After the disruptions of the past few years, many of us are looking for a return to normal. For investors in emerging-market bonds, normal would mean a world in which global inflation is in check, interest rates are no longer rising, China is healthy, and traditional asset correlations resume.

That may be where we are headed, even if we’re not there yet.

Although recessionary fears still loom large, we’re now seeing a confluence of trends that should bode well for some parts of the emerging-market bond universe. But emerging markets are diverse, and fundamentals vary widely, making sector and credit selection key.

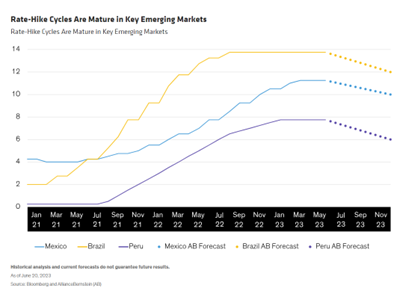

Mature Rate-Hike Cycles Could Pace Emerging Markets

An end to aggressive rate hikes could be a catalyst for emerging markets, following last year’s sharp rise in both developed-market yields and the US dollar, which weighed heavily on the performance of emerging-market debt. Although global inflation remains elevated, we believe the era of rapid rate hikes is over.

Here, emerging markets hold the edge. Many emerging-market central banks hiked interest rates earlier, faster, and more aggressively than their developed-market counterparts. This was due in part to more recent experience addressing high inflation, as well as a greater tendency for inflation expectations to become unanchored in emerging markets. As a result, monetary tightening is on pause or nearing completion in many emerging markets, including Mexico, Brazil, and Peru (Display).

This landscape has benefited local emerging-market bond markets, particularly in Latin America, which have outperformed so far this year. It’s also a dynamic that can continue, as central banks in the developing world eventually pivot to cutting rates.

Local Duration or Hard Currency? A Bifurcated Landscape

With inflation coming under control and emerging-market interest rates largely poised to hold steady or decline, local-duration assets—that is, sovereign debt denominated in local currencies—have benefited. We believe local markets with mature hiking cycles, core disinflation, and attractive yield premiums will continue to see the best opportunities.

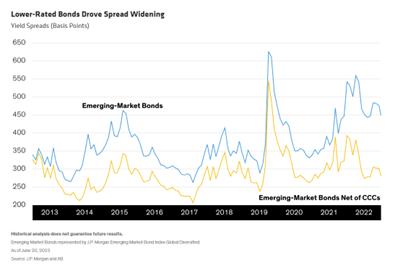

Among hard-currency assets, spreads have tightened in recent months but are still elevated in the lowest-quality cohort—especially CCC-rated securities. This is reflected in the J.P. Morgan Emerging-Market Bond Index Global Diversified, where much of the observed valuation at a headline index level comes from these lower-quality credits (Display). Once this is accounted for, index spreads do not appear as attractive.

In a world where the growth outlook in the second half of this year could come under pressure, this lower-quality portion is where investors should be most selective.

A Bumpy Start to China’s Economic Reopening

It’s been clear for a while that global growth is under pressure. But, in our view, emerging markets are poised to grow faster than developed markets over the coming year. A lot could depend on China. China’s decision to abandon restrictive zero-COVID protocols has provided marginal benefits to emerging markets, but it’s been a bumpy road. As we expected, China’s reopening hasn’t supercharged the emerging-market growth outlook, and recent economic data have been underwhelming so far.

The initial bounce from China’s reopening has faded, and policymakers appear to have moved economic performance higher up their priority list, with Beijing cutting a series of policy rates to help support the economy. Although far short of past fiscal stimulus measures, these efforts should help offset the slowdown in domestic demand and, in turn, support emerging-market asset price performance—particularly important if global growth underwhelms in the second half of 2023.

We’d like to see more evidence of increased consumer spending from China spilling over to neighboring markets in Central and East Asia. This could take the form of increased tourism by Chinese nationals or an uptick in trade between China’s major trading partners—including the 10-member Association of Southeast Asian Nations.

It’s been said that when China sneezes, the rest of the world catches a cold. Conversely, we believe a return to good health by China would bode well for its closest neighbors.

Diversification Coming Back into Balance

Diversified investors have at least one trend working in their favor. Traditionally, there has been an inverse correlation between duration-sensitive assets like US Treasuries or other developed-market sovereign debt, and risk assets like credit spreads. Last year, that correlation turned positive, which weighed down returns when both sectors stumbled at the same time.

Now, the correlation between duration and risk assets has returned to negative, which should aid investors’ diversification efforts and improve the risk/return profile of emerging-market hard-currency bonds, which have both duration and spread components that offer attractive long-term risk-adjusted return potential.

Have Emerging Markets Turned the Corner?

With the bulk of monetary tightening over and China abandoning zero-COVID policies while incrementally ramping up economic policy support, two primary headwinds to emerging markets are easing. In this more subdued environment, emerging-market central banks may even have runway to reverse previous monetary tightening.

Conditions are increasingly favorable for emerging-market bonds to regain their footing—particularly in local duration. With investors generally under-allocated to emerging-market debt following the worst year of asset-class outflows on record in US-dollar terms, renewed inflows could provide added momentum, although investors will need to be particularly selective in the lowest-credit-quality names.

Investors should also bear in mind that, while emerging-market debt represents a large and growing percentage of the global fixed-income market, it isn’t a monolith. Rather, it comprises more than 80 countries split across multiple asset classes and different currencies—making both security selection and asset-class selection critical.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© AllianceBernstein

Read more commentaries by AllianceBernstein