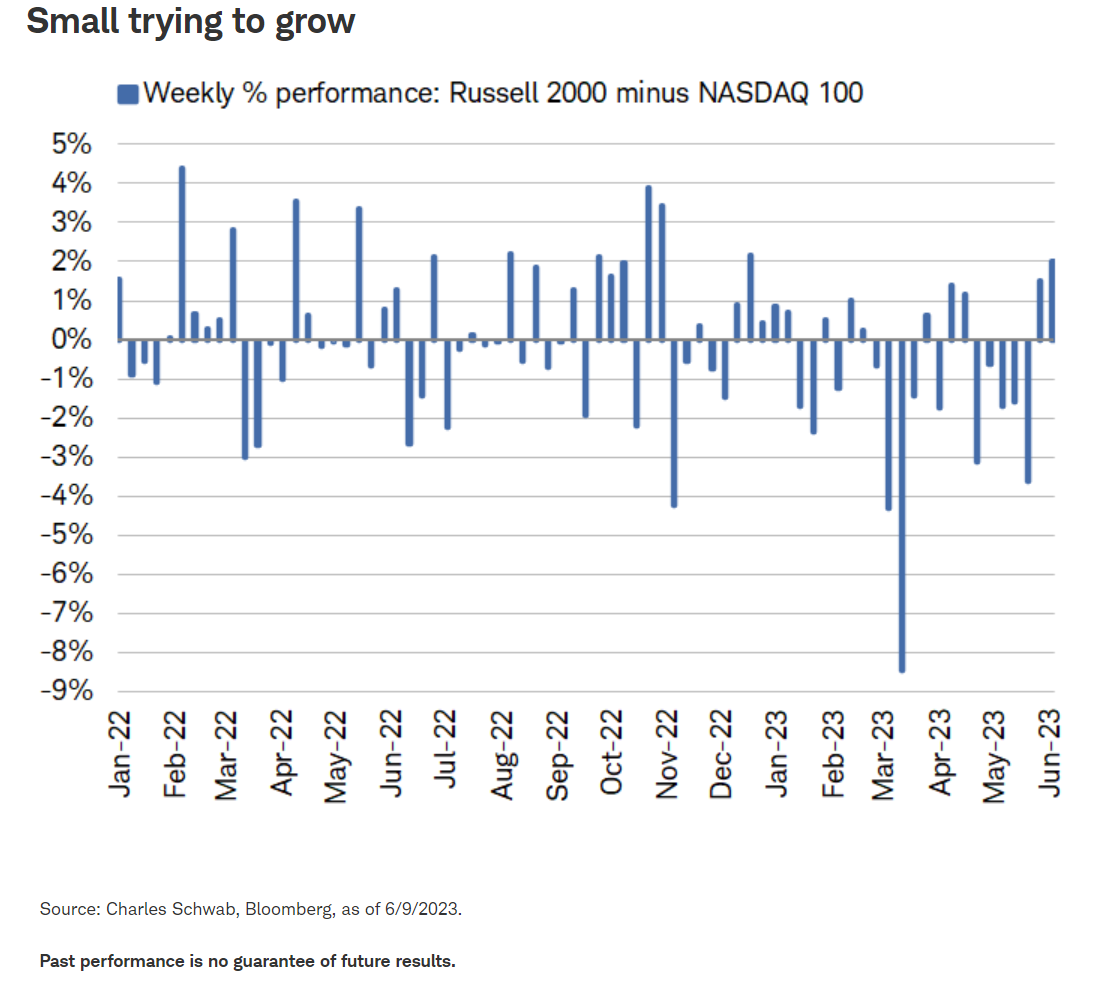

On the surface, the recessionary-like signal from leading indicators seems to be at odds with a stock market (as reflected by the S&P 500 index) that continues to propel higher. Yet, a look underneath the surface reveals that the market's internals are somewhat reflective of concerns over the trajectory of the economy. The Russell 2000 (a proxy for small caps and increasingly linked to economic growth) has underperformed the Nasdaq 100 (which tracks large-cap, tech-oriented stocks) considerably this year. In fact, the former has only outperformed the latter on a weekly basis for 10 weeks thus far in 2023—but that seems underwhelming when looking at how severe the down weeks have been, as shown in the chart below.

As has been well-advertised at this point, the bifurcation between strong performance among large caps and very little (if any) participation among small caps has cast doubt on the market's rally this year. The good news is that breadth metrics—such as the percentage of members trading above their 200-day moving average—started to flash positive signals in the first couple weeks of June, helping propel the Russell 2000 relative to its large-cap peers.

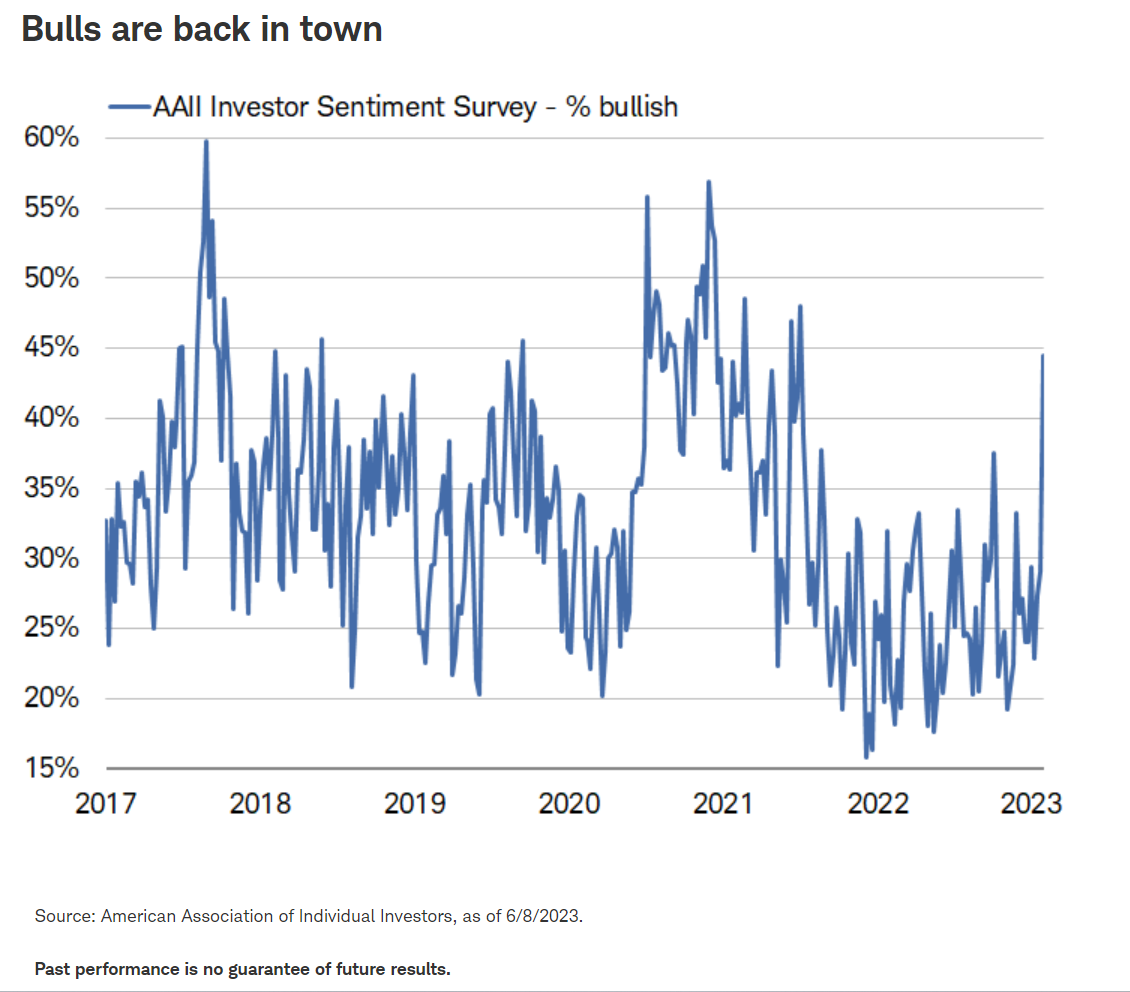

Should that continue, we think it will help sustain the market's advance. One growing risk worth pointing out, though, is the recent buildup in bullish investor sentiment. As shown in the chart below, the percentage of bulls in the American Association of Individual Investors (AAII) survey jumped in early June to its highest since November 2021 (the magnitude of the jump was the strongest since November 2020). It's not yet back at the peak, but in conjunction with other behavioral metrics that have started to underscore a buildup in optimism, any signs of froth are worth pointing out as a risk to the market.

We think it's important to keep in mind, however, that frothy sentiment in and of itself isn't a reason for stocks to reverse their recent trend. Rather, it exposes vulnerabilities for the market, which are then exacerbated by a negative catalyst.

Fixed income: Taking the long view

The Federal Reserve continues to follow its playbook to: hike, hold and recalibrate. After rapid rate hikes over the past 16 months, the decision to pause at the most recent meeting signals a subtle shift to the "hold and recalibrate" phase. The Fed made it clear that the door is still open to more rate hikes, with the median estimate among the members suggesting another two rate hikes of 25 basis points1 each could be seen this year. However, with inflation trending down, growth sluggish and the financial system still dealing with the fallout of bank failures—a more cautious approach seems to be warranted.

In our view, there are some key indicators we are watching that point to the likelihood that the peak in short-term rates may be near, while intermediate to long-term rates should fall.

