El Niño Could Bring Storms to the Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsA high probability for an El Niño event in the second half of 2023 brings concerns of extreme weather, persistent inflation, supply chain disruptions, and market volatility.

Weather rarely has a material impact on overall markets. But that could change in the coming quarters as the potential for extreme weather heightened by El Niño could cause significant economic disruptions. The World Meteorological Organization has announced a 90% probability of an El Niño event in the second half of this year. This phenomenon refers to a warming surface of the Pacific Ocean that can cause shifts in both temperature and weather patterns. Extreme heat is already being felt with the hottest week on record for the entire planet at the beginning of July, following the hottest June on record according to the World Meteorological Organization. Fierce heatwaves are being felt across the globe, including one last week that dried up some of Europe's main rivers, threatening supply chains and energy supplies.

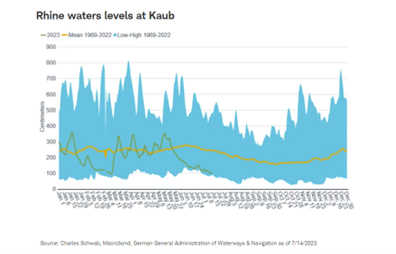

- In Germany, the Rhine at Kalb fell below 100 centimeters, making the river potentially impassable for most barges carrying industrial products and coal.

- In France, the Rhone has been too warm to cool nuclear reactors for Electricite de France, leading to shutdowns and lower output.

- In Eastern Europe, the Danube at Budapest is down to 135 centimeters, threatening a key Ukrainian grain transport route.

Extreme weather has had impacts in the U.S., Canada, and South America in recent weeks:

- Forecasters extended an excessive heat warning through the weekend for Arizona's most populated area and alerted residents in parts of Nevada and New Mexico to stay indoors.

- The Canadian Ministry of natural resources said the number of wildfires in the country was "off the charts" with a long and difficult summer ahead. Smoke from the fires so far this season has polluted the air in Canada and the U.S., affecting more than 100 million people.

- Shifting weather patterns has meant heavy rainfall in Chile, disrupting the country's copper mining industry, its primary export.

If these impacts continue to threaten agriculture, energy, and lives, or worsen—as forecasters expect—the economic impact could be significant for both inflation and economic activity.

Higher inflation

While core inflation in major economies has remained stubbornly high, headline inflation—which includes food and energy—has declined, easing concerns over high prices as it has trended downward. However, the inflation impacts of extreme weather are likely to be concentrated in food and energy, potentially pushing overall inflation higher in the coming months.

- Energy inflation could be boosted by low water levels in reservoirs, curtailing hydropower generation, adding to the strain on power supplies, and putting upward pressure on gas and coal prices. Energy demand may also rise due to higher air conditioning needs.

- Freight transportation costs, including fuel, may rise if river transport must be shifted to trucking and rails.

- Higher food prices could result from both poor crop yields due to drought as well as increased fuel costs needed for harvest and transportation. Already, rice prices are the highest in more than two years, per futures prices on the Chicago Board of Trade, a result of importer stockpiling as El Niño-related supply concerns intensify in Thailand and Vietnam.

More rate hikes

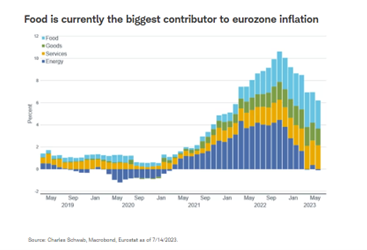

Some central banks may need to keep rates higher for longer to combat inflation should high food prices persist, particularly in emerging and frontier markets. Food prices have been a major contributor to high inflation in the Eurozone, as you can see in the chart below. Food also makes up over 50% of the CPI in India, and closer to 20% in China versus only 13% in the United States. High food prices could filter through to wages if they persist, which could sustain core inflation at higher levels, and result in data-driven central banks to keep monetary policy tight.

Potential unrest

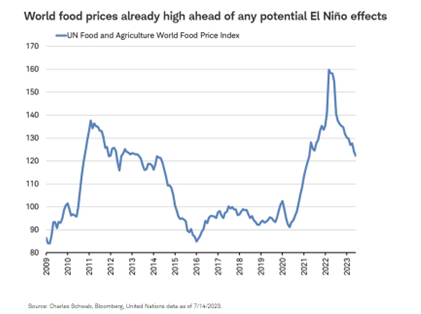

Economic disruption can also result from geopolitical unrest fueled by high food prices as seen in the Arab Spring in 2011. Higher food prices and unemployment, along with economic stagnation and corruption, were on the minds of demonstrators when protests erupted in Tunisia and spread to Egypt, Libya, Yemen, Syria, and Bahrain in early 2011. These protests resulted in the toppling of several governments and civil wars in the region. Food prices are already elevated and not far from the levels seen in 2011 (as you can see in the chart below) ahead of potential El Niño effects. In emerging and frontier market countries, food tends to make up a larger share of consumer spending.

In addition, agriculture accounts for a larger share of GDP and employment in Africa and South Asia than in other parts of the world. Therefore, these regions are particularly vulnerable to a strong El Niño: declining cocoa production in Côte d'Ivoire and Ghana, sugar production in India and Thailand, coffee production in Vietnam and Indonesia, and rice production in Vietnam and Thailand could mean weaker GDP in these countries. Weaker economic output could translate to economic stagnation and fewer jobs. Unrelated to potential unrest, a sharp reduction in the volume of crops that can be exported could result in debt strains for some economies.

Financial effects

Record-level sea surface temperatures have led to an early start for the 2023 hurricane season in the Atlantic. On July 6th, Colorado State University updated its forecast for the hurricane season to "above normal," predicting the probability of landfall of at least one major storm at 50% for the eastern U.S. coastline, an upgrade to their 44% probability given in April. A research paper from the Scripps Institution of Oceanography at the University of California, focusing on the Western U.S., revealed that 1% of extreme events caused over 66% of total losses for insurance companies noting that, "Connections between extreme events and El Niño are borne out in the insurance data. In coastal Southern California and across the Southwest, El Niño conditions have had a strong effect in producing more frequent and higher magnitudes of insured losses." On the other side of the Pacific, El Niño effects bring hotter, drier, and more settled conditions that may result in fewer insurance losses in Australia and Asia's Pacific rim.

Market impact

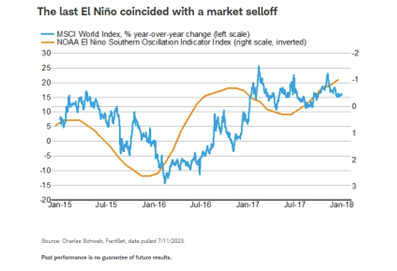

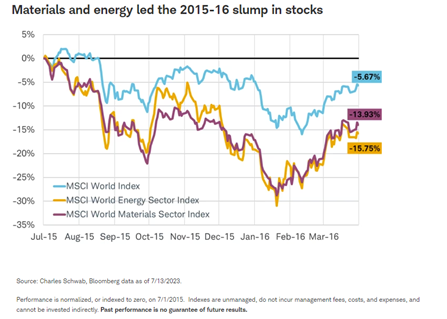

Market volatility could increase if El Niño impacts accumulate. The last El Niño coincided with the market selling off 13% in 2015-2016, although other factors likely contributed to the volatility. However, the impact on the market appeared to be relatively short-lived.

During El Niño events, sectors like agriculture and energy typically experience increased volatility due to weather patterns impacting crop production and energy consumption. The El Niño event in 2015 was one of the strongest on record, and lead to significant weather disruptions. Unsurprisingly, the material and energy sectors led the slump in the global stock markets in late 2015 and early 2016.

Storms on the horizon

Extreme weather heightened by El Niño could bring market volatility, should history repeat itself. El Niño may result in disruptions to food production, impact the movement of goods and price of energy, cause hurricane losses for insurance companies, create geopolitical unrest, and keep rates higher for longer in some countries—particularly in emerging markets. Weather of course is difficult to forecast—as are markets—but the potential impacts are worth considering by investors.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Commodity-related products, including futures, carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions, regardless of the length of time shares are held. Investments in commodity-related products may subject the fund to significantly greater volatility than investments in traditional securities and involve substantial risks, including the risk of loss of a significant portion of their principal value.

Futures and futures options trading involves substantial risk and is not suitable for all investors. Please read the Risk Disclosure Statement for Futures and Options prior to trading futures products.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research, and are developed through analysis of historical public data.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

The UN Food and Agriculture Organization World Food Price Index (FFPI) is a measure of the monthly change in international prices of a basket of food commodities, consisting of the average of five commodity group price indices weighted by the average export shares of each of the groups during 2014-2016.

The NOAA El Nino/Southern Oscillation Indicator Index (ENSO) is a measure of the fluctuation in sea surface temperature and the air pressure of the overlying atmosphere across the equatorial Pacific Ocean.

The MSCI World Energy Index is designed to capture the performance of the large and mid-cap segments across 23 Developed Markets (DM) countries in the Energy sector as per the Global Industry Classification Standard (GICS®).

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All