Schwab Market Perspective: On the Line

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWill the economy roll into a formal recession, or is a recovery underway? It's a close call.

We've believed all year that the economy has been undergoing a series of "rolling recessions" affecting various industries and sectors. The question is whether it eventually would roll into a formal recession. To date, it's still not clear. Despite the Federal Reserve's efforts to cool economic growth and control inflation, job growth has remained relatively strong—although job expansion historically is common at the beginning of recessions, as we'll discuss below.

Meanwhile, longer-term Treasury yields have risen sharply in recent weeks. While this traditionally is a sign that markets expect stronger economic growth in the future, we think there are other factors currently at work in the bond market: namely, increased bond supply and the potential for lower demand from Japanese buyers.

Finally, the global economy seems to be transitioning out of "stagflation" (low growth and high inflation), to just stagnation as the pace of economic growth and inflation is slow enough to end the rate hiking cycle in most major economies.

U.S. stocks and economy: Strengths and weaknesses

Economic data have looked relatively resilient lately. U.S. gross domestic product (GDP) growth reaccelerated in the second quarter to a 2.4% annualized pace, led by business investment and still-positive consumer spending (though the latter's strength eased from the first quarter). Meanwhile, the U.S. economy added 187,000 jobs in July, per the Bureau of Labor Statistics. While that is a strong gain relative to history, it was softer than the consensus expectation for 200,000 new jobs; also, the prior two months' job gains were revised lower by 49,000 payrolls.

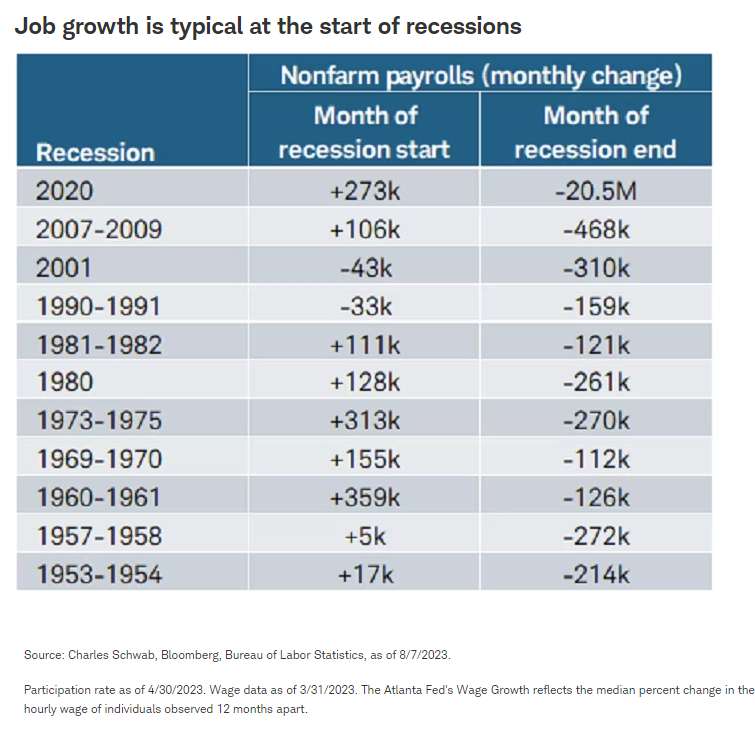

Labor data can often look confusing at economic inflection points. One of the widely held myths around the labor market and recessions is that data don't look poor when a recession begins. That isn't the case, however, when looking at payroll gains at the start of historical downturns. As shown in the table below, out of the 11 recessions going back to the 1950s, nine of them began as the economy was still adding jobs.

That underscores the fact that investors shouldn't place too much emphasis on a single data point when determining the state of the business cycle. That especially holds true today, when there is an almost even split between the number of indicators that signal coming weakness vs. a recovery that is already underway. That dynamic is consistent with our thesis that the economy has been suffering from a series of rolling recessions since the beginning of last year.

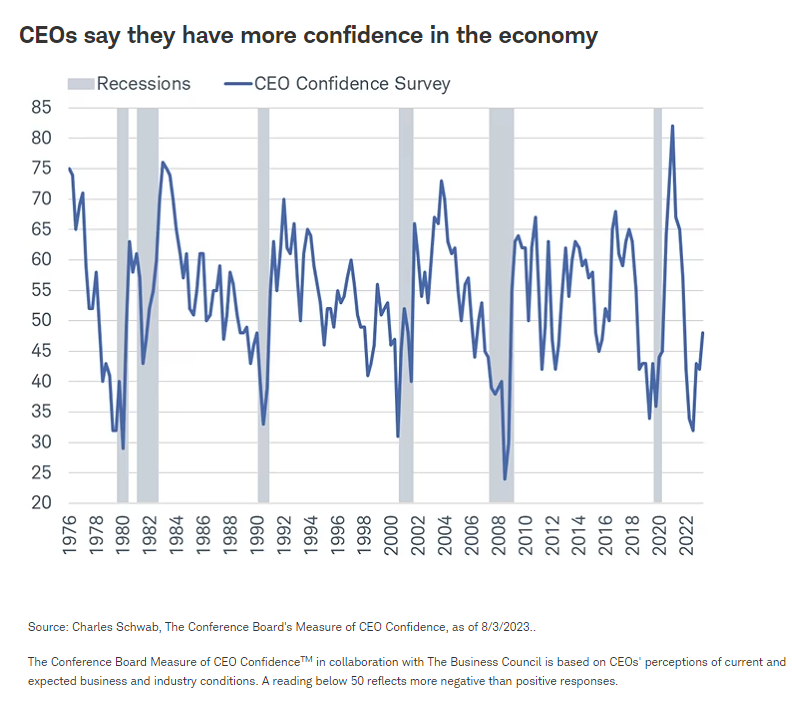

Confidence among CEOs was one of the first areas to slip into a recession. Yet now, as shown in the chart below, executives are increasingly optimistic that the worst might be behind us. A continued improvement should bode well for businesses, but it's worth noting that 84% of respondents in The Conference Board's CEO confidence survey said they still expected the economy to enter a recession during the next 12-18 months (although that was down from 93% in the previous survey).

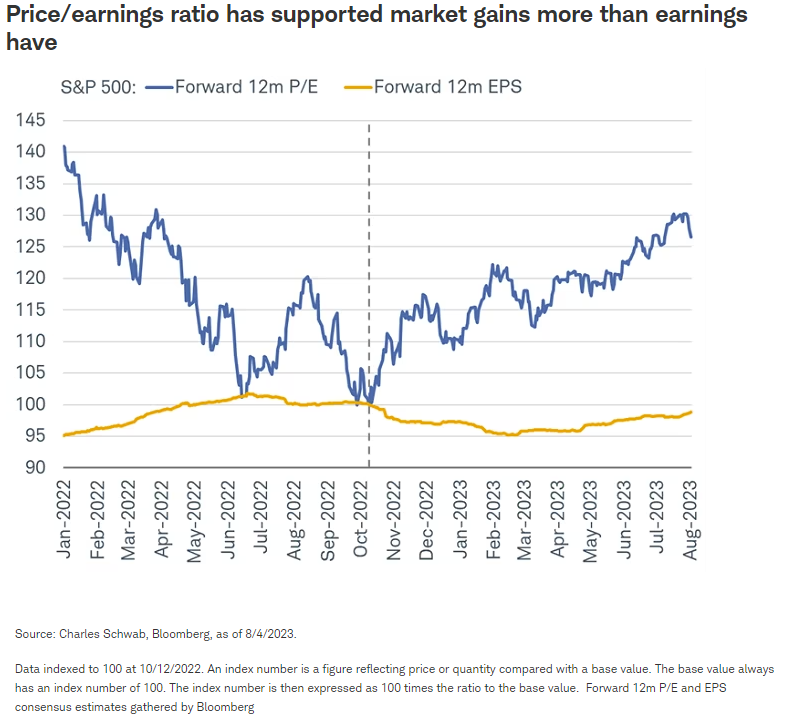

That pessimism might be stemming in part from the lack of improvement in the earnings backdrop. Second-quarter earnings season is nearly over, and thus far, profits are still expected to contract from the prior year (the worst drop since the third quarter of 2020). The decline in earnings historically hasn't been synonymous with prior recessionary drops, but a building risk is that earnings estimates fail to pick up markedly from here. That would work against the strength of the market's rally this year and since the recent low last October—especially because, as shown in the chart below, the advance has been driven entirely by a climb in the forward price-to-earnings (P/E) ratio. Forward earnings growth has yet to contribute to the rally.

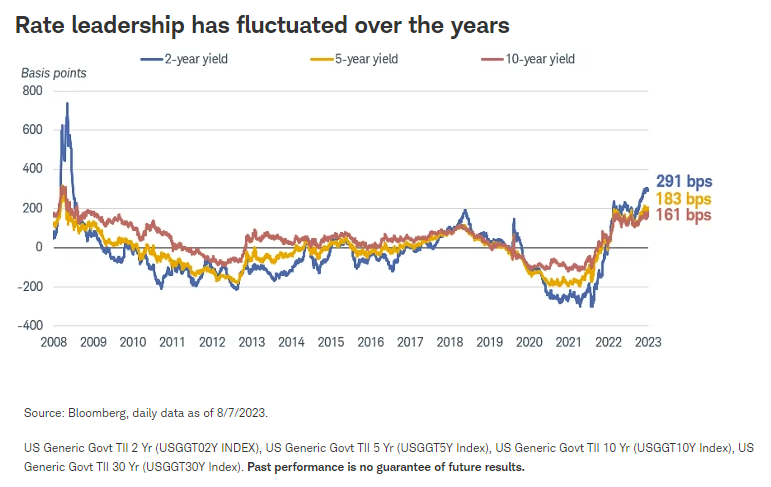

Fixed income: Supply and demand kill the bond rally

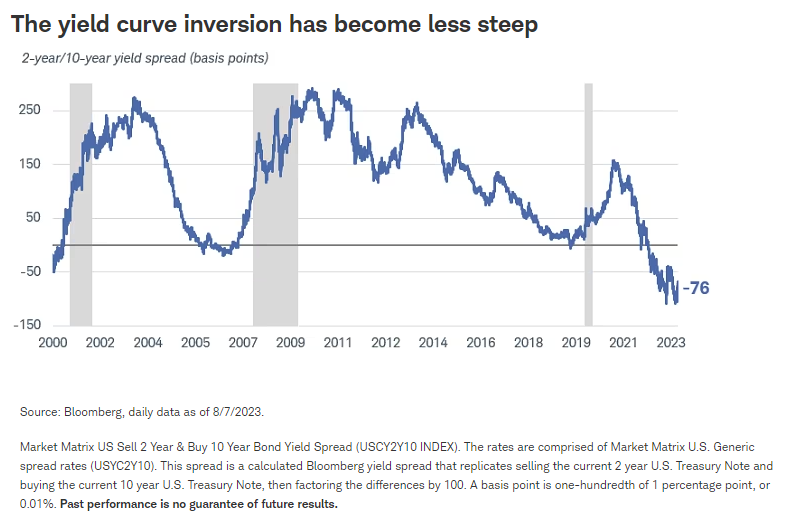

The third quarter kicked off with a sharp selloff in bond prices. Since the beginning of July, Treasury yields (which move inversely to prices) have rebounded sharply, with many maturities near last year's cyclical highs. Unlike earlier in the year, the rise in yields has been driven by long-term rates increasing faster than short-term rates. As a result, the yield curve inversion—when short-term rates are higher than long-term rates—has become less pronounced.

When long-term rates lead the way higher, it is usually due to rising inflation expectations, but the recent rise has largely been due to an increase in real interest rates (that is, rates adjusted for inflation). Inflation expectations have risen, but not as much as nominal yields. That suggests there are other factors at work.

In our view, the timing of the recent spike in yields suggests that concerns about the increase in the supply of bonds is the main culprit. With fiscal budget deficits rising, the Treasury is issuing a record amount of bonds to finance government expenditures. Now that the U.S. debt ceiling has been lifted, the issuance of intermediate- to longer-term bonds is picking up. All else being equal, when supply increases prices tend to fall. That is true in the bond market as it is in other markets.

Concerns about finding buyers for U.S. debt were also complicated by the Bank of Japan's recent decision to allow its government bond yields to rise for the first time in decades. Because Japan historically has been a large buyer of U.S. Treasuries, any change in the attractiveness of Japan's domestic market relative to the U.S. market could be significant. Consequently, Treasury yields are rising to attract buyers at a time when there is potentially less demand and more uncertainty about how high the Federal Reserve will hike rates in this cycle.

Despite these challenges, we don't see yields moving sharply higher from current levels. Much of the negative news appears to be priced into current elevated real yields. In the long run, the direction of yields is driven by prospects for growth and inflation. Indications point to inflation continuing to decline, as the effects of the Fed's policy tightening to date work their way through the economy.

Credit conditions have tightened, which is starting to show up in a slower pace of consumer borrowing and rising delinquency rates on auto loans and credit cards.1 In addition, the pace of job growth and wages is slowing down as the labor market cools off. On the global front, weak manufacturing and trade data in Europe and China2 suggests a slowdown in demand for goods and services, especially commodities, is unfolding.

Global stocks and economy: Out of the box?

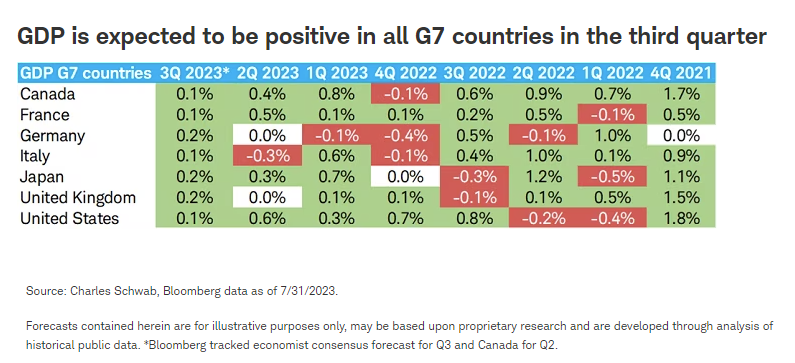

With most second-quarter data now released, economists currently expect the third quarter to be the first with no GDP contraction in any Group of Seven (G7) economies since the fourth quarter of 2021. But this appears to be no V-shaped rebound in economic activity. The forecasts reflect a transition from "stagflation," or no growth and high inflation, to just stagnation as the pace of economic growth and inflation is slow enough to end the rate hiking cycle in most major economies.

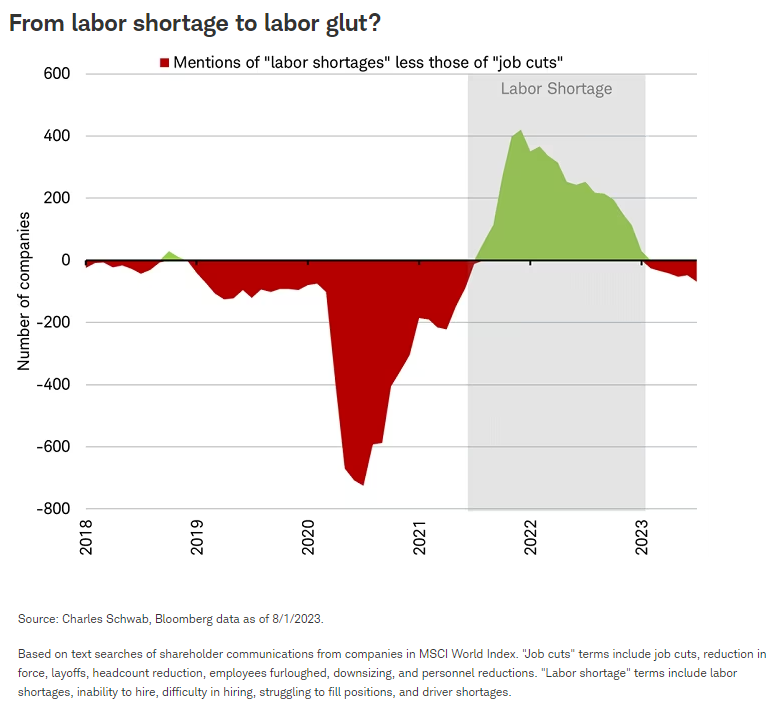

One reason the growth outlook remains sluggish around the world is that the "Cardboard Box" recession concentrated in manufacturing and trade may be coming out of the box and spreading to the formerly healthy services sector of the economy. The services purchasing managers indexes (PMI) fell for either the second or third month in a row in all G7 economies (except Canada, which does not have a services PMI).

Because G7 economies have more service jobs than manufacturing jobs, a weakening trend in services could undermine the job market that has supported consumer confidence. Notably, Canada reported job losses in two of the past three months. The commentary from business leaders on earnings calls so far this reporting season has mentioned layoffs more often than labor shortages. For example, recent layoff announcements have come from a wide range of industries including drug store chain CVS Pharmacy, AB InBev (the parent of Anheuser-Busch), biotech company Biogen, mobile phone chip maker Qualcomm, and money manager T. Rowe Price.

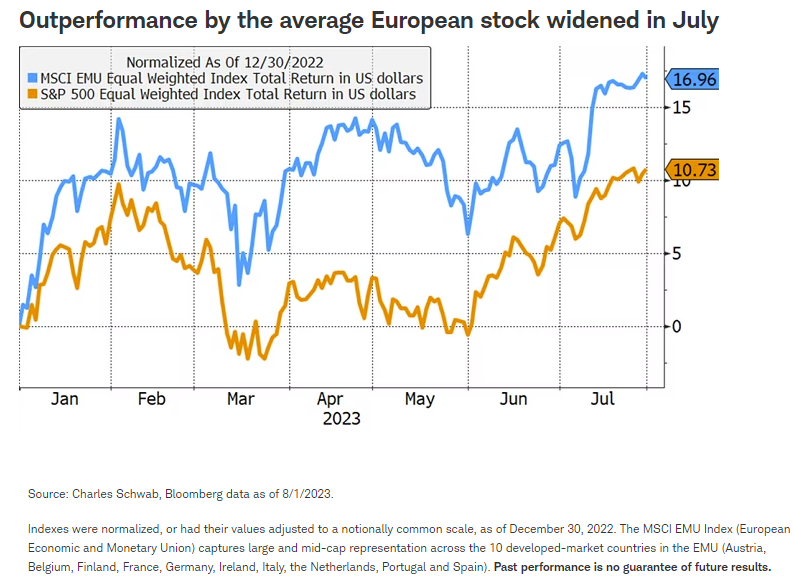

The bright side is that inflation has eased and the rate-hiking cycle for major economies may be over. In addition to the Federal Reserve, both the European Central Bank (ECB) and Reserve Bank of Australia appeared to signal that rate hikes may have ended at their July meetings. Signs that the ECB may shift from its aggressive hiking stance and pause as soon as the next meeting may help lift European stock valuations. The price-to-earnings ratio based on analysts' expectations for next-12-months eurozone earnings (as reflected by the MSCI EMU Index) is 12.4 times earnings, below its 10-year average of 13.9. Investors may have begun to recognize the valuation disparity, as the MSCI EMU Index has posted a gain of 21.6% year-to-date through the end of July, narrowly outperforming the U.S. S&P 500's gain of 20.6%.

Using equal-weighted versions of the same indexes, measured in U.S. dollars, the outperformance by the average European stock is even more impressive, with a total return of nearly 17% year-to-date, compared with the average U.S. stock total return of 10.7%.

1 Federal Reserve Bank of New York, “Quarterly Report on Household Debt and Credit”, 2Q 2023, released August 2023.

2 Eurozone Manufacturing PMI SA (MPMIEZMA Index) as of July 2023, and China Export Trade USD YoY (CNFREXPY Index) as of July 2023.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. All expressions of opinion are subject to changes without notice in reaction to shifting market, economic, and geopolitical conditions. Data herein is obtained from what are considered reliable sources; however, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

All expressions of opinion are subject to changes without notice in reaction to shifting market, economic, and geopolitical conditions.

Past performance is no guarantee of future results.

Investing involves risk including loss of principal.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

International investments are subject to additional risks such as currency fluctuation, geopolitical risk, and the potential for illiquid markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors.

Treasury Inflation-Protected Securities (TIPS) are inflation-linked securities issued by the US Government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based on the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the US Government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

Mortgage-backed securities (MBS) may be more sensitive to interest rate changes. They are subject to extension risk, where borrowers extend the duration of their mortgages as interest rates rise, and prepayment risk, where borrowers pay off their mortgages earlier as interest rates fall. These risks may reduce returns.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Commodity-related products, including futures, carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions, regardless of the length of time shares are held. Investments in commodity-related products may subject the fund to significantly greater volatility than investments in traditional securities and involve substantial risks, including the risk of loss of a significant portion of their principal value.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Treasury Inflation-Protected Securities (TIPS) are inflation-linked securities issued by the U.S. government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based on the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the U.S. government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approve or endorse this material, guarantee the accuracy or completeness of any information herein, or make any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All