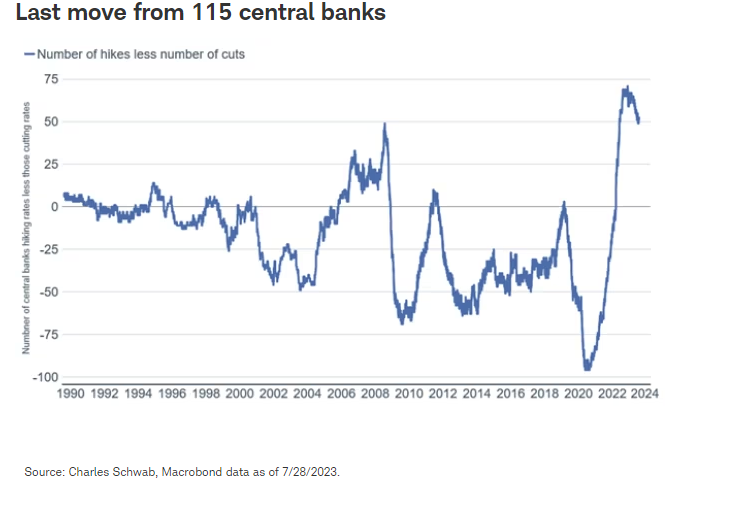

Divergence: Rate Cuts, Pauses, and Hikes

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsCentral bank policies are set to diverge from the steady hikes characterizing the first half of 2023, contributing to increased market volatility for the remainder of the year.

The rate hike cycles for the biggest central banks, the U.S. Federal Reserve and the European Central Bank (ECB), appear to be over. Last week's meetings by the Fed, ECB, and Bank of Japan (BOJ) revealed important policy changes that may continue to impact markets in the months to come. This week, other central banks will be cutting, pausing, or hiking rates. Central bank policy is now diverging, with the Bank of Brazil and other emerging-market economies expected to start cutting rates, joining the People's Bank of China in a more accommodative monetary policy. In contrast, the Reserve Bank of Australia is on pause and the Bank of England is likely to continue to hike rates.

Bank of Japan

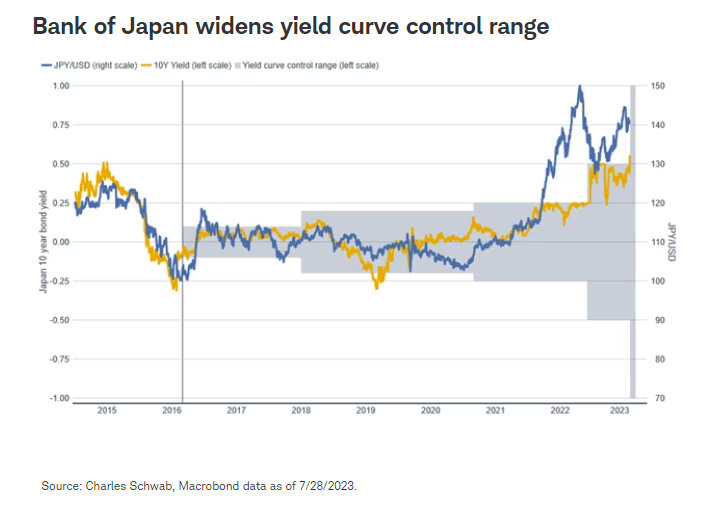

As we wrote in February (Are You Focusing on the Wrong Central Bank?), the anticipated policy changes that BOJ was likely to make over the next six to nine months may affect the markets. Last week, the BOJ tweaked its yield curve control (YCC) policy, shifting from a hard cap on the 10-year Japanese government bond (JGB) yield at 0.5% to instead offering to buy 10-year bonds at 1.00%. Their remarks stated that 0.5% is now a reference point and not a ceiling. This adds yet another step in the BOJ's end to its easy monetary policy. Global stocks, bonds and currencies could be volatile as a result.

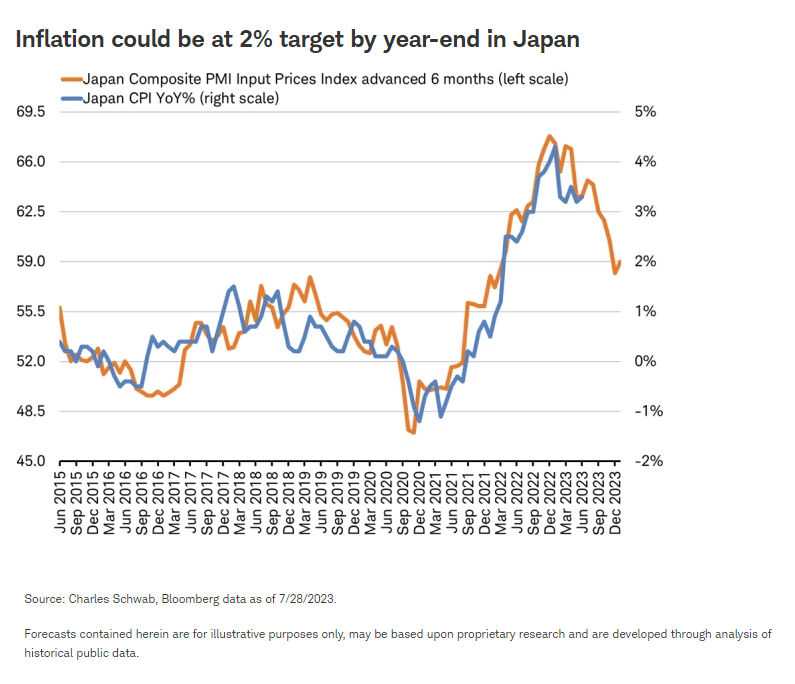

However, the BOJ is not yet convinced deflation is no longer a concern. While inflation is above its 2% target now, inflation in Japan may recede quickly if it continues to track the Purchasing Managers' Index (PMI) input prices index, which has tended to lead the consumer price index (CPI) in Japan by six months, as you can see in the chart below.

A popular strategy, the yen carry trade takes place when investors borrow yen at a low-interest rate and exchange that currency to purchase investments in a country that pays a higher rate of return. Now, this trade generally works if exchange rates remain stable. But should the value of the yen increase on prospects for higher interest rates in Japan, carry traders would need to spend more dollars or euros to pay back the yen initially borrowed, reducing any potential return. If the rise is significant enough, investors could go bankrupt if they don't act swiftly to mitigate losses. Should the carry trade unwind too quickly, it could lead to outsized cross-market volatility.

Because of the prevalent low rates in Japan for the last two and a half decades, Japanese investors participated heavily in this strategy to become the biggest non-U.S. holders of U.S. Treasuries and foreign stocks. A stronger yen and higher JGB rates may bring back money to Japan from the rest of the world as investors unwind these trades. The sale of assets in non-Japanese markets may cause stocks to sell off, global bond yields to rise, and non-yen currencies to fall. The yen has already appreciated 2% in July as markets anticipated the move by the BOJ.

Japan's stock market has been the best-performing developed market this year with a gain of 27%, but the drop in the yen versus the dollar has reduced this year's total return to U.S.-based investors to 18%. A lift in the value of the yen could further support returns on Japan's stock market. We previously discussed the reasons Japanese stocks have attracted investors this year in Japan: Reclaiming Lost Decades. Japanese stocks are trading below their long-term price-to-earnings (PE) ratio, despite the Nikkei surge this year bringing it close to a 33-year high.

European Central Bank

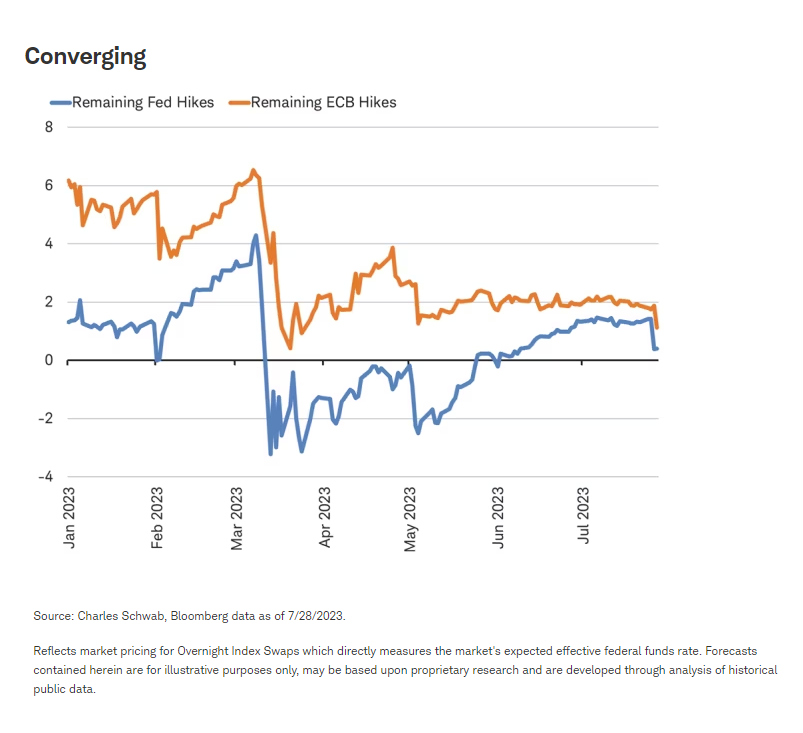

In June, the ECB delivered a hike with a clear commitment to do more. But just last week, the central bank surprised markets by signaling the July rate hike may be its last. The overnight index swaps (OIS) market moved to price in convergence with the outlook for Fed rate hikes. At the press conference following last Thursday's meeting, ECB President Lagarde said that "We might hike, or hold, but we won't cut," at the September meeting, while reaffirming that the decision is data-dependent.

We believe the incoming economic data over the next six weeks—including Friday's GDP and the inflation readings—will likely persuade the markets to further reduce the probability of a September hike.

- Last week, our favorite leading indicator for Europe's economy, the composite PMI, decreased by one point to 48.9 in July on the back of a broad-based decline across sectors and countries. The reading was both below consensus expectations and the 50-level that marks the threshold between growth and contraction.

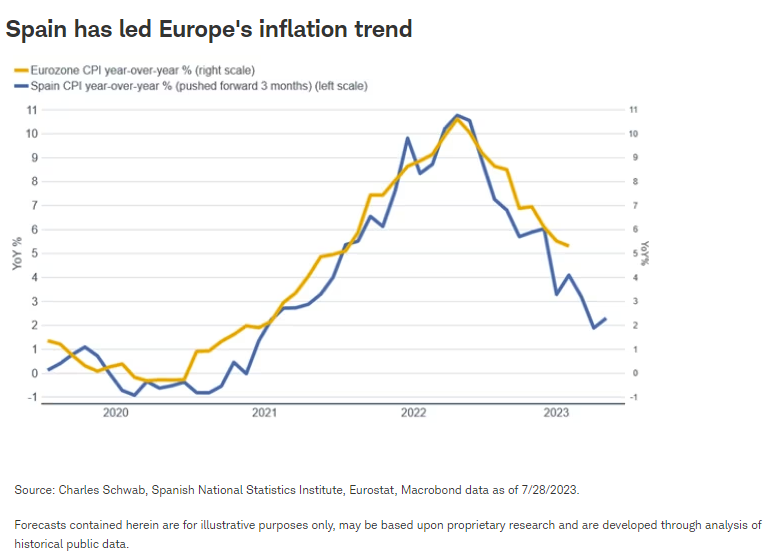

- Inflation seems to be cooling fast in Europe. Spain has already seen inflation retreat to under 2% after peaking above 10% last fall. For the past three years, Spain has consistently led Europe's trend in inflation by three months, possibly because Spain moved more quickly to apply and then phase out government aid during the pandemic. Should this correlation persist, it suggests eurozone inflation may be at the ECB's 2% target by the end of the third quarter—leading to no rate hike in September.

We think that the ECB is probably finished hiking rates, despite the market still pricing in about a 50% chance of another hike (down from 80% ahead of the ECB meeting last week). European stocks are trading at a price-to-earnings ratio of 12, well below their 10-year average. Any signs that rate hikes have come to an end could support valuation gains for European stocks. Stocks in the eurozone reacted favorably to the most recent data, outperforming U.S. stocks last week and adding to this year's outperformance by the MSCI Euro Index over the S&P 500, measured in both euros and U.S. dollars.

Reserve Bank of Australia

While there is a possibility of a final rate hike in Australia this week, the cooling of inflation has increased the likelihood that the Reserve Bank of Australia goes on pause for an extended period. Headline inflation surprised to the downside in the second quarter, rising just +0.8% for the quarter. At the June meeting, Deputy Governor Bullock noted the Board was not on a "pre-set course" and would be monitoring incoming data on inflation, employment, and consumption.

Bank of England

In the United Kingdom, a 25-basis-point (bp) rate hike is expected by the market for this week's Bank of England (BOE) meeting. Commenting on the BOE's 50 bp hike in June, Governor Bailey argued that, since the evidence had called for two successive 25 bp hikes, then it was better to hike by 50 bp. In his guidance, Bailey stated he found it interesting "that the market thinks the peak will be quite short-lived, in a world where we're dealing with more persistent inflation." Further hikes are widely expected—so any signs the BOE could be considering a pause could move markets.

The BOE's aggressive monetary policy has weighed on U.K. stocks this year, leaving the U.K. stock market, as measured by UK FTSE 100 Index, with a 3% gain in local currency for the year—one of the worst performers among developed markets.

Rate cuts

Those countries with rate hiking cycles that led major developed market central banks by six to 12 months are beginning to implement rate cuts. Last week, Chile joined Uruguay and Hungary in a July rate cut. Brazil is expected to cut rates this week, with Peru, Mexico, and Columbia likely cutting rates by year-end.

Divergence

In the second half of the year, central bank policy is diverging from the steady pace of hikes seen in the first half of the year. Perhaps most significantly, a potential unwinding of the yen carry trade could roil markets. These shifts could mean more volatility in currencies, interest rates and stocks than seen in the first half of the year.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. The examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Currencies are speculative, very volatile and are not suitable for all investors.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors.

Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly.

For additional information, please see schwab.com/indexdefinitions.

The Input Prices component of the Japan Composite Purchasing Managers' Index (PMI) measures the conditions surrounding the prices of raw materials and other business expenses experienced by surveyed business leaders in Japan.

A message from Advisor Perspectives and VettaFi: VettaFi’s Fixed Income Symposium was the biggest virtual event of the summer. Register here for the replay link to learn from the experts and thought leaders who participated in the event.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All