2023 Mid-Year Outlook: Municipal Bonds

Membership required

Membership is now required to use this feature. To learn more:

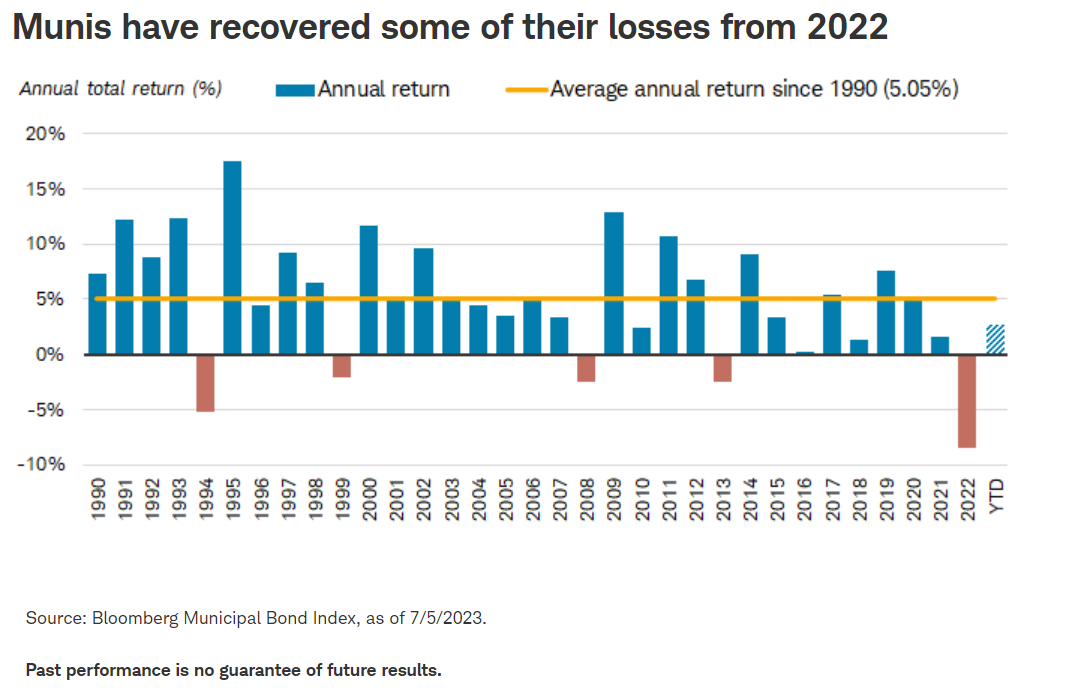

View Membership BenefitsThe old saying, "the more things change, the more they stay the same" appropriately summarizes the municipal bond market today. Despite an awful 2022 for total returns and an eventful first half of the year dominated by concerns about banking instability and the debt-ceiling drama, the outlook for the muni market is largely unchanged. Given the combination of attractive yields and strong credit conditions, we have a positive view on the muni market over the remainder of the year.

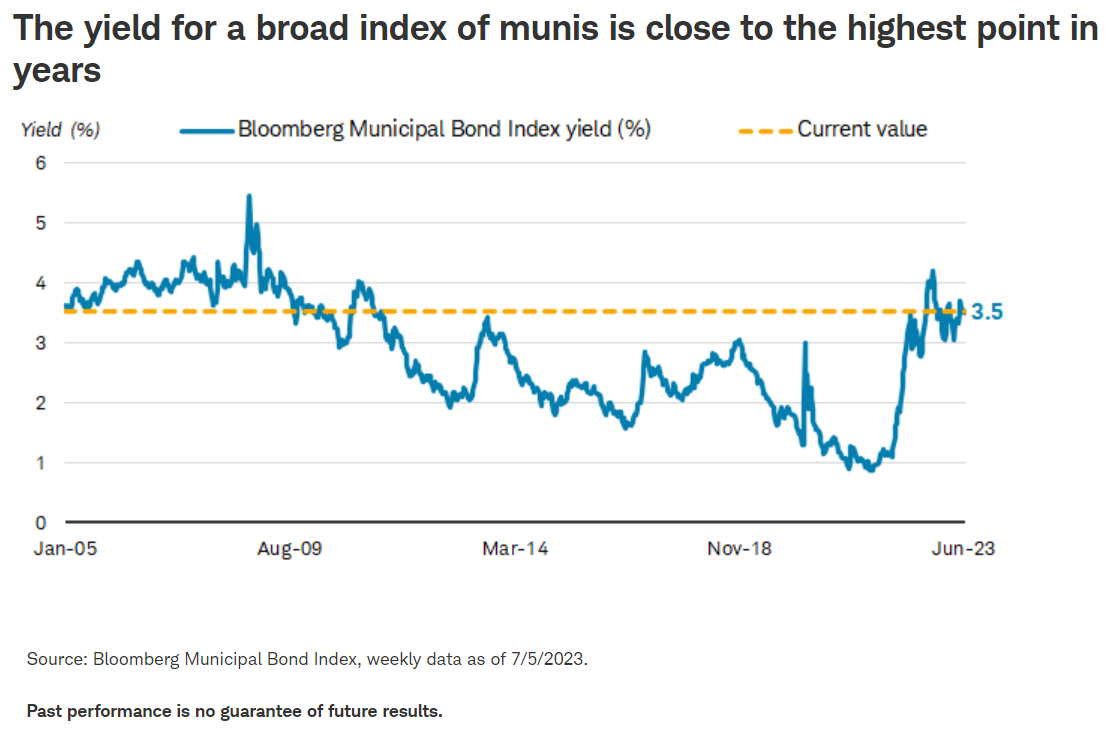

Just two years ago, the yield for a broad index of muni bonds was 1%, which was near the lowest level in the history of the index.1 In dollars and cents, it would take a portfolio of $1 million to generate $10,000 of interest income. An investor would need a very sizeable investment for not much income. That's no longer the case today. Since the trough in July 2021, yields have increased to above 3.5%. To generate the same $10,000 of interest income, an investor would now need a portfolio of roughly $280,000. While it's still a large amount, it's far less than $1 million.

Municipal bonds are issued by cities, states, and local governments and most pay interest income that is exempt from federal and potentially state income taxes. While 3.5% isn't as high as the yield offered by other fixed income options, municipal bonds are one of the few investment options that are often exempt from federal and potentially state income taxes (if the issuer is located in your home state), so after adjusting for this, they are attractive relative to alternatives.

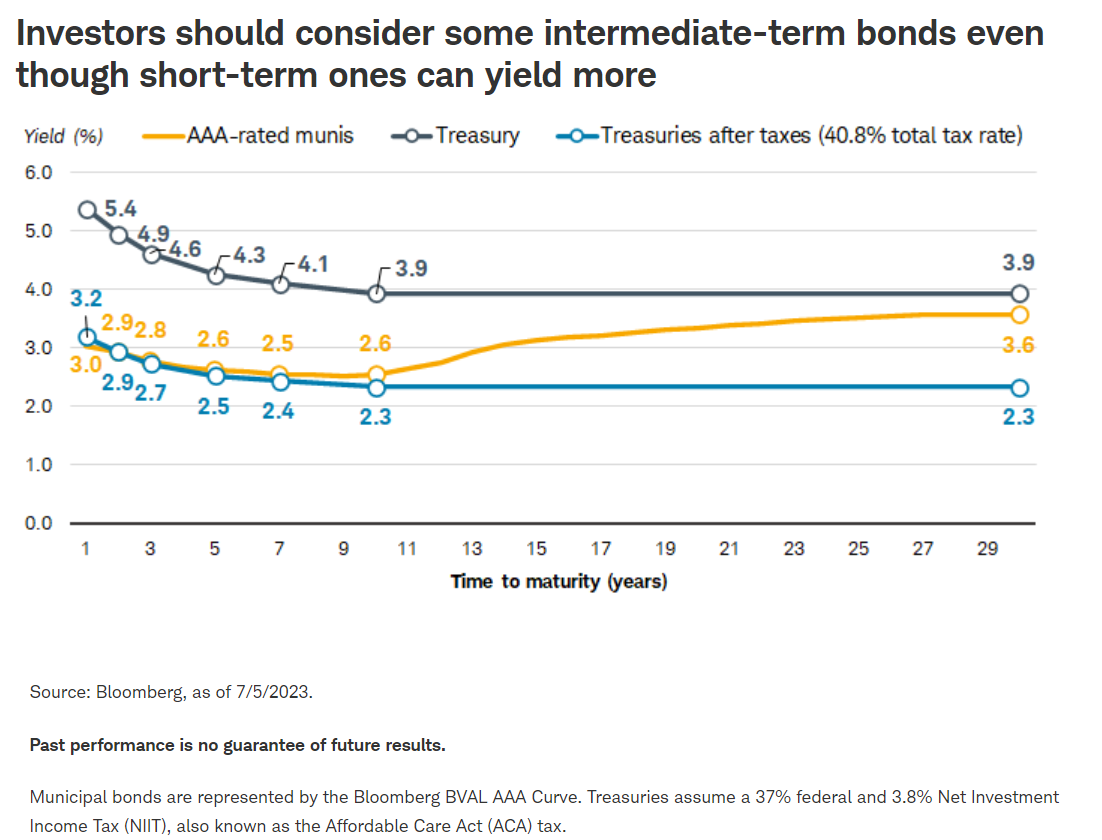

We like the intermediate part of the yield curve

We often hear from clients, "why should I invest in intermediate-term bonds if I can get the same or an even higher yield with shorter-term bonds?" The answer is simple: "reinvestment risk." By purchasing some longer-term bonds, investors are locking those yields in rather than staying in short-term bonds and being more subject the changes in interest rates. For example, a one-year general obligation AAA rated muni yields about 3%, whereas a similarly rated five-year muni yields 2.6%.2 In one year, when the one-year muni matures, an investor would be faced with the possibility of reinvesting at a rate that's lower, whereas the investor in the five-year muni has locked in a yield of 2.6% over the life of the five-year bond.

We don't have major concerns about credit quality for most muni issuers

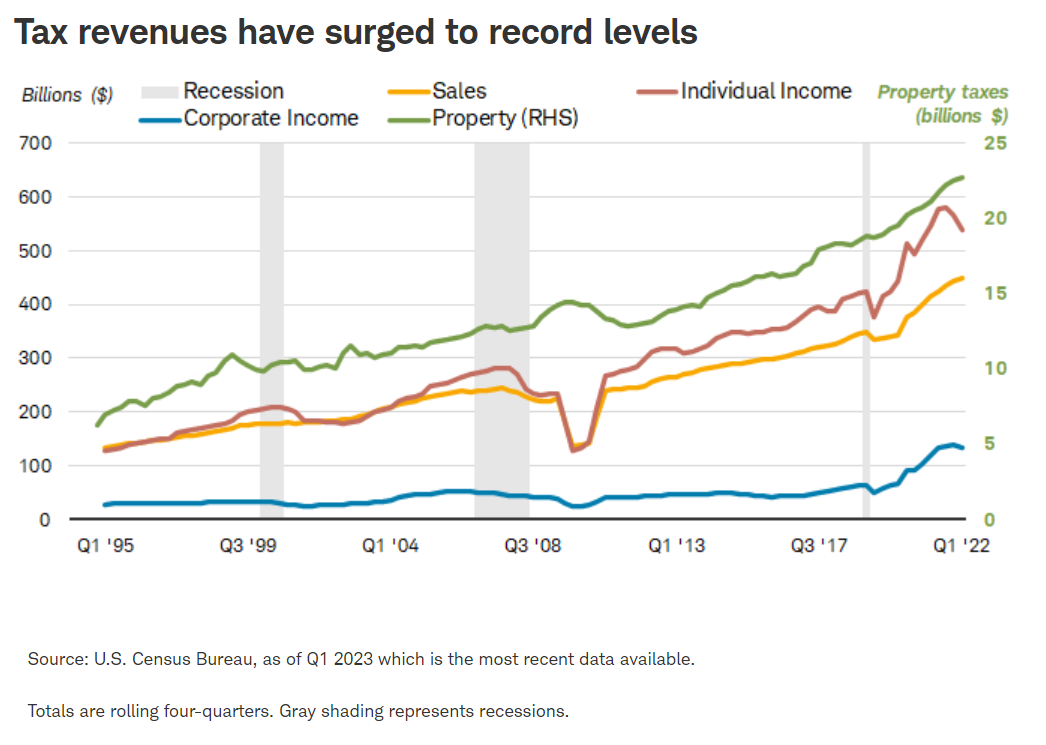

There are signs that the strength in credit quality for state and local governments is beginning to slow, but that isn't a major risk in our view. State tax revenues are near record level highs because of the fiscal aid in response to the COVID-19 pandemic as well as continued strength in the economy. This has allowed many states to build up their reserve levels to record levels and are therefore in a strong financial position to weather a decline in revenues.

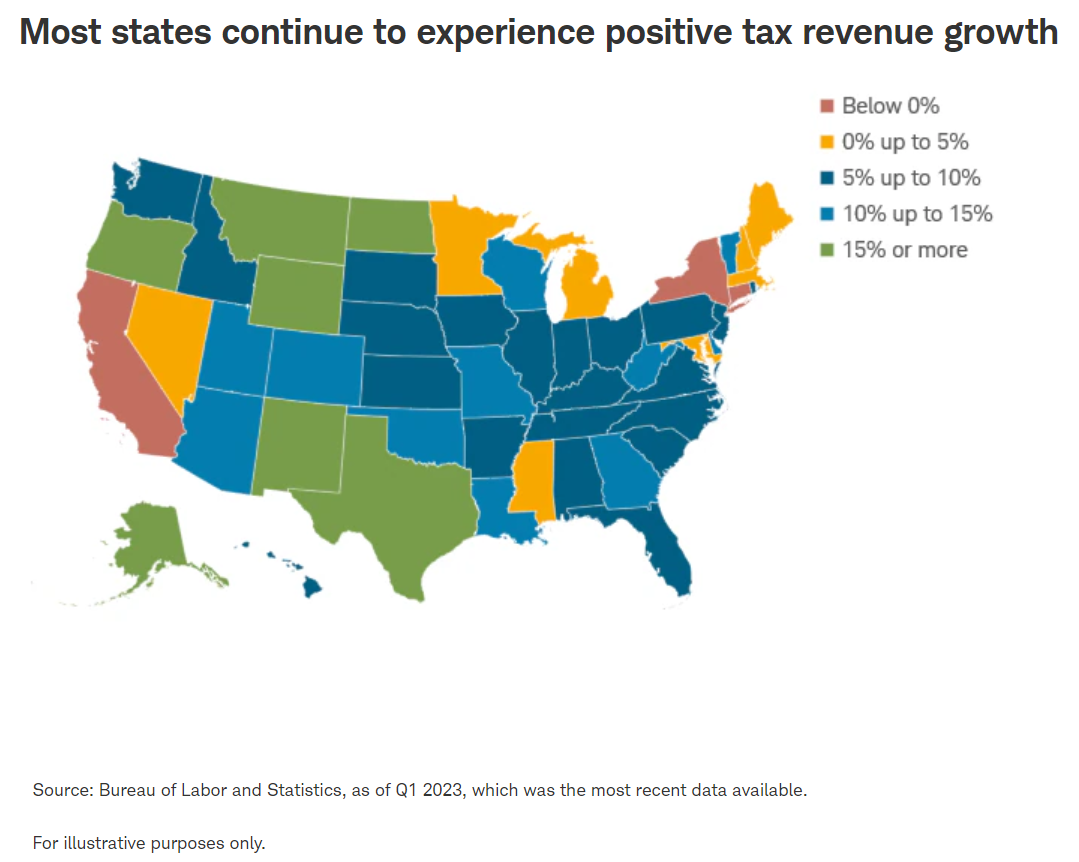

Although credit quality is high, we believe that we are past the peak for muni credit quality. If the economy continues to experience below-trend growth, the pace of growth for state and local government tax revenues should continue to slow, too. The slowdown in tax revenues likely won't lead to an increase in defaults or downgrades, but the pace of upgrades should slow. The slowdown in tax revenues is already starting to happen in states with a higher reliance on revenue sources that are more tied to economic growth. For example, both the state of New York and the state of California derive more than 70% of their tax revenue from corporate and income taxes. Tax revenues have fallen 3.3% for New York and are down 9.5% for California.3 Again, we don't believe this poses a major risk, because most states are already on a very strong financial footing.

We suggest sticking with investment-grade issuers, but take risks cautiously

Although we don't have major concerns about credit quality, we don't believe that lower-rated bonds are attractive now. Generally speaking, lower-rated bonds are more attractive when risks about credit conditions are low, but we believe that investors will be better suited by focusing more on higher-rated investment-grade issuers like those in the AA/Aa category or above. We think investors with a greater tolerance for risk could also consider some bonds in the A/A category, but would suggest caution with BBB/Baa rated issuers. We believe they should account for only a small portion of your overall muni portfolio, if you have the risk tolerance for it.

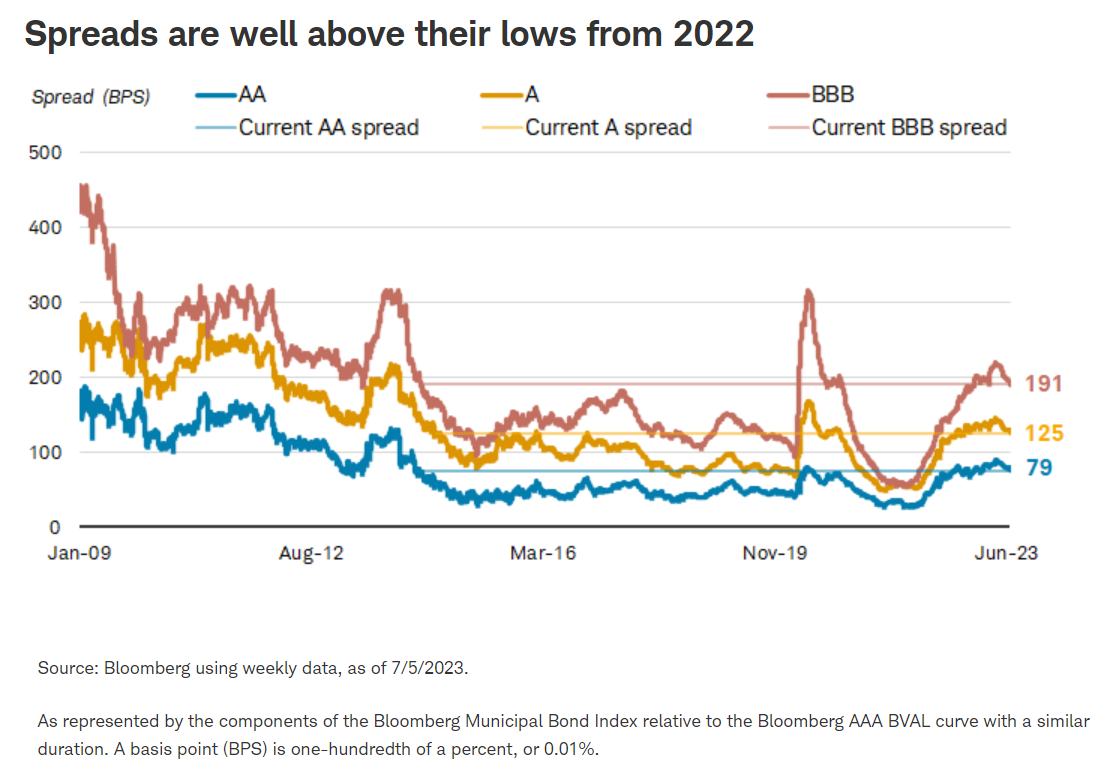

One reason why we suggest staying up in credit quality is because spreads (the additional yield for taking on credit risk) have increased, so investors don't need to target the lowest rungs of investment grade to get higher yields. In other words, at the beginning of 2022, the average BBB-rated bond only yielded roughly 1.5%, which is about 0.5% more than the average AAA-rated muni.4 Today, the average A-rated muni yields roughly 3.9%, which is roughly 1.3% more than the average AAA-rated muni. In other words, investors are now being better compensated for taking on less credit risk than they were at the beginning of the year. Spreads have pulled back recently, but they are still attractive relative to their longer-term average, in our view.

A recession doesn't pose a major risk to most muni issuers

Even if the economy slows over the second half of the year and enters a recession, we believe that the credit quality of most muni issuers should continue to remain strong. Over 70% of the munis in the Bloomberg Municipal Bond Index are either AAA or AA rated, which are the top two rungs of the credit rating scale. Higher-rated issuers usually have more stable revenue sources and stronger liquidity. This strong footing to begin with should allow most issuers to manage through a recession if it does occur.

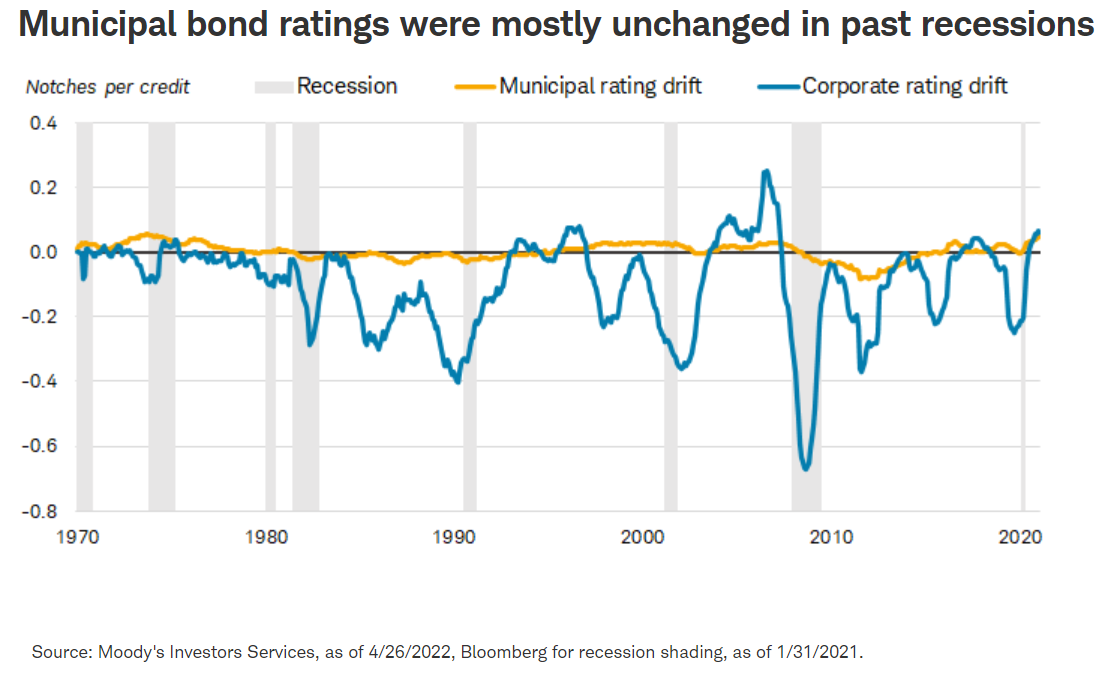

Additionally, the slowdown in tax revenues tends to lag the slowdown in the economy, which allows states and local governments ample time to adjust spending if needed. The combination of a strong starting point and fairly stable revenue sources has translated to stable ratings during past recessions. In past recessions, the ratings for most municipal issuers stayed relatively the same, which is unlike corporate bonds. The ratings drift for municipal bonds is relatively benign when compared to corporate bonds, as illustrated in the chart below. Ratings drift is the average change in credit-rating "notches" for every 100 bonds over the observed one-year period. One "notch," for example, is the incremental difference between AA+ and AA. In other words, in September 2008, the average corporate bond was downgraded 0.7 notches while the average municipal bond's rating was essentially unchanged. This is important because when a bond is downgraded or the market anticipates it may be downgraded, it usually falls in price.

What to do now

It's been an eventful first half of the year for many parts of the market, but not so much for munis. That's a welcome relief because it illustrates that munis are doing what they're generally supposed to do—provide tax-advantaged income with little volatility. Going forward, we expect more of the same for the muni market. We like sticking with higher-rated issuers and focusing on the intermediate part of the yield curve.

Schwab clients can log in to research individual municipal bonds, view pre-screened municipal bond exchange-traded funds (ETFs) on Schwab's ETF Select List® or municipal bond mutual funds on Schwab's Mutual Fund OneSource Select List®. For additional help in selecting an appropriate solution for your needs, a Schwab financial consultant or fixed income specialist can help.

1 Based on the Bloomberg Municipal Bond Index. The low was 0.86 on 7/27/2021.

2 As represented by the Bloomberg AAA BVAL Curve. The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

3 Based on the rolling four-quarter change. As of Q1 2023 which is the most recent data available.

4 As represented by the components of the Bloomberg Municipal Bond Index relative to the Bloomberg AAA BVAL curve with a similar duration.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All