Emerging Markets from the Asset Allocator’s View

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBut the macro outlook includes potential downsides. A strong cyclical slowdown and developed-market recession remain risks, as does a prolonged spell of market volatility. Given the complex macro picture and the combination of wide-ranging valuations, growth outlooks, and fundamentals within EM, we think a nuanced, highly selective active approach makes sense. Today, we see more opportunities within EM than at the overall asset-class level.

Valuations Alone Aren’t Compelling Enough

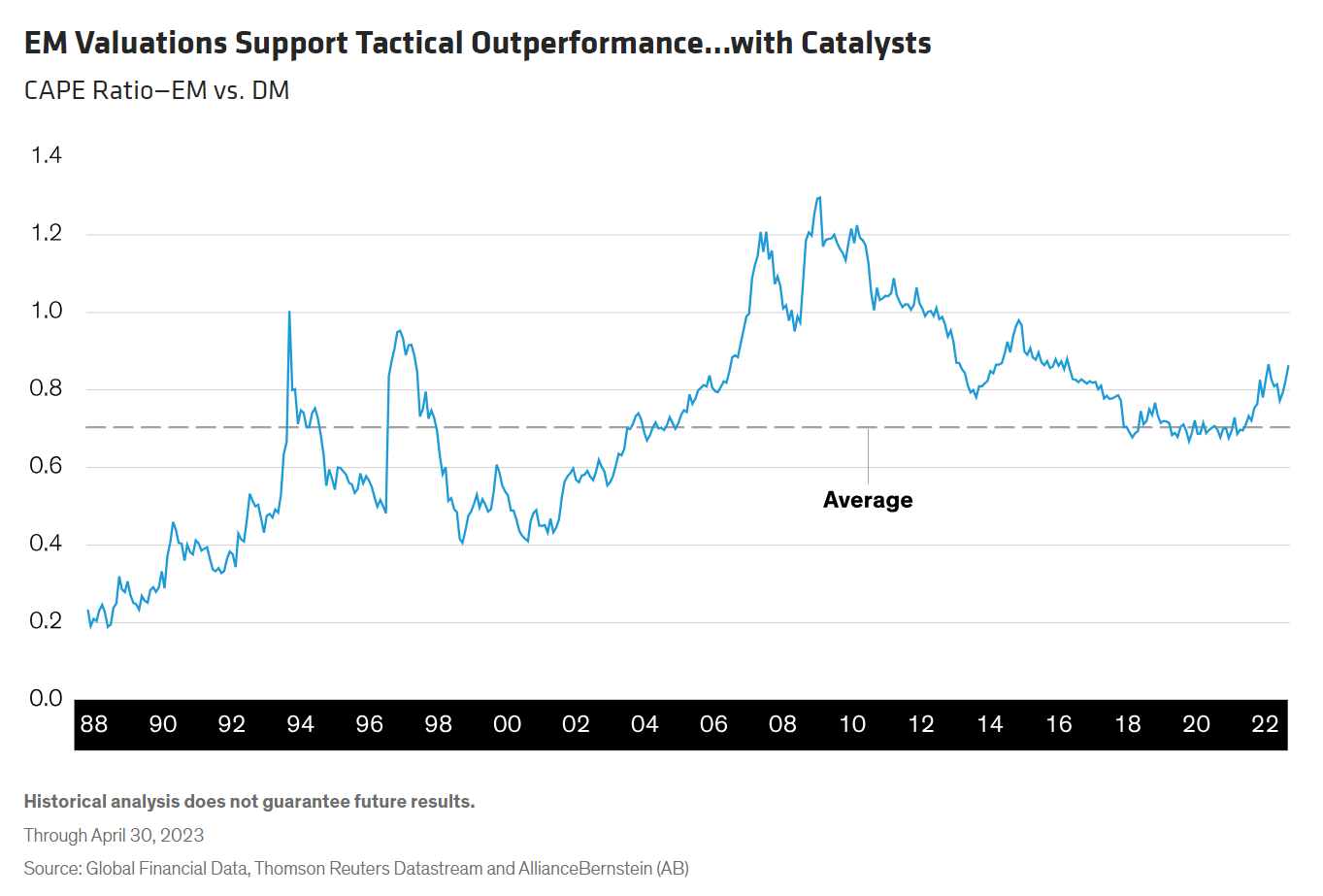

Equity valuations are more relevant over a medium- or long-term horizon, but they’re also tactically important in helping determine an entry or exit point. Measured on a cyclically adjusted price/earnings (CAPE) basis versus developed markets, EM is now trading at 0.86x, reasonably higher than the historical average of 0.71x (Display).

