India's growth initiatives and demographics may help its economy continue to advance; its stocks seem to have priced in high expectations for the world's fifth-largest economy.

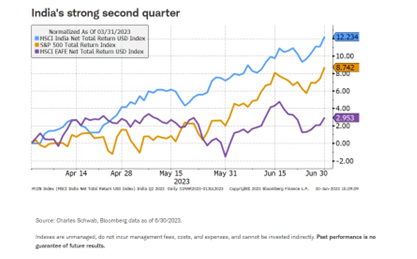

The best-performing stock market in the world during the second quarter was India even outpacing Japan's solid performance. Stocks headquartered in India make up 14% of the MSCI Emerging Market Index, the largest share of any country other than China and Taiwan.

India's rising relevance

There are several reasons why India has become increasingly important to the global economy and markets:

- India's economy is now the world's fifth biggest, recently surpassing the United Kingdom. India's GDP is expected by economists to grow faster than 6% in each of the next three years, compared to the U.S., which is expected to grow less than 2%. The International Monetary Fund forecasts India to be the third-largest economy by the end of the decade, overtaking both Japan and Germany.

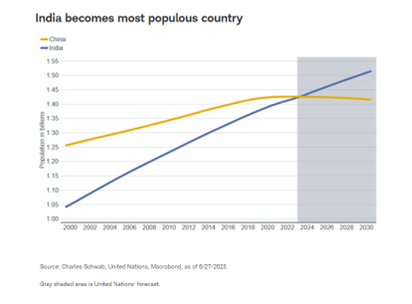

- India's population is set to surpass China's this year according to the United Nations, which has predicted India will end 2023 with 1.429 billion people. China is forecasted to end the year with 1.426 billion. Thirty years of a "one child" policy in China and the high cost of raising children have resulted in the fertility rate falling to 1.2 births per woman in China, while India's rate is 2.0 births per woman.

- India has the world's largest democracy, with a capitalist economy and the world's most popular leader, Prime Minister Modi. As the world looks to "de-risk" supply chains in Asia, some are looking to India. Demonstrating the desire to work with India on their shared goals, President Biden threw a formal banquet for Modi at the White House and the leaders of Congress invited him to address a joint session in early June.

India's positive momentum

For decades, foreign companies invested in China setting up factories while India's manufacturing sector lagged. India did not follow China's development approach of restricting outbound capital flows and directing excess domestic savings towards infrastructure and foreign exchange reserves. Rather, India has been subject to swings in capital flows and regulatory land-use restrictions that have hindered infrastructure development. Currency volatility forced India's central bank to try to offset the impact of irregular capital flows with aggressive hikes and cuts to defend the currency. Currently, India may be seeing positive momentum on these issues of infrastructure and currency that may help spur growth momentum in manufacturing.

- India is making changes to increase its attractiveness as a manufacturing base. India is known for IT outsourcing, but the sector only employs a small fraction of the workforce. The pandemic highlighted the supply chain risks of concentrated manufacturing bases in Asia, and western policymakers' desire to "de-risk" Asian supply chains may mean a shift to India. Modi's government is making efforts to attract companies by offering incentives for producing in India, easing regulatory burdens, and investing billions of dollars in improving the country's infrastructure. It is showing some signs of success. For example, Apple is expected to move some iPhone manufacturing to India.

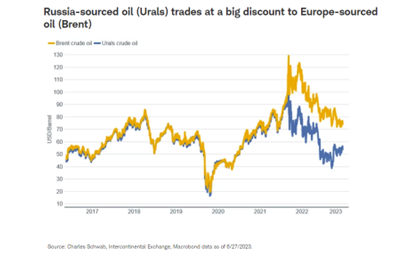

- India's currency may become less volatile through the purchase of Russian oil. India may be less prone to capital outflows as Russia receives rupees in exchange for oil exports to the country. Should the trade relationship become longer lasting, Russia may avoid converting the rupees into Western government bonds and instead hold them in Indian government bonds used to fund India's massive infrastructure needs. This should lead to capital inflows and a stronger rupee, which would be a powerful combination that may lower long-term rates in India, supporting stocks and real estate values and potentially contributing to greater stability in India's monetary policy.

- India is benefiting from cheap energy, a critical manufacturing input. India's purchases of Russian oil, coal, and other energy products since the war began in Ukraine offer a cost advantage to manufacturing.

India's risks

India's positive momentum faces some risks for investors.

- India's path to becoming a manufacturing powerhouse is not easy. India is challenged with lower productivity, labor-skills mismatch, inconsistent manufacturing quality, poor infrastructure, complicated investment rules, and labor and land-use regulations. In contrast to India, China's government takes quick and decisive action with little political opposition in the way.

- The climate could pose a challenge to India's growth. This past June, temperatures in India soared as high as 115˚ F, part of an increasing pattern of intense heat waves in the country over the past decade. The World Bank has flagged India as likely to be one of the first places in the world where heat waves breach the human survivability threshold. The potential for increasingly intense heat waves poses a risk to lives, agriculture, manufacturing, and political stability.

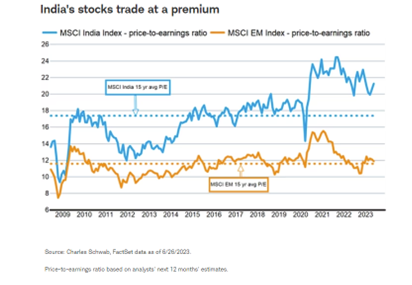

- India's stocks are typically expensive but are even more so now. India has a unique growth story relative to the emerging-market (EM) universe, as it has been more domestically focused than other Asian economies. Its young demographic and small manufacturing share of GDP gives it a runway for growth and as a result, its stocks tend to trade at a premium to the EM universe. However, Indian stocks are currently even more expensive than their longer-term average and have a larger premium to the EM universe than usual.

India's growth momentum may carry it to the top three global economies in size before the end of the decade if it is able to capitalize on its transformative initiatives. It will take time for companies to evaluate if they are able to achieve the quality and reliable manufacturing needed to open and maintain operations in the country. India's stocks are expensive, perhaps already priced in high expectations. Holding a broad mix of exposure to emerging markets includes meaningful exposure to India's growth, but also diversification to help insulate from its risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Fixed-income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Commodity-related products, including futures, carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, and illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions, regardless of the length of time shares are held. Investments in commodity-related products may subject the fund to significantly greater volatility than investments in traditional securities and involve substantial risks, including the risk of loss of a significant portion of their principal value.

Currency trading is speculative, volatile, and not suitable for all investors.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research, and are developed through analysis of historical public data.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

The MSCI India Index is designed to measure the performance of the large and mid-cap segments of the Indian market covering approximately 85% of the Indian equity universe.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab