Japan: Reclaiming Lost Decades

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsJapanese stocks may help boost the performance of international markets although the unique nature of Japan's economic and business structure could pose some risks.

Japan is home to the world's second-largest stock market after the United States. Japanese stocks make up the largest country weighting in the developed stock market index, MSCI EAFE, at 22%. Yet, Japan often gets little attention from investors. Ask a typical investor what they think of Japan and a common phrase you might hear is "lost decades," referring to the Japanese stock market failing to recover its peak of December 1989. But investors are taking another look as Japanese stocks show signs of finally closing in on their previous high after more than 30 years.

Japan's stock market, measured by the Nikkei 225 Index, hit a 33-year high last week following 10 weeks in a row of gains Japan's stock market has even outperformed the solid gains for the S&P 500® this year (when measured in U.S. dollars as well as in local currency), as it did last year despite stock markets around the world falling.

Confluence of positives

There are several reasons why Japanese stocks may continue to surprise investors and help lift the performance of international markets.

- Pro-market reforms are pushing companies to improve shareholder returns. Japanese companies have long hoarded cash, reaching $2.5 trillion, bloating book values but offering little return in a country where interest rates on cash remain below zero. Currently, about half of the 1835 listed firms on the Tokyo Stock Exchange have Price to Book (P/B) ratios below 1.0, including some very large, well-known companies. Earlier this year, the Tokyo Stock Exchange made changes requiring these companies wishing to list on the Prime and Standard sections to provide plans to boost their P/B ratios above 1.0 as soon as possible. This regulatory push is meant to encourage putting idle cash to use in the form of stock buybacks and other measures to help improve shareholder returns.

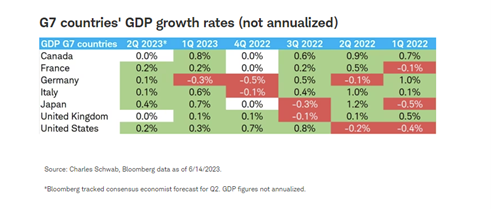

- Japan's GDP growth is exceeding the U.S. and other Group of Seven nations this year. Japan's GDP expanded an annualized 2.7% in the first quarter, much higher than economists' forecast of 1.9%. Several factors are helping drive growth, the most substantial of which may be something the Japanese economy hasn't consistently experienced since the 1980s: inflation. After decades of flat to falling prices, the year-over-year pace of inflation in April was 3.5% and has now been running above the Bank of Japan's targeted 2% for 13 straight months. This is the first time an entire generation of consumers and businesses has experienced sustained inflation. Previously, falling prices provided an incentive to delay consumption, which handicapped economic growth. But now, rising inflationary expectations could lead to positive changes in consumption and investment by Japanese individuals and corporations helping drive stronger growth.

- Japan may benefit from the "de-risking" of supply chains in Asia. Japan welcomed leaders of the Group of Seven (G7) nations for a summit in May. As leaders seek to mitigate economic security concerns by "de-risking" critical supply chains amidst anti-China consensus buildup in Washington and Brussels, Japan represented Asia as a low-risk investment destination. The event was accompanied by meetings between Japan's Prime Minister Kishida and executives from many of the world's biggest semiconductor businesses (TSMC, Samsung, Micron, Intel, IBM, and Applied Materials) that have the potential to result in significant manufacturing coming back to Japan. Japan, through the efforts of the Ministry of Economy, Trade, and Industry (METI), has already unveiled 1.3 trillion yen in subsidies to attract semiconductor companies, with seven manufacturers recently announcing investments. At the same time, Asian emerging and frontier markets are seeing gains in low-cost export businesses being moved from China. As these economies invest in capital and infrastructure to facilitate this transition, the Japanese industry has a leading position to supply them with construction equipment, trucks, robots, and machine tools.

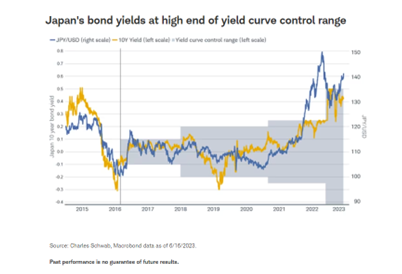

- Monetary and fiscal policy support. The Bank of Japan (BOJ) remains a global outlier, having not yet raised rates this cycle, despite inflation surpassing their 2% target. The slow approach to rate hikes is likely helping the performance of Japanese stocks, even if it has weighed on the yen. This slow approach also has meant that Japanese banks have not suffered the rising interest rate issues that plagued U.S. banks. The BOJ could change course and raise rates or alter its yield curve control policy that keeps interest rates in a tight range around zero. The BOJ's zero-interest-rate policy since 1999 makes it hard to foresee all the consequences of abandoning their current policy—even if done slowly and marginally. Yet, a likely result of moving toward tightening monetary policy is support for the yen. Higher yields and a stronger currency may prompt Japanese investors to move their substantial savings out of foreign investments back home into Japanese stocks and bonds.

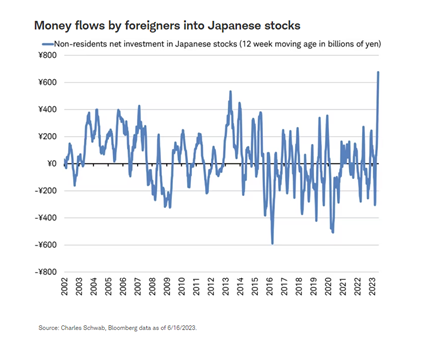

- Money flows are favoring Japanese stocks. Foreign investors were net sellers of 27 trillion yen of Japanese stocks between 2015 and the end of 2022. But this year, Japan's Ministry of Finance reports that Japanese stocks have seen rising net foreign inflows this year; foreign investors are increasingly seeking exposure to Japan, with Warren Buffett among them (Berkshire Hathaway said on Monday that its wholly-owned subsidiary National Indemnity Company increased its stake in five Japanese trading firms to average more than 8.5% after a prior increase to 7.4% was announced in April). The 12-week moving average of net inflows by foreigners into Japanese stocks is the highest in more than 20 years. Japan's domestic demand for stocks may also be on the rise, supported by fiscal policy. Starting next year, the tax-free amount Japanese households can invest in equities as part of the Nippon individual savings accounts will double in size, and investors will no longer have a 20-year cap on the tax-exempt period. A shift to an inflationary mindset may also encourage investors to move away from holding cash into investments with the potential for higher returns.

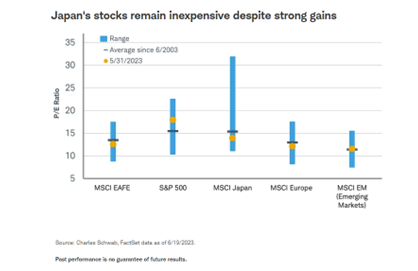

- Japanese stocks remain inexpensive. Japanese stocks currently trade at a price-to-earnings ratio of 14 on 12-month forward earnings estimates, which is below the 20-year average for the MSCI Japan Index. That compares to an above-average 19 for the U.S. S&P 500 Index. Japanese stocks are inexpensive relative to U.S. stocks today.

Japan's unique risks

We believe Japan could surprise many investors with strong performance driven by a confluence of positive factors. Yet, there are risks.

- Pro-market reforms may fail. A push to improve corporate governance in 2014-2015 under former Prime Minister Abe did not significantly alter the valuation of Japanese stocks, which have long been viewed as inexpensive and a "value trap." Monitoring cash levels may be an important indicator.

- Slower global growth may weigh on exports. Slowing economic momentum in China, Japan's largest trading partner, could weigh on growth. Japan is also an export-dependent economy and could be adversely affected if global growth is weak. An upcoming signal of momentum is the widely watched Tankan quarterly assessment of business conditions in Japan issued by the Bank of Japan is due on July 1.

- Japan's aging population. Japan's aging population had tended to restrain growth and inflation, although Japan has some unique advantages in combating this drag relative to other countries. First, unlike many developed economies where the domestic population is the largest customer base, more than half of the sales of Japanese companies are outside of Japan (e.g. big Japanese companies like Sony and Toyota get 70-80% of sales outside of Japan) mitigating this risk. Second, the potential wave of capital spending could boost output per worker in Japan, whose productivity is among the lowest of the G7. Third, the costs of an aging population are much less of a drag for Japan than the United States. Japan is aging more quickly than the U.S., but healthcare costs per capita for Japan ($4,378 during pre-pandemic 2019 according to the World Bank) are a fraction of those in the U.S. ($12,914 during pre-pandemic 2019), per the U.S. Centers for Medicare & Medicaid Services.

- Japanese stocks have seen a powerful rally already. Strong net money inflows and a 10-week winning streak have pushed Japan's stocks to a 33-year high. Japanese stocks might consolidate recent gains.

- Ultimately, Japan's debt growth may be unsustainable. As of December 2022, Japan's government debt is 263% of GDP, double that of the U.S. (123%), and the highest of any developed nation according to the International Monetary Fund (IMF). To help finance this debt, the Bank of Japan has bought half (52%) of all Japanese government bonds, known as JGBs. This is more than double the share of U.S. government debt owned by the U.S. Federal Reserve (20%). This large growth in debt financed with low-interest rates has weighed on the value of Japan's currency. The yen has fallen nearly 25% against the dollar since the end of 2020 when the bank's self-imposed ceiling on purchasing JGBs was lifted in response to the pandemic. This effect on its currency may eventually act as a market-imposed debt limit on Japan, but since Japan has a high savings rate and can finance its debt without relying on foreign investment, it is not clear how high domestically financed government debt can grow without adverse effects.

Japan's stock market may continue to surprise investors as it nears an all-time high, reclaiming its lost decades of performance. However, the uniqueness of Japan's economy and businesses also pose risks. Further gains by the second-largest stock market in the world can help boost the performance of international stocks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Fixed-income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Currencies are speculative, very volatile, and are not suitable for all investors.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research, and are developed through analysis of historical public data.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

The Tanki Keizai Kansoku Chousa, or Tankan, is a short-term economic statistical survey carried out by the Bank of Japan which aims to provide an accurate picture of business trends of enterprises in Japan, to aid in their implementation of monetary policy. The survey is conducted on a quarterly basis, covering approximately 10,000 enterprises.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All