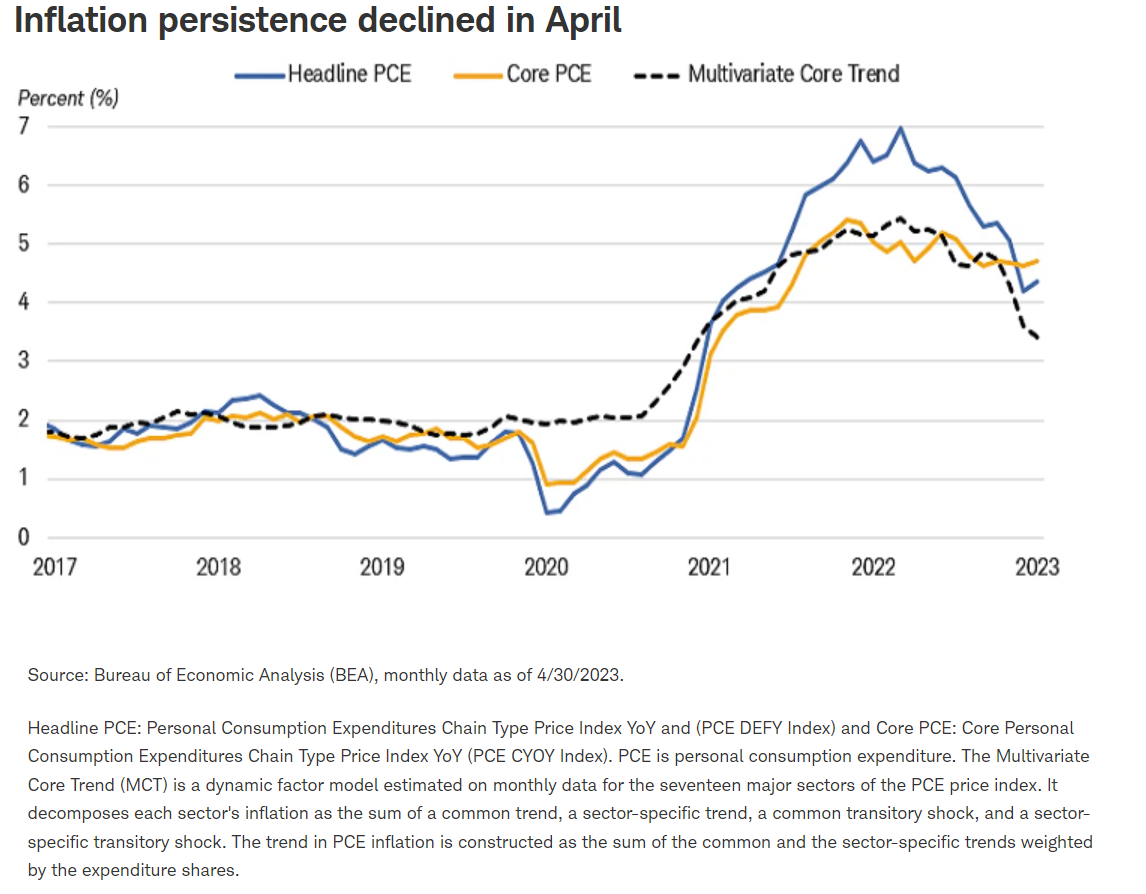

1. Inflation pressures are easing. Because the Fed's goal is to get its benchmark inflation index—personal consumption expenditures excluding food and energy (known as "core PCE")—heading toward its 2% target, we're keeping an eye on its rate of change. Overall or "headline" PCE has declined sharply from its peak level, but the core rate hasn't made much progress to the downside in recent months as consumer spending on services such as airline tickets remains firm.

However, with wage gains slowing, the savings rate coming down and the unemployment rate starting to rise, it's likely that consumers will begin to be more cautious going forward. A recent study from the New York Fed, which tries to take these factors into account, suggests that "sticky" or "persistent" inflation pressures are likely to ease in the months ahead.

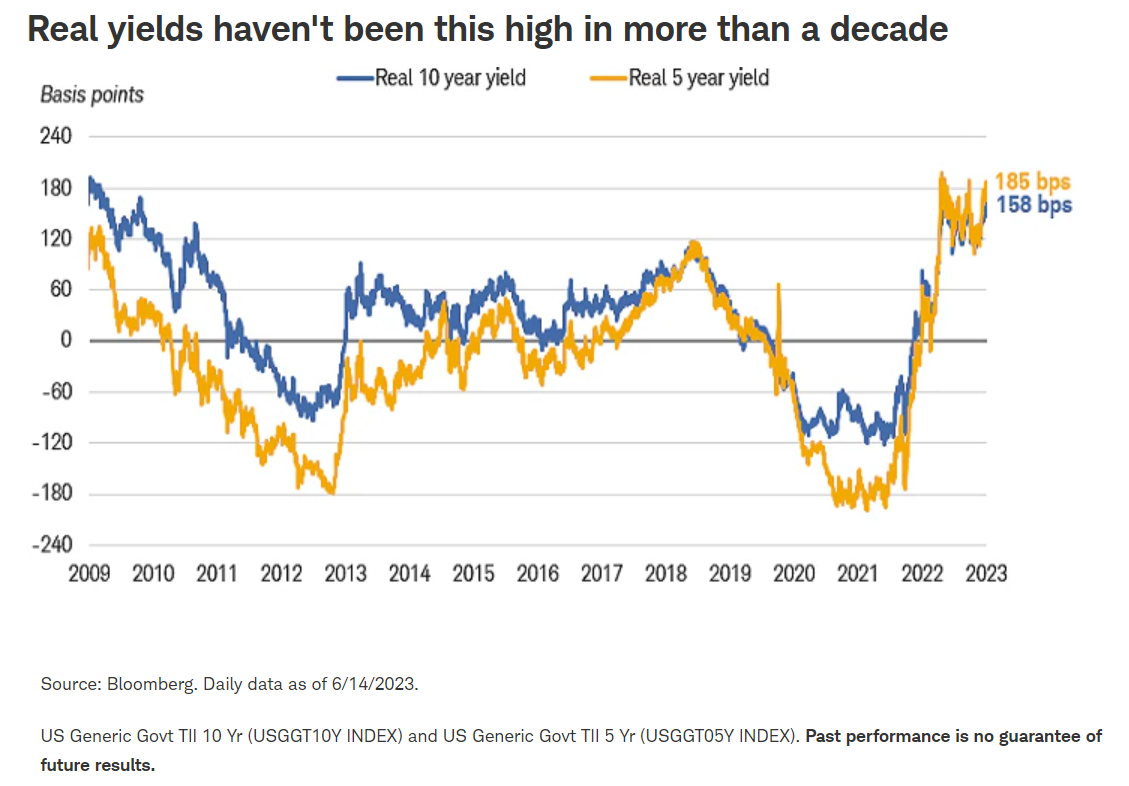

2. Real interest rates are high. Monetary policy works by pushing up the cost of borrowing to a level that slows economic activity. In particular, high real rates—adjusted for inflation—tend to have the sharpest impact on the economy. With the Fed hiking rates at the fastest pace in modern times, real interest rates are now back at the highest levels since 2009. Those rates make it more expensive for households to finance purchases of goods such as homes and cars. For businesses, high real rates drive up the cost of financing investment, hiring and expansion. When the cost of financing is too high, it historically leads to cutbacks and slower growth.

While the Fed may choose to hike rates again later this year, further tightening at this stage may risk pushing the economy into recession. We believe that the more the Fed tightens, the more likely it is that long-term interest rates will decline, and the yield curve inversion will deepen. It's likely to be a bumpy ride to lower yields as each data point is scrutinized for its potential policy impact. But overall, we continue to favor an investment approach of adding duration to bond portfolios. For investors concerned about inflation, Treasury Inflation Protected Securities (TIPS) offer positive real yields, which can provide a buffer against future inflation.

Global stocks and economy: Recession and a bull market

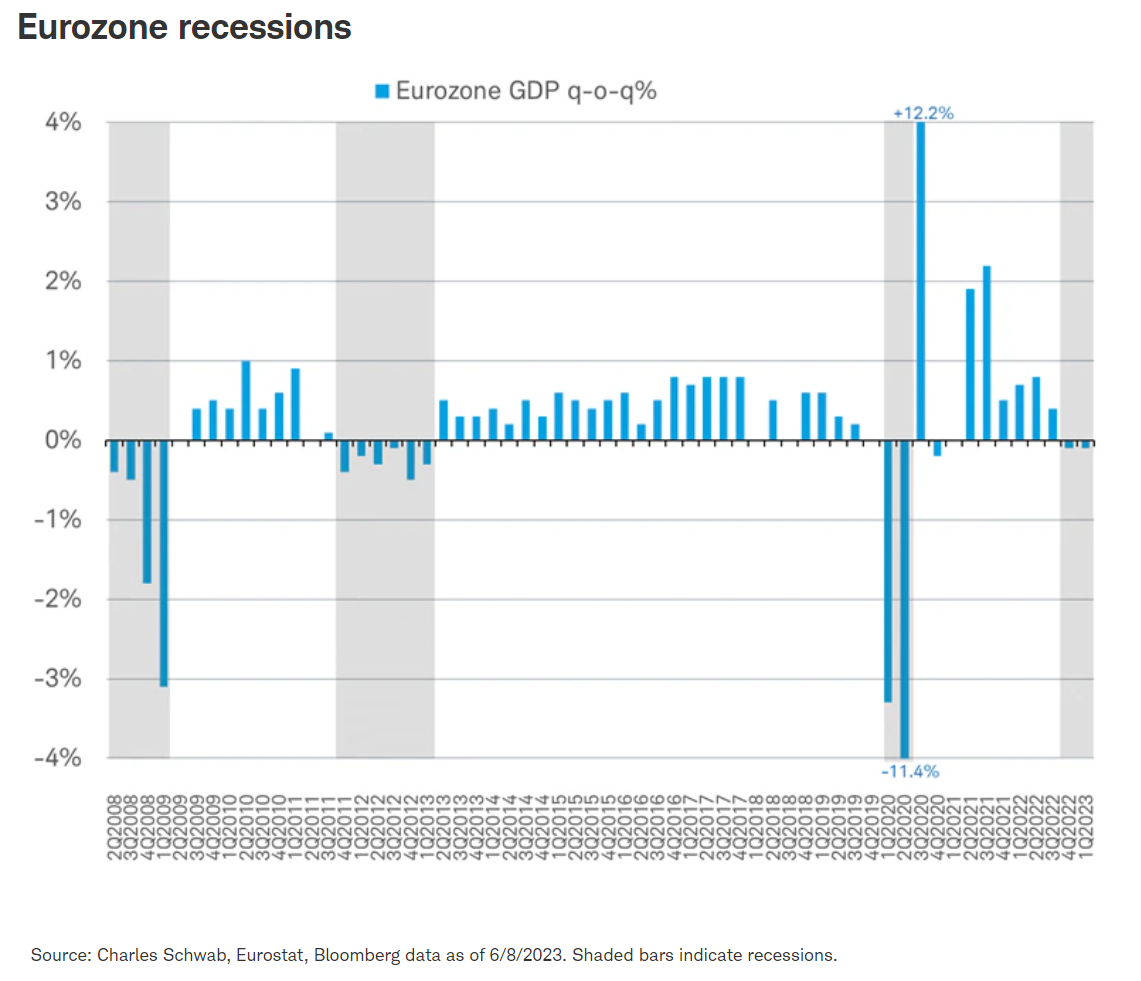

It's official: Europe has entered a recession. The eurozone economy shrank -0.1% in the first quarter, following a -0.1% decline in the fourth quarter—the first back-to-back quarterly decline since the pandemic. It also counts as the mildest recession ever, with consecutive quarterly gross domestic product (GDP) declines summing to just -0.2%.

During a typical global recession all areas of the economy (like manufacturing, services, retail, construction, and trade) tend to turn down around the same time. Yet, over much of the past year, only manufacturing and trade have seemed to be in a global recession, according to indicators such as industrial production, worldwide trade volumes, job growth by industry, surveys of purchasing managers at manufacturing companies, and many others. This can be called a Cardboard Box Recession, because items that are manufactured and shipped tend to go in a box. Also, demand for corrugated fiberboard, which is used to make cardboard boxes, is at recession levels, per data from the Fibre Box Association. In contrast, global services industries have continued to grow as consumers have turned to shopping for experiences over goods. As an example, the airline industry's International Air Transport Association, said last week that it is doubling its estimate for global net profit in 2023 on the surge in flying in North America and Europe.

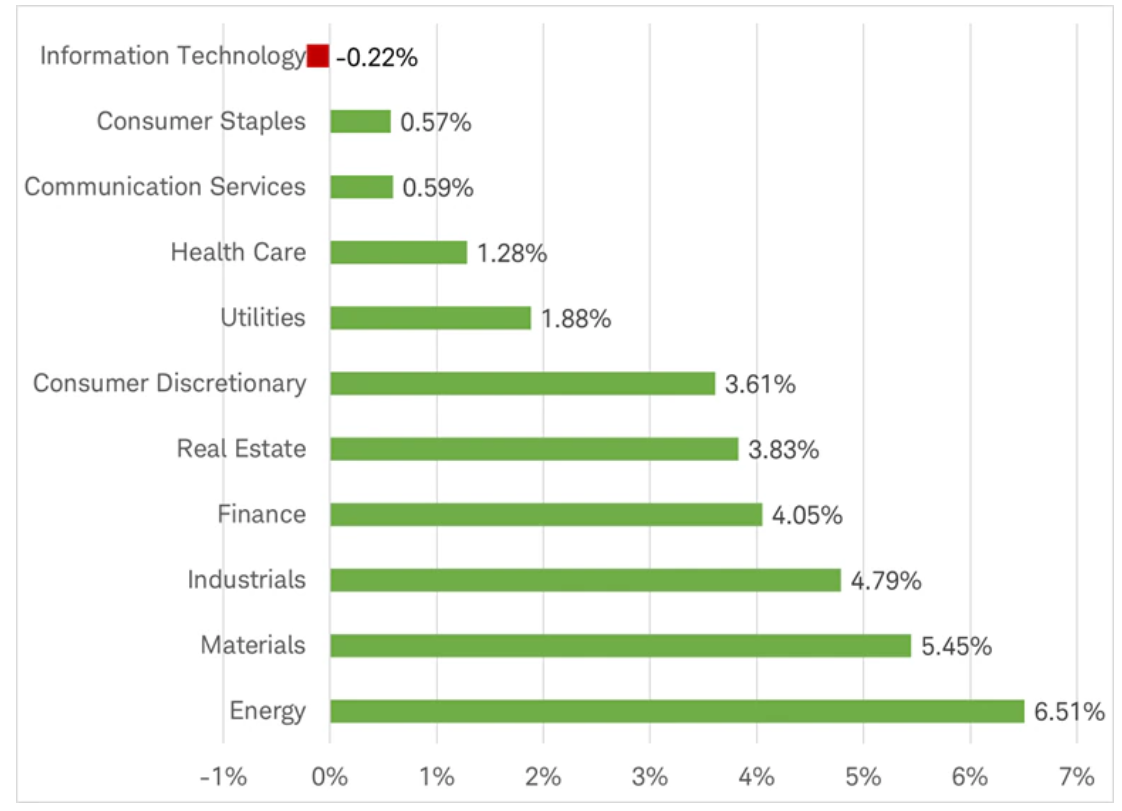

Despite the recession in Europe, the European Central Bank may not cut rates while inflation remains well above target levels. The surprise 25-basis-point rate hikes last week by the Bank of Canada and Reserve Bank of Australia, after both central banks had paused earlier in the year, are a reminder that the rate-hike cycle isn't over and central banks remain data dependent. Tech stocks soared this year amid speculation that central banks are flipping from hikes to cuts, and further fueled by optimism surrounding the developments in artificial intelligence. The surprise rate hikes last week suggest tech stocks may have been overbought on hopes of a rapid shift to rate cuts, as the tech sector moved to the worst-performing sector of the MSCI World Index in early June.

Early June performance of sectors of MSCI World Index

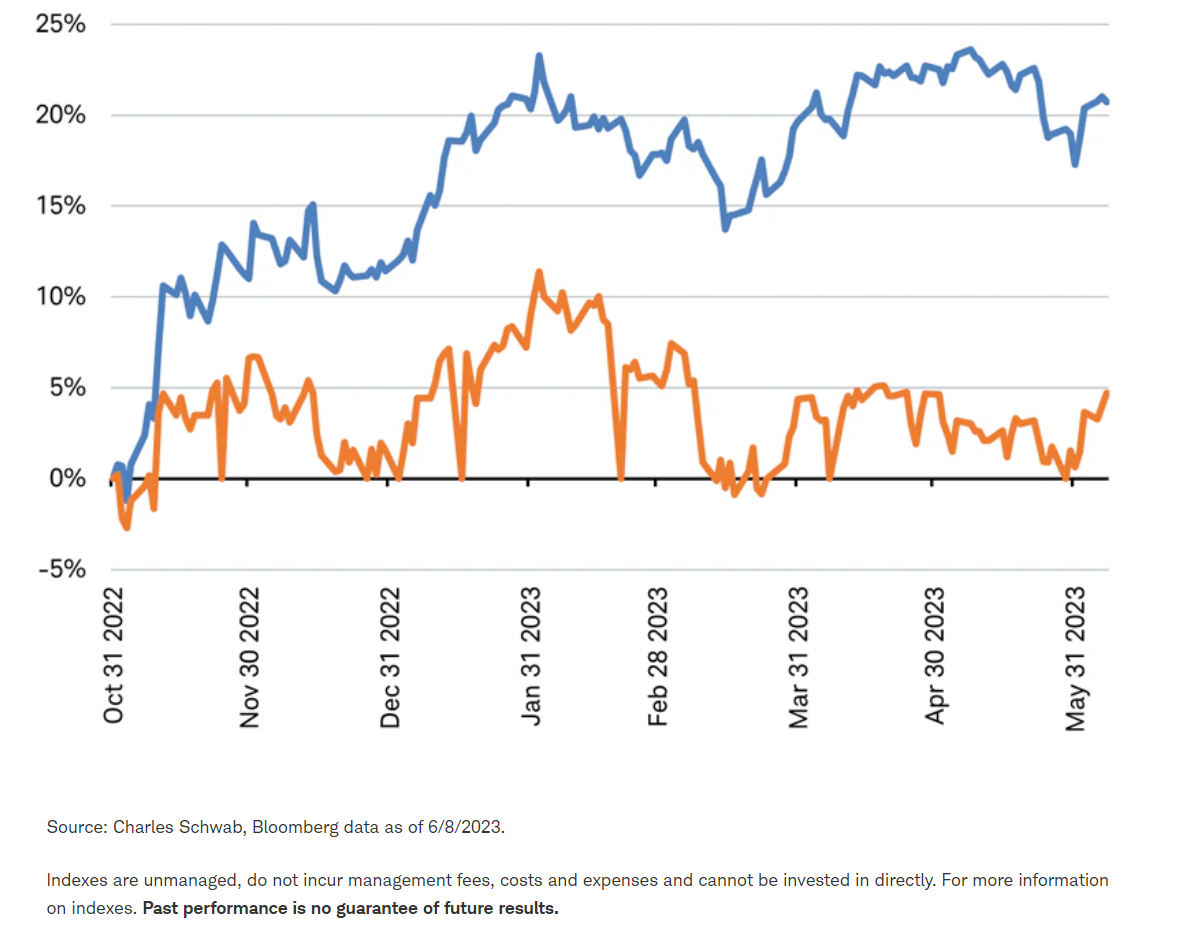

The performance in the first week of June has fueled mounting concern about the vulnerability of the narrow, tech-led advance in the U.S. stock market. But those concerns may not be valid outside the U.S., where the bull market has been broad. An equal-weight index represents the "average" stock, with each stock getting the same weighting. Last summer, global stocks had entered a bear market, with the equal-weighted MSCI World Index falling more than 20%, from its peak in late 2021 to the end of October 2022. Since October, the message from the performance of the average stock is that a new bull market seems to be underway.

The MSCI EAFE Index, along with the equal-weighted stock markets in Europe, Japan, and the United Kingdom, are all up well over 20% (measured in U.S. dollars) since the end of October 2022, meeting the technical definition of a new bull market. Yet the equal-weighted S&P 500 index is up only 4%, showing little progress for the average U.S. stock. In general, the greater the number of stocks that are helping push the overall market higher, the more support the market has. While U.S. and international stock are up a similar amount measured by capitalization-weighted indexes this year, the average international stock continues to outpace the average U.S. stock, offering a broader base of support for the bull market in international stocks.

Kevin Gordon, Senior Investment Strategist, contributed to this report.

1 A basis point is one-hundredth of 1 percentage point, or 0.01%, so 25 basis points would be equal to 0.25%.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All