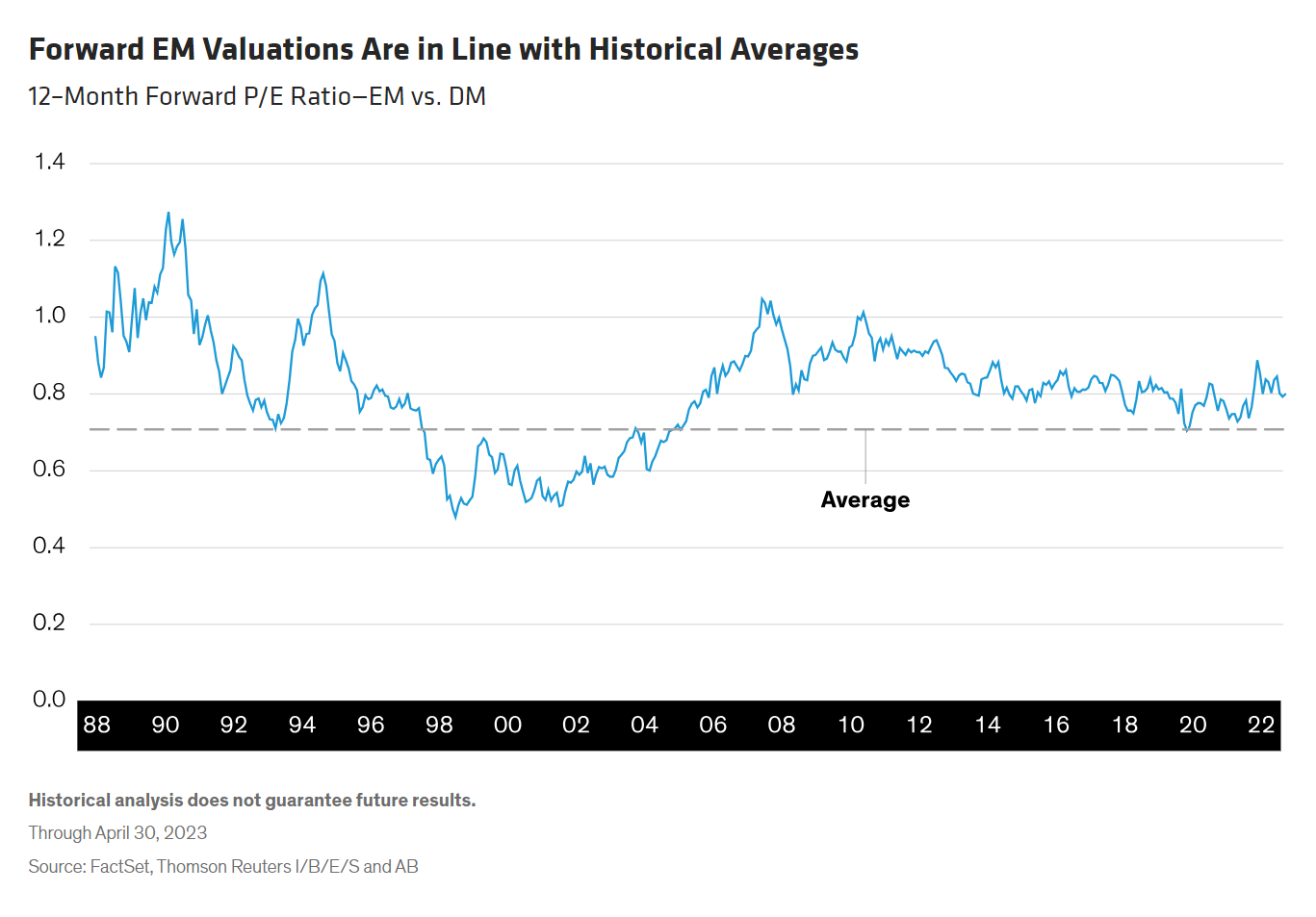

Based on a 12-month forward P/E ratio, EM is currently trading at 0.8x, in line with the historical average (Display).

