Bond investors have been looking for an approach that delivers attractive, repeatable, uncorrelated active returns. Is their wait over?

Higher rates mean bond markets once more offer worthwhile real returns, while more challenging economic conditions are creating greater scope for active fixed-income security selection. But how can investors harvest these opportunities consistently? We believe systematic fixed-income investing approaches can help provide the answer—and offer a high degree of customizability.

What Is a Systematic Approach to Fixed-Income Markets?

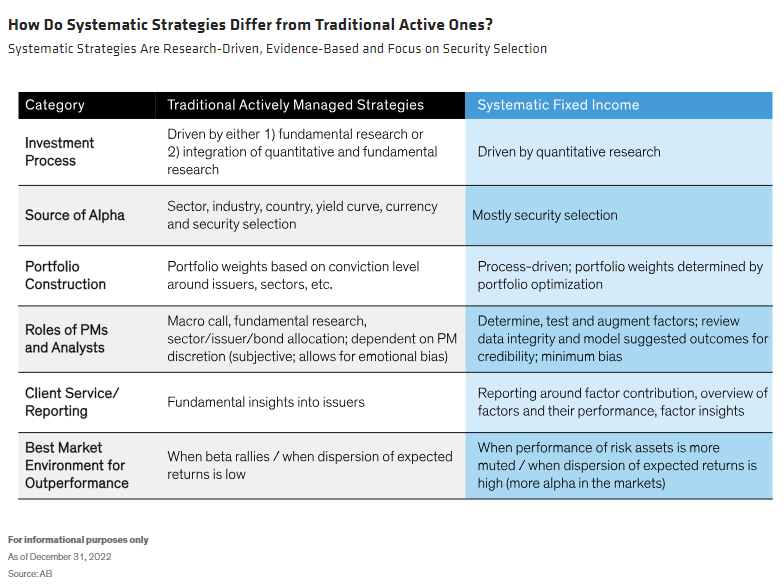

Systematic fixed-income investing is an active approach that aims to outperform bond-market benchmarks. In this approach, a dynamic multifactor process drives the investment decisions, using predictive factors with demonstrable links to outperformance. A quantitative and AI driven decision process ranks each bond in the market based on its alignment with these predictive factors, and so aims to generate outperformance (alpha) through bottom-up security selection.

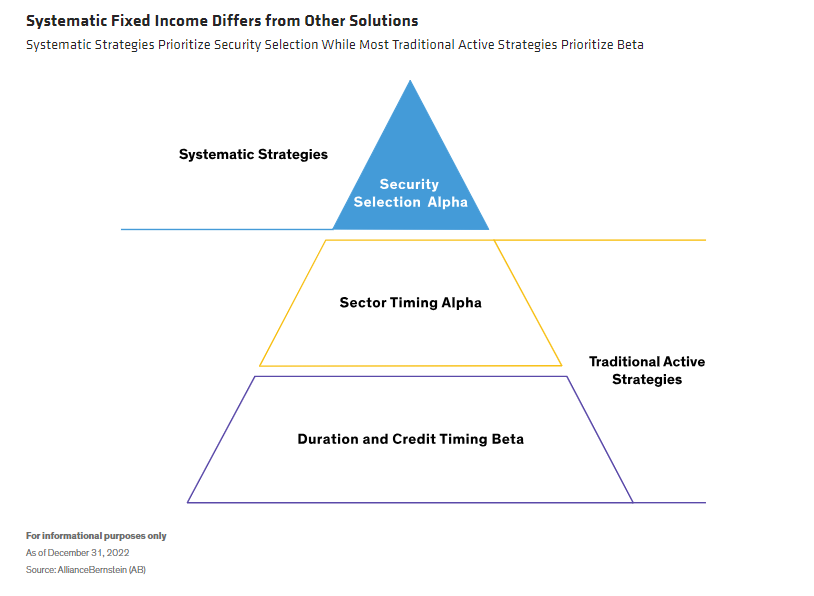

This systematic methodology contrasts with traditional active approaches, which mostly prioritize duration and credit-market exposure (beta) and sector tilts (Display).

Because systematic approaches depend on different performance drivers, their returns will likely be different from—and complementary to—traditional active strategies. The active returns from security selection in systematic strategies are by design largely uncorrelated both with the benchmark and with important risk premia. As a result, these strategies can be effective diversifiers in a fixed-income portfolio. In addition, systematic approaches can enable competitive fee structures, making them a potentially lower-cost way to beat bond benchmarks. They can also be readily customized, allowing managers to tailor portfolios exactly in line with client preferences while retaining performance potential.

