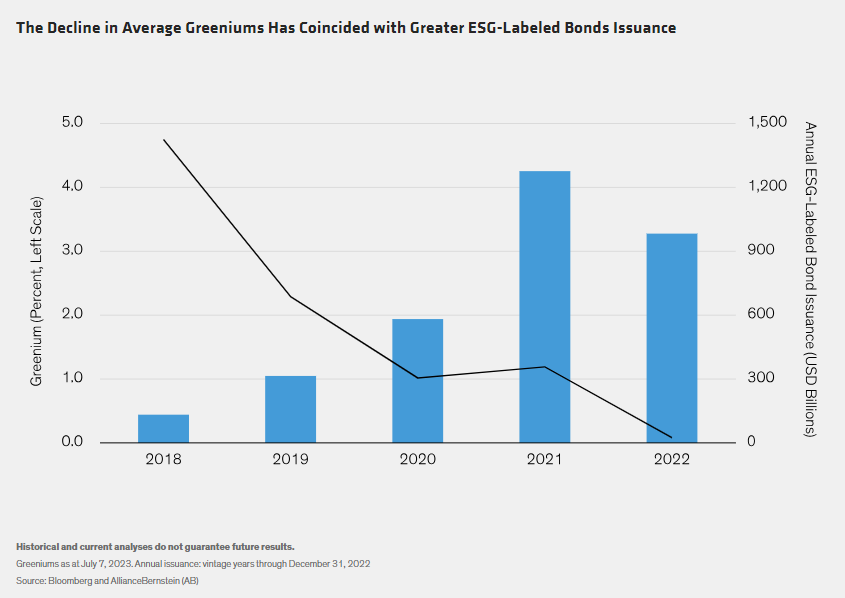

Investors in ESG-labeled bonds expect well-structured issues with strong green or social credentials to command higher prices than the same issuer’s conventional bonds. This price premium, known as the “greenium,” seems to have been shrinking over time (Display). But factor in metrics such as quality and volume of issuance per vintage year, and a more nuanced picture emerges.

Although it’s common knowledge that the average greenium across major bond indices has decreased in recent years, the significance of issuance year (vintage) for greeniums is less well understood. But the vintage year is important because both the issuance levels of ESG-labeled bonds and the quality of their ESG proposition have varied significantly over time.

The decline in average greeniums has been driven primarily by two related factors: the increased issuance of ESG-linked bonds and the coinciding decline in the quality of the ESG proposition across many of the newer issues. We can see the changes in both factors more clearly when we analyze vintage years.

We find that many older ESG-labeled bonds issued in the 2018–2019 era have maintained their greeniums over time. These include issues from pioneering financial institutions and best-in-class European names.