The current valuation may not present a compelling entry point on its own. However, multiples are at levels where we think EM equities can outperform tactically, if they’re accompanied by positive catalysts such as China’s reopening, slower policy tightening in developed economies and a possible tailwind from US-dollar weakness. But there’s a wide dispersion of regional valuations within EM. For instance, China is trading at a 12-month forward P/E multiple of 12x and Brazil at 8.7x, while India’s multiple is 19.4x.

Investor Sentiment and Positioning Provide Tactical Support

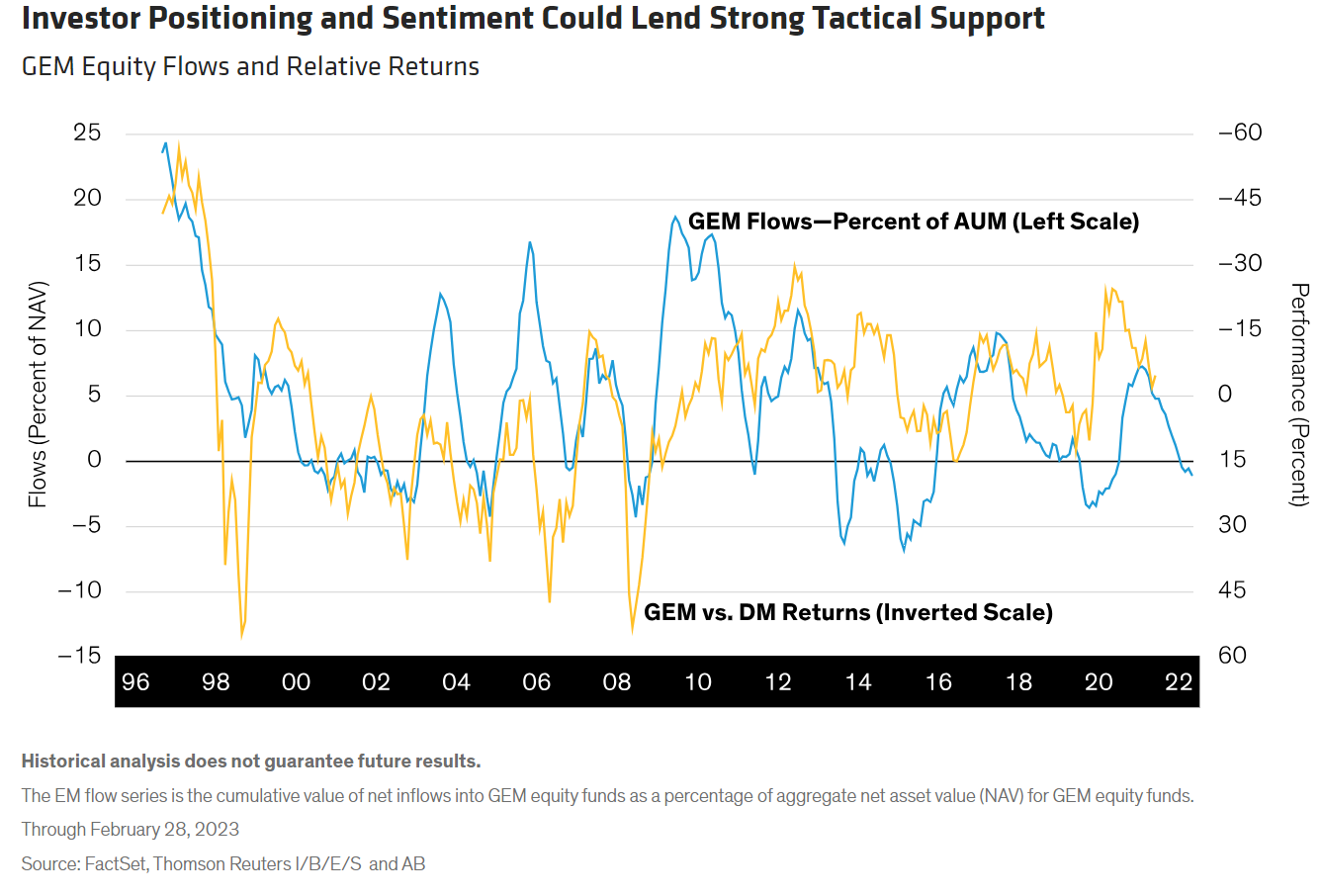

More important, investor positioning and sentiment could provide strong tactical support. Based on our global emerging-market (GEM) equity fund-flow indicator and the link to historical EM versus developed performance, investor sentiment toward EM is currently muted. In the past, similar sentiment levels have been associated with EM outperformance over a 12-month horizon (Display).

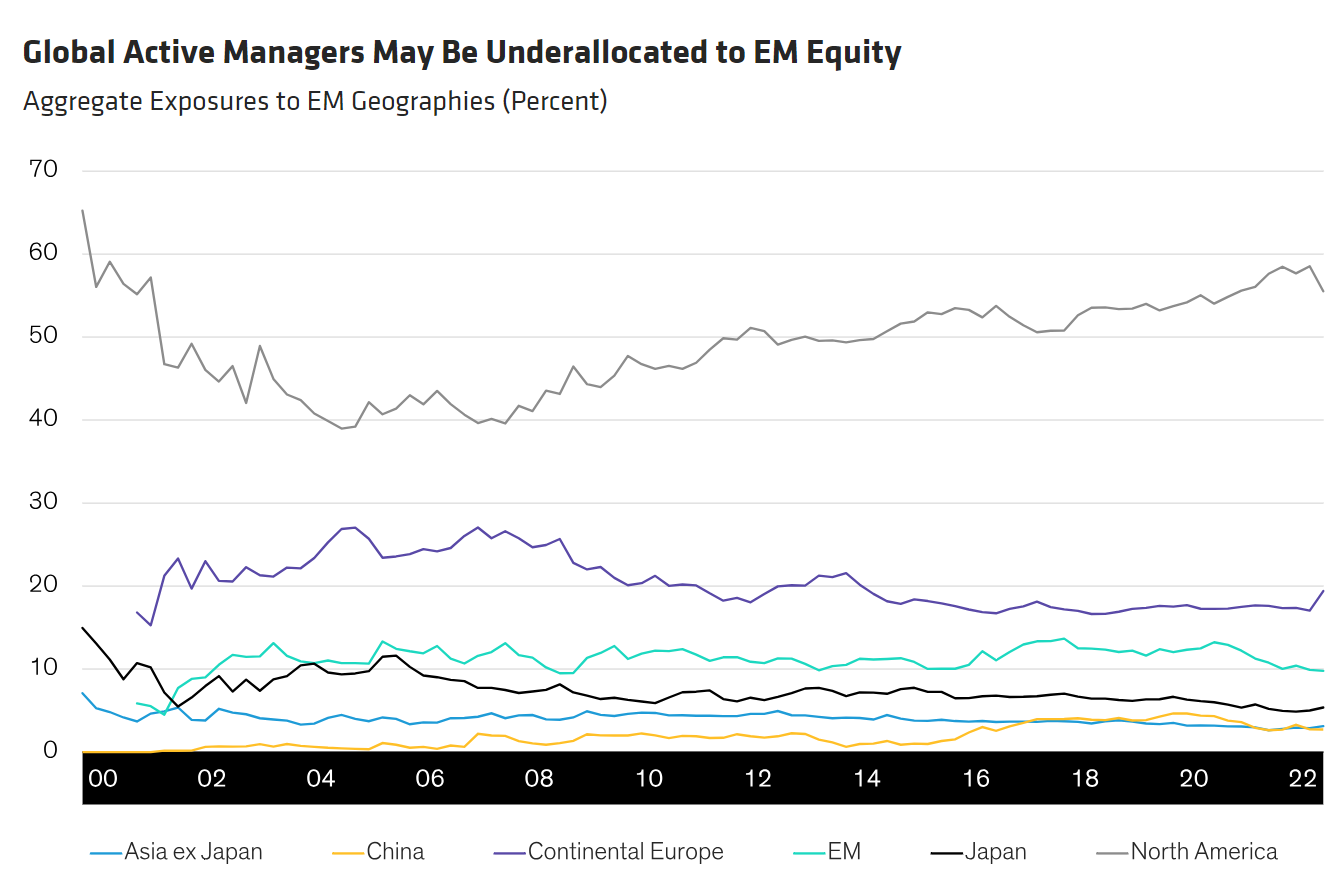

Assessing changes in exposures to different regions can be informative, too. Among our large sample of globally benchmarked active portfolio managers (Display), EM exposure has declined from 13% at the end of 2020 to less than 10%. This positioning suggests that global active managers might be underallocated to EM, with scope to increase their exposure.

The Macro Picture Is Complex

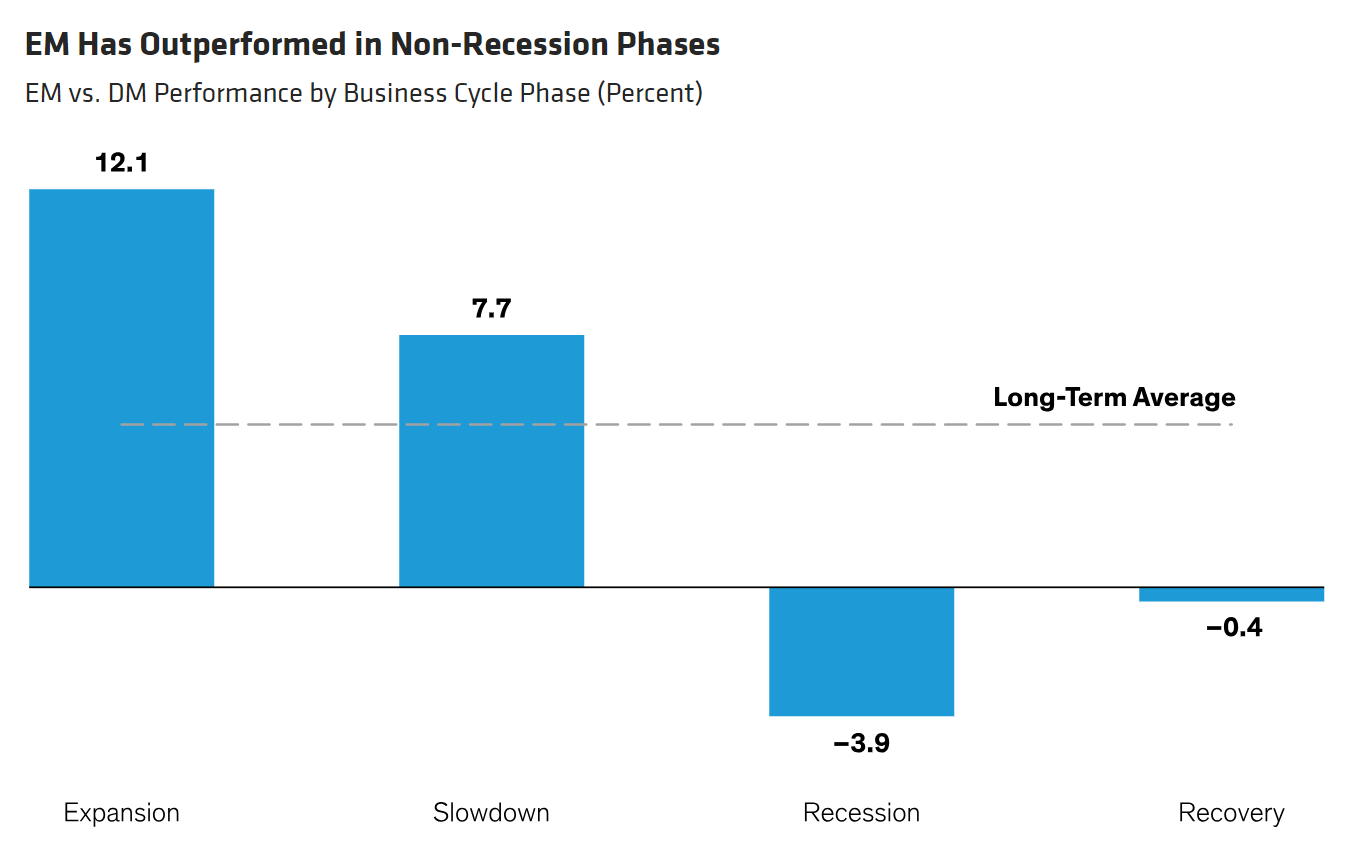

The global business cycle is a key influence on EM’s relative performance, as we can see when assessing returns in different phases of the cycle (Display). EM has underperformed developed-market stocks during recessions (trailing by nearly 4%) but outperformed in periods when an economic slowdown didn’t turn into an outright recession, with a 7.7% leading margin.

While recession remains a clear risk in developed markets, the International Monetary Fund (IMF) expects global real gross domestic product (GDP) to grow by 2.8% in 2023. This rate is down from 3.4% in 2022, indicating a slowdown. But a global recession isn’t the current base case in most economic forecasts, and most of the projected weakness will come from the US and Europe.

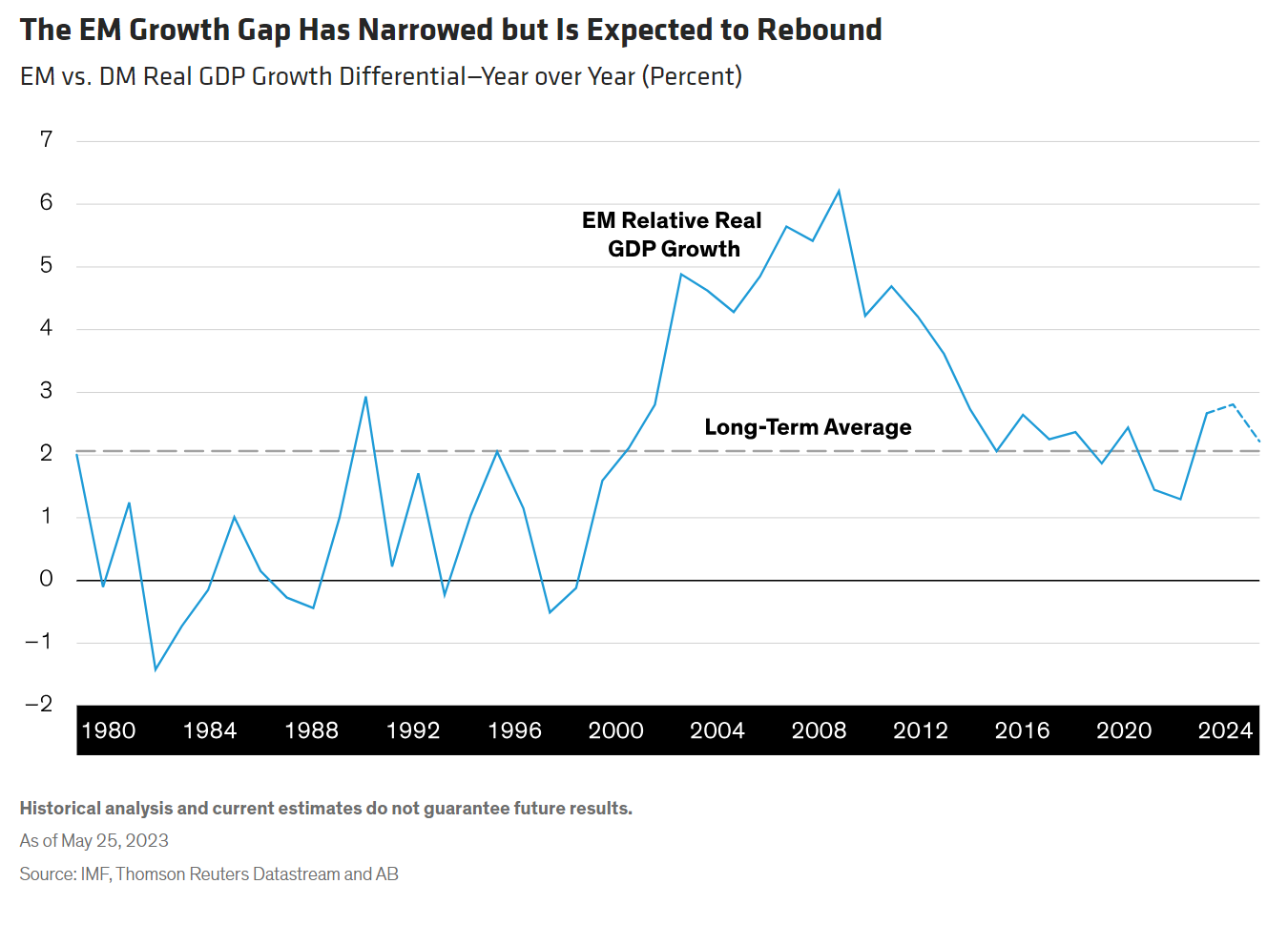

The economic-growth gap between EM and developed markets narrowed substantially in 2022. However, according to IMF projections, EM growth is expected to rebound in 2023, with the EM versus developed-market growth gap widening to above historical average in 2023 and 2024 (Display).

Within EM, Asian economies (notably China and India) are expected to drive most of 2023’s global growth, as they benefit from the ongoing dynamics of China’s reopening and face less intense inflationary pressures than other parts of the world.

The Impact of Interest Rates Can’t Be Gauged in Isolation

The direction of US and global interest rates is another significant macro driver: the relationship between relative EM and developed-market performance and the US fed funds rate has tended to be negative. Rising US rates increase EM debt burdens, trigger capital outflows to higher-yielding and safer US assets, and tighten financial conditions in EM. In extreme cases, this situation has triggered financial crises.

The Fed is still in policy-tightening mode, but the pace of tightening has slowed, given the fallout from the recent banking-sector turmoil. The central bank has signaled that only one more rate hike is left in the queue, so an end is in sight for the US tightening cycle and should remove a key headwind while supporting relative EM performance.

However, the impact of interest rates shouldn’t be judged in isolation, with the US-dollar outlook as a particularly important consideration. A stronger dollar increases the burden of EM foreign currency–denominated debt obligations, makes it harder to finance current-account deficits, and may lead policymakers to raise rates to prevent capital outflows. These factors can hurt economic growth and equities.

Since its September 2022 peak, the trade-weighted US-dollar index has fallen by more than 9%. If this weakness lasts, it could be another catalyst for EM outperformance. On the other hand, if worries about credit availability in the US remain, or if we see a bout of macro volatility, the US dollar would benefit from its status as the most liquid currency and historical reputation as a “safe haven” in times of crisis.

Many EM central banks face lower inflationary pressures, giving them latitude to do less tightening or perhaps no additional tightening, but they’re vulnerable to a sudden US-dollar liquidity shortage, which could weigh on their currencies. Depending on how financial-stability risks evolve, they could also prompt still more hikes from many of these central banks in the months to come.

Overall, we see macro risks as finely balanced. The near-term cyclical outlook is a source of downside risk but doesn’t necessarily imply a bearish outlook for EM. The monetary cycle in the US and the dollar outlook could prove supportive but have potential downside risks, too.

Where Are the Opportunities in EM?

Given wide-ranging valuations, growth outlooks, inflationary pressures and vulnerabilities to macro risks within EM, an active and selective approach is needed. We can highlight several themes we think are promising, including countries that:

- Are “ahead” of other economies in the policy-tightening cycle (Brazil, Mexico)

- Have contained or declining inflation rates (China, Indonesia)

- Have seen multiples and earnings expectations adjust enough to be well positioned for a rebound (China, Indonesia, Brazil)

- Are well positioned for the net zero transition and/or benefiting from the reconfiguration of global supply chains (Brazil, Mexico, India, Indonesia)

China Should Be Considered a Distinct Building Block Within EM

From a strategic perspective, we also believe that China should be considered a distinct building block within an investors’ EM allocation. What’s the main reason for this view? The investment approach needed to form a view on China is increasingly different fundamentally than it is for other EM markets.

To a very large extent, the China view depends on President Xi’s policy. Given the overriding influence of his ideology on China’s structural strategy and outlook, getting the correct read of his policies is paramount. Making a beta call on this market is challenging, even over a shorter investment horizon.

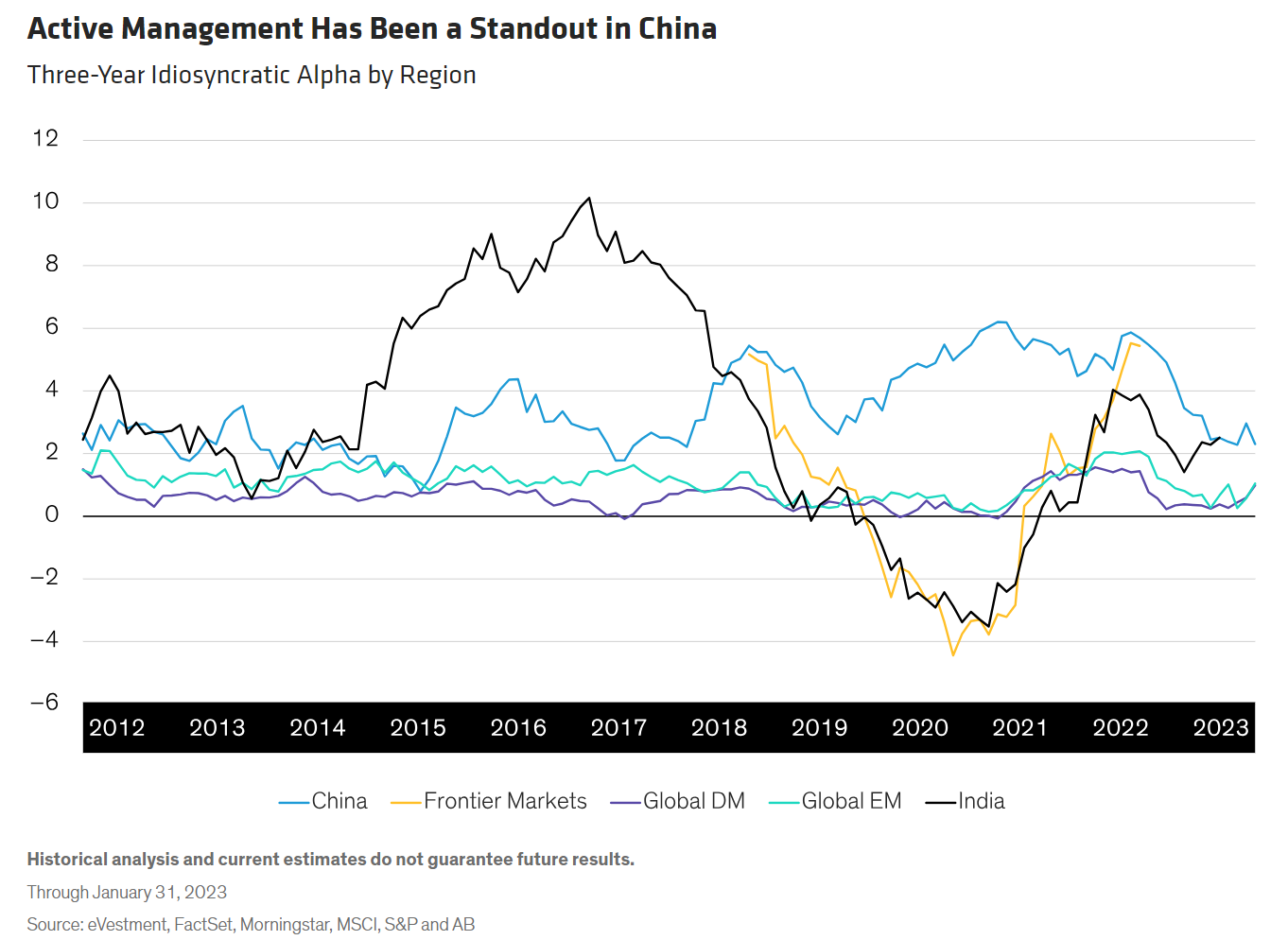

Another distinctive feature of China is that active management has long been a standout in alpha generation among other regions. The active industry has been under pressure and performance has suffered, but equity managers with China benchmarks continue to generate positive idiosyncratic alpha—alpha adjusted for common factor exposures—in excess of other key regions (Display).

We think China remains an area of great opportunity for active investing, although it’s important to be highly selective in choosing both managers and securities. If investors approach China thoughtfully, we think it offers access to superior active alpha opportunities and can be an effective diversifier in many portfolios. You can find more detailed views on strategic opportunities in China from our equity teams.

Alla Harmsworth is Co-Head of Institutional Solutions and Head of Alphalytics at AB. She was previously head of European Quantitative Strategy at Bernstein Research. Prior to joining Bernstein in 2015, Harmsworth worked for two years on Nomura's Institutional Investor-ranked European Equity Strategy and Quantitative Strategy team. Her previous experience includes seven years at Fidelity as a quantitative analyst and portfolio manager, along with stints at Nikko Asset Management and ABN AMRO. Harmsworth holds a BA (Hons) and an MA in philosophy, politics and economics from University College Oxford and an MSc in economics from the London School of Economics and Political Science. Location: London

Robertas Stancikas is a Vice President and Senior Research Associate on the Institutional Solutions team at AB. He was previously a senior research associate on the Global Quantitative Strategy team at Bernstein Research. Prior to joining AB in 2015, Stancikas was part of Nomura Securities’s Global Quantitative Strategy and European Equity Strategy teams. He holds a BSc in economics and industrial organization from the University of Warwick and is a CFA charterholder. Location: New York

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All