How Do Predictive Factors Work?

Risk factors, such as interest-rate risk (duration) or spread duration (the sensitivity of a bond’s price to changes in its credit spread) identify the ways that market drivers can influence security prices. Systematic strategies aim to discover factors that have predictive power to repeatably find securities with the best risk-adjusted return potential—that is, predictive factors. These can be market value–based (for instance, value and momentum) or fundamental, company-specific factors (such as quality). Predictive factor insights are used to systematically analyze large volumes of historical market data and single out securities with the right characteristics to have an above-average probability of outperforming the market (Display).

Managing Factor Strategies in Practice

With our deep research databases, AB is able to identify and access hundreds of proprietary factors. Not all will be implemented continuously in a systematic portfolio, but the manager can rotate them according to market conditions as investment regimes change and the efficacy of the factors varies with them.

Predictive factor–based approaches originated in equity markets, where benchmarks are relatively straightforward to construct, and pricing is largely transparent. Factor-based approaches arrived more recently in fixed-income markets, which are larger, more complex and fragmented across disparate trading pools. All these features make liquidity and pricing harder to discover in bond markets.

For these reasons, advanced technology and analytics are vital to making systematic approaches work in fixed-income markets. And although academic research supports the case for predictive factors in fixed-income investing, it takes rigorous testing and practical implementation skills to create successful portfolios.

Creating a Systematic Portfolio: Combining Predictive Factors

With a systematic approach, each bond in the benchmark is scored on a range of predictive factors. This results in an array of scores for each security. For instance, a bond might have a high score on value but a low score for momentum. A factor combination model then rolls up the different factor scores to produce a single composite total factor score for each security.

The model adopts two criteria to create a portfolio using the factor scores: predictive efficacy and correlation with other factors. It weights them using an algorithm determined by a machine learning technique. This ranks the total factor score for each bond subject to other optimization and risk constraints, principally: bond, issuer, sector, ESG, duration, spread, liquidity and transaction cost limits. In this way, the model seeks superior risk-adjusted returns by balancing predictive efficacy with rigorous risk controls.

Three Critical Success Factors

In this relatively new field, the performance of some providers’ systematic fixed-income products has proved disappointing, with live returns failing to live up to back-tested results. We think there are three frequent failings: relying on static factors, using unreliable data, and an inability to source liquidity and to execute ideas effectively. These illustrate the importance of three “pillars” for effective systematic strategies:

A Dynamic Factor Approach. Market conditions are always changing, and factor efficacy varies from market to market and over time. For instance, carry (yield) may be a strong factor in investment-grade bond markets but not in high yield, where default risk is a more important performance driver. Consequently, it’s crucial to evaluate factors continuously and manage them dynamically.

Abundance of Data. Reliable data are the indispensable building blocks of effective systematic strategies. Systematic investors need vast quantities of data that are clean (free of anomalies and inconsistencies), extensive and have a very long history. Compiling those data is a laborious, research-intensive task. It involves amassing data that extend across a wide range of bond metrics, include point-in-time analytics for companies’ financials across multiple fields and cover many fixed-income classes globally.

Liquidity Considerations. Firms that can’t effectively assess a bond’s liquidity won’t be able to implement their investment ideas. To keep up in a marketplace that will digest and react to every new bit of information faster and faster, successful fixed-income managers need to use technology that pulls all external fixed-income trading platforms together in one place. Finding adequate liquidity to execute desired trades is a precondition for managing a portfolio’s factor weights. And finding enough liquidity at attractive prices is paramount because systematic strategies only execute trades if they pass tests for transaction-cost effectiveness.

An Idea Whose Time Has Come

We believe systematic fixed-income investing is an idea whose time has come. It provides an active, cost-effective way to achieve attractive, repeatable and uncorrelated risk-adjusted returns through:

Bottom-up selection and structuring of many independent bond holdings

A high level of risk control that makes systematic portfolios relatively less vulnerable to big drawdowns resulting from adverse interest-rate, credit and other single-factor events

This dual emphasis on outperforming through individual security selection and rigorous risk control makes systematic approaches complementary to most traditional active fixed-income strategies, and potentially powerful portfolio diversifiers.

Investors today face a world where conditions are rapidly changing, with increased availability of data and the advent of AI shifting familiar paradigms. We believe a leading-edge systematic approach that utilizes these new developments can help provide an objective, evidence-based path to more consistent risk-adjusted fixed-income returns.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein