We expect generally good performance during the second half of the year, although volatility may increase, especially for high-yield bonds.

Corporate bond investments generally performed well during the first half of the year. With higher starting yields, coupon payments were a key driver of returns, while a modest decline in intermediate- and long-term yields this year helped pull up prices, as well.

Performance in the second half of the year may be similar, but we continue to see a greater risk of price declines with high-yield corporate bonds. With the Federal Reserve expected to keep rates high for an extended period of time, potentially slowing down economic growth, we continue to suggest investors focus on high-quality investments.

For more conservative investors looking for income today, we prefer investment-grade-rated corporate bonds. For those investors who are willing to take more risk to earn higher yields, highly rated preferreds appear more attractive than high-yield bonds. If the economy slows, as we expect, high-yield bond prices may fall sharply, but the prices of preferreds issued by the large, highly rated U.S. banks may hold their value better.

Investment-grade corporate bonds appear attractive

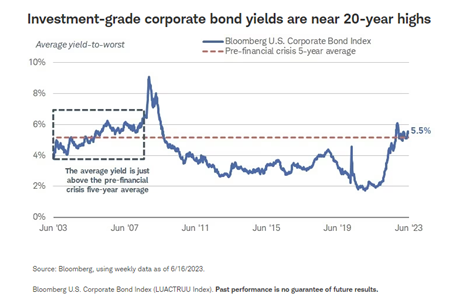

Investment-grade corporate bonds still appear attractive for investors looking to earn higher yields without taking too much additional risk. Yields generally remain near their highest levels since 2009, with the average yield-to-worst (the lowest possible yield that can be received on a bond with an early retirement provision) of the Bloomberg U.S. Corporate Bond Index closing at 5.5% on June 16th. That index has an average duration—a measure of interest rate sensitivity—of seven years, meaning it has more interest rate risk than short-term investments. Over 90% of the index is made up of bonds with A and Baa credit ratings, so it has moderate credit risk.1

Investors who have been hesitant to consider more intermediate- or long-term bonds while the Federal Reserve was hiking rates still have the opportunity to earn yields that generally haven't been available since before the 2008-2009 financial crisis. In the five years leading up to that crisis, the index offered an average yield of 5.2%, lower than where it is today. In other words, aside from the surge in yields in 2008 and 2009 as corporate defaults were rising, yields are near their 20-year highs.

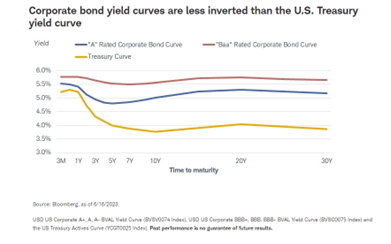

The average index doesn't tell the whole story, as it represents an average of all investment-grade credit ratings and all maturities. As the chart below illustrates, short-term corporate bonds don't offer much of a yield advantage over Treasuries, so those investors considering investments with maturities of two to three years or less might want to consider Treasuries or certificates of deposit (CDs). As the time to maturity lengthens, however, corporates look more and more attractive relative to Treasuries.

The "A" and "Baa" rated corporate bond yield curves are noticeably less inverted than the U.S. Treasury curve. While intermediate-term yields are still lower than short-term yields, the difference is significantly less than that gap with U.S. Treasuries. While accepting lower yields with longer-term bonds relative to what short-term bonds offer may be a difficult pill to swallow, it's less of an issue with investment-grade corporate bonds than it is with U.S. Treasuries.

There are risks with corporate bond investing, like credit risk—that is, the risk that an issuer can't make timely interest or principal payments and defaults. The risk of default is generally low with investment-grade-rated issuers because they tend to have stronger balance sheets and more stable cash flows than sub-investment-grade issuers. An economic slowdown could weigh on the broad corporate bond market, but we think the prices of investment-grade corporate bonds should hold their value more than high-yield bonds.

Investor takeaway:

Investors looking to earn higher yields without taking too much additional risk should consider investment-grade corporate bonds. While slower economic growth does pose a risk to the market, we expect their prices to hold up better than the prices of high-yield bonds.

High-yield corporates: Caution is warranted, but positive returns are possible

We remain cautious about high-yield bonds over the near term, but their high yields can help them earn positive total returns over long holding periods. For those considering high-yield bonds today, we continue to expect spreads to rise and prices to fall over the next six to 12 months, but their high coupon payments can help offset some of those potential declines.

We have no shortage of concerns related to the high-yield bond market, including:

- the inverted yield curve;

- the risk of tighter financial conditions following the aggressive Fed rate hikes;

- our outlook for slower economic growth;

- tighter bank lending standards;

- rising corporate defaults.

Each of those factors alone is a cause for concern, and when all are taken together they suggest that spreads should rise later this year. A credit spread represents the extra yield that corporate bonds offer compared with another bond of comparable maturity, such as a Treasury bond, to compensate for the risk of lending to a corporation. When the economy slows or investors believe that issuers might face difficulties repaying their debts, spreads may widen as bond prices fall.

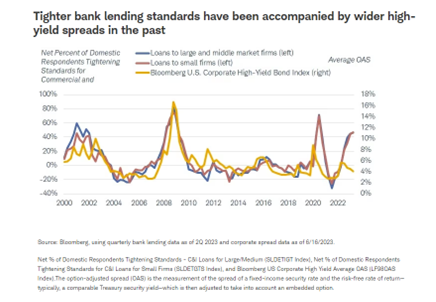

Bank lending standards can be a key driver of the economy because reduced bank lending, or tighter lending conditions, may mean less spending or investment by households or businesses. The most recent Senior Loan Officer Opinion Survey from the Federal Reserve showed that banks are generally tightening their lending standards when lending to firms of all sizes, and demand for loans has declined as well. When lending standards have tightened in the past, high-yield spreads have tended to rise. That hasn't really happened during this cycle, with the average option-adjusted spread of the Bloomberg U.S. Corporate High-Yield Bond Index declining lately, closing at 4.01% on June 16th.

The number of corporate defaults has already been on the rise lately, but the high-yield market has been shrugging that off. According to Moody's Investors Service, the U.S. trailing 12-month speculative-grade default rate rose to 3.1% in May 2023, up from just 1.4% in May 2022.2 That rate is expected to rise to 5.6% by May 2024. We'd expect spreads to rise given the risk of more corporate defaults. In previous economic slowdowns and "risk-off" investing periods over the last 13 years, spreads have risen to 8% or above. Should that happen during the cycle, high-yield bond prices would likely fall sharply.

Despite those concerns, the high-yield bond market has been one of the best-performing fixed-income investments this year. We don't expect that trend to continue, but it's still possible for high-yield bonds to post positive total returns even if spreads rise. The high coupon payments can help offset price declines over longer holding periods. The high-yield index has an average coupon rate of almost 6%, meaning prices could fall by roughly 6% over a 12-month span and an investor may still break even.

Investor takeaway:

We're still cautious on high-yield bonds in the near term. Price declines seem likely, which should result in underperformance compared to Treasuries or investment-grade corporates over the next 12 months. But from a long-term strategic standpoint, the 8.5% average yield that high-yield bonds offer represents a high starting point for investors who plan to hold for the long run and can ride out the ups and downs.

Preferred securities: The entry point appears attractive, but be prepared for volatility

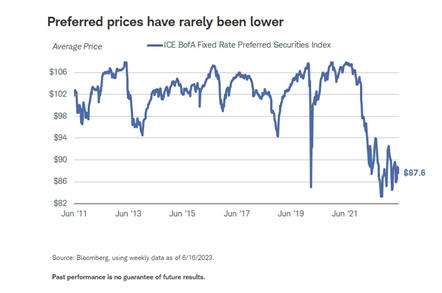

Preferred securities continue to be rattled by banking sector concerns, as financial institutions make up more than 80% of the ICE BofA Fixed Rate Preferred Securities Index. Prices have rebounded from their recent lows, but still remain low compared to the last 10 years.

With the fall in prices pulling up the average yield of the index to near 7%, the entry point appears attractive for income-oriented investors, but we'd caution that volatility should remain elevated. Preferreds have high-interest rate risk (i.e., the risk that a change in overall interest rates will reduce their value) and high credit risk. Any additional rise in Treasury yields, while not our base case, could pull preferred yields up and prices down. Credit risk appears to be more of a risk these days given the large concentration of financial institution issuers. Although the banking sector's woes have settled down, there are still concerns given the depressed value of many investments that banks hold on their balance sheets. Regional bank stocks have rebounded from recent lows but are still down sharply this year, suggesting that the markets are still concerned about the profit outlook.

For many $25 par preferred securities (commonly held by individual investors), those issued by the largest U.S. banks by total assets have generally delivered positive total returns this year. Meanwhile, preferreds issued by small and mid-size banks have seen a wide dispersion of returns, including some deeply negative total returns. One key characteristic of preferreds is that they rank below traditional bonds—for example, in a default scenario or after a bank failure the recovery rate likely would be very low if there were any recovery value at all. Given lingering concerns about some small banks, some preferred security prices remain very depressed.

Finally, for those considering preferreds today, it always makes sense to consider them long-term investments. Although the starting yield appears attractive, coupon payments—not price appreciation—should make up the bulk of the return in the near term. Prices are low given the aggressive pace of rate hikes and concerns about the banking sector, and those factors are unlikely to reverse soon.

Investor takeaway:

Preferred security yields appear attractive for income-oriented investors willing to take additional risks. Always consider preferred long-term investments and be prepared to ride out the ups and downs. If you are considering preferreds, those issued by large, highly-rated banks appear to be the most attractive now. Their prices have generally held up better than the preferreds issued by small and midsize banks, and we expect that trend to continue should the banking concerns linger.

1 The Moody's Investors Service investment-grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C.

2 Moody's Investors Service, "May 2023 Default Report," June 15, 2023.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Investing involves risk including loss of principal.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Fixed-income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Preferred securities are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features may affect yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so they are subject to increased loss of principal during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than the original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

The information provided here is for general informational purposes only and is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific advice is necessary or appropriate, consult with a qualified tax advisor, CPA, financial planner or investment manager.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approve or endorse this material, guarantee the accuracy or completeness of any information herein, or